Default Rate

The rate of all loans issued by a lender or financial institution that is left unpaid by the borrower and declared to be in default

What is the Default Rate?

The default rate is the rate of all loans issued by a lender or financial institution that is left unpaid by the borrower and declared to be in default. An individual loan is typically declared in default if no payments are made for an extended period as per the initial loan agreement. The account in arrears will then be transferred to a third-party debt collection agency.

The role of the collection agency is to contact the individual or business and collect the unpaid, overdue funds. If funds are still not successfully recovered from the collection agency, the defaulted loans are written off by the financial institution as a loss or expense.

Summary

- The default rate is the rate of all loans issued by a lender or financial institution that is left unpaid by the borrower and declared to be in default.

- The lending institution will write off the entire value of defaulted loans, removing them from the books altogether.

- The default rate is important for institutions to reassess their risk from borrowers and is also an important representation of economic conditions.

Understanding the Default Rate

It is the borrower’s responsibility to make on-time payments as per the initial agreement with the financial institution. Whether through a mortgage payment or a credit card agreement, the borrower may fail to make the payments. To be considered a defaulted consumer loan, multiple consecutive payments have not been received over several months.

Defaulting on a loan will damage the borrower’s credit score, making it difficult to receive approvals on loans in the future. Even if a future loan were to be approved, the low credit score would likely lead to a much higher interest rate on loans.

Before being considered a defaulted loan, a loan with a missed payment is a delinquent loan. The period in which a loan is delinquent is the duration in which the lending institution allows some time to pass before declaring the loan defaulted. During such a time, the borrower must act and make up missed payments to avoid the consequences of a defaulted loan.

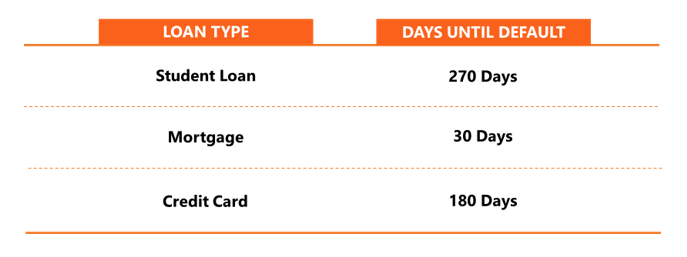

If the borrower still does not make up their missed payments, the lender will eventually write off the loan and declare it to be in default. The timeframe for default may vary depending on the type of loan. For student loans, default is approximately 270 days or nine months that no payments have been received.

Default Rate Formula

The default rate is calculated using the following formula:

Importance of Default Rates

Default rates are important for lending institutions to measure their risk from borrowers. If a lending institution finds that they incur a high default rate, it is an important indicator for them to review their lending procedures. A higher default rate leads to a higher rate of risk for the institution. By aiming to lower the default rate, the institution can protect itself from any major losses with borrowers who default.

Certain groups are more likely to default than compared to others. For example, it would typically include people who are young, unemployed, or living in a single household.

Alternatively, default rates may be representative of economic conditions. Default rates are high during periods of economic pressure and low during periods of economic growth. Default rates may also be applied to situations outside of lending, such as bond default rates or even corporate default rates.

Period Until Default After Last Payment

Routinely Missed Payments

Lending institutions may implement consequences for borrowers with routinely missed or late payments.

One strategy a lender may implement is to increase the interest rate on the borrower’s remaining loan after delinquency. The substantially higher interest rate is referred to as the penalty rate. The lender may decide to lower the penalty rate if the borrower successfully makes on-time payments.

Another strategy allows the lending institution to take hold of personal assets after a defaulted loan. Personal assets may include property, wages, retirement savings, or investments. For example, upon taking ownership of a property, the bank may recover some of its losses on the loan. Through the process of foreclosure, the bank can sell the property.

Both strategies allow the lender to reduce their potential loss from defaulted loans.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: