Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

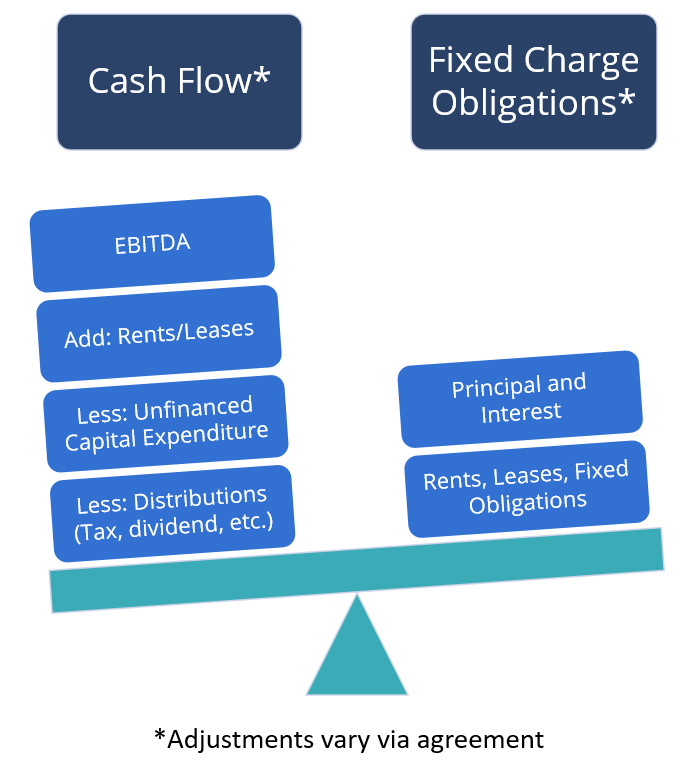

A measure of a company’s cash flow to meet fixed charge obligations

The Fixed Charge Coverage Ratio (FCCR) compares the company’s ability to generate sufficient cash flow to meet its fixed charge obligations, such as the required principal and interest payments on debt. It may include leases and other fixed charges. It is an important financial ratio, and when it is a debt covenant, it also governs the company’s ability to incur or refinance debt from lenders.

As with other non-IFRS/GAAP measures, lenders and borrowers negotiate and specify the lending ratio calculation within a credit agreement.

As a proxy for cash flow, analysts may start with earnings before interest, tax, depreciation, and amortization (EBITDA), then make adjustments. These adjustments add rents and lease expenses (EBITDAR), deduct capital expenditures paid for by earnings (i.e., the portion that’s not funded by debt), and deduct distributions (examples such as cash taxes and cumulative dividends).

Fixed charges may include long-term debt repayment (such as scheduled or current portions) and interest expenses, with adjustments to include obligations such as rents and leases, cash taxes, and other fixed charges.

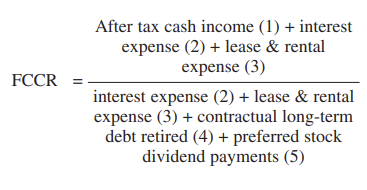

An example of an FCCR definition from the Federal Reserve [1] manual for supervising bank holding companies is duplicated below. As there is no one definition in use, actual practice in the industry will depend on an agreement between the parties involved.

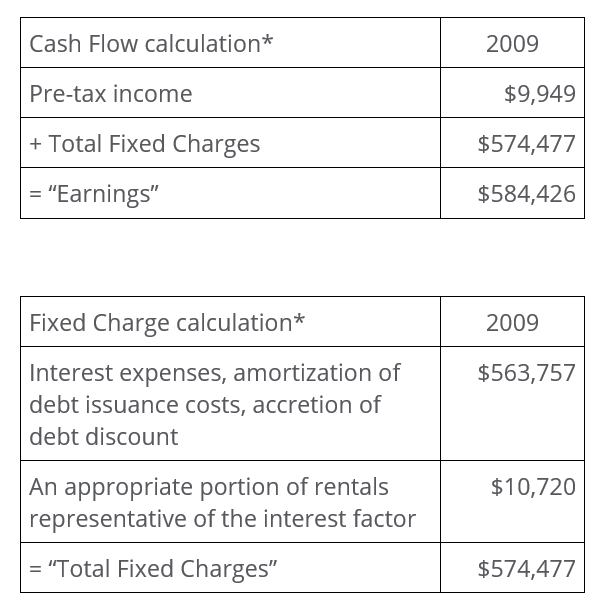

The abstract below is from the SEC filing of MF Global Holdings Ltd.[2], a company that filed for bankruptcy in 2011.

One can note here that a weak and declining FCCR could have been an early warning of the potential inability to service fixed obligations.

For this company, cash flow was defined as “pre-tax income/(loss) from continuing operations” (EBT), then adding “total fixed charges” to arrive at “earnings.”

The two main categories of fixed charges were “interest expenses, amortization of debt issuance costs, accretion of debt discount,” and “appropriate portion of rentals representative of the interest factor.”

This further highlights how fluid the definition of FCCR can be; regardless of how it is defined, it can be directionally relevant to lenders and equity investors as a sign of potential financial distress and future solvency issues.

* As defined between borrower and lender.

In 2009, the FCCR was 1.02 ($584,426 / $574,477), and the company had pre-tax losses in the two years before bankruptcy, which caused the ratio to fall below 1.

The fixed-charge coverage ratio is regarded as an important financial ratio because it shows the ability of a company to repay its ongoing financial obligations when they are due.

If a company cannot meet its financial obligations, it may be in financial distress. Unless remedied, it’s possible that the company will only be able to remain solvent for a limited period of time.

Here is a way to evaluate the FCCR number:

Therefore, the higher the fixed-charge coverage ratio value, the better. It measures directionally whether a company operates with adequate revenues and cash flow to meet its regular payment obligations.

Lenders or analysts often use the FCCR to assess the adequacy of a company’s cash flows to handle its recurring debt obligations and regular operating expenses.

They are not; however, they are used in a similar manner by lenders and analysts seeking to understand the financial health of an operating company. Conceptually, both ratios are trying to measure a company’s ability to generate enough operating profit to service its fixed obligations (including debt repayment).

An argument as to why FCCR is more comprehensive than DSCR is that the latter does not adequately capture certain fixed obligations that a company legitimately requires in order to operate. These include rent at physical premises, unfunded maintenance CAPEX, dividend payments on preferred stock, etc.

This Fixed Charge Coverage Ratio Template will allow you to compute the fixed charge coverage ratio using annual expenses and EBITDA figures. You may also make adjustments to suit your circumstances.

Here is a preview of the template:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is a leading provider of financial analysis courses, including the Commercial Banking & Credit Analyst and Financial Modeling & Valuation Analyst (FMVA)™ certification program. To help you advance your career, check out the additional CFI resources below: