Grace Period

A period after the deadline for a financial obligation where a late fee is waived if the financial obligation is satisfied within that period

What is a Grace Period?

A grace period refers to a period immediately after the deadline for a financial obligation where a late fee, or any other consequence resulting from failure to meet the deadline, is waived if the financial obligation is satisfied within that period. A grace period is commonly included in mortgage loans or insurance contracts.

Summary

- A grace period is a period after the deadline for a financial obligation where a late fee is waived if the financial obligation is satisfied within that period.

- The grace period duration varies depending on the contract and debt instrument but is usually 15 days.

- Satisfying a financial obligation during the grace period will not negatively impact an individual’s credit score.

Understanding How a Grace Period Works

The grace period duration varies depending on the contract and debt instrument but is usually 15 days. During the grace period, if the financial obligation is satisfied, penalties such as late fees and credit report impacts are annulled. A grace period timeline is graphically illustrated below:

Although late fees are annulled during the grace period (assuming the outstanding financial obligation is satisfied during the grace period), interest on the outstanding balance may continue to accrue depending on the debt instrument and/or contract.

With that in mind, it is important to check the details of the grace period in every contract – credit cards typically do not charge interest during the grace period while loans (such as student loans) typically accrue interest.

Grace Period and its Impact on Credit

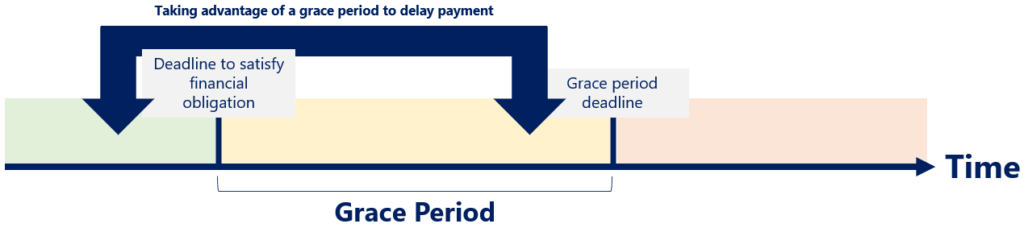

According to consumer credit reporting company Experian, individuals who satisfy their financial obligation during the grace period will not see their credit score adversely impacted. If interest does not accrue during the grace period, it may be favorable for individuals to satisfy their financial obligation during the grace period rather than at the initial deadline. It is illustrated below:

As shown above, by utilizing a grace period, an individual can delay their payment and achieve greater financial flexibility.

Potential Penalties

In addition to late fees that must be paid if a financial obligation is not satisfied before the end of the grace period, there may be other consequences, which may include:

- Interest rate hike: The go-forward interest rate may be increased if a payment is missed. For example, if a mortgage payment is unsatisfied before the end of the grace period, the lender may have the option to instill an interest rate hike on future mortgage payments.

- Seizure of collateral: The lender may seize assets pledged as collateral if a financial obligation is outstanding for an extended duration. For example, if a mortgage payment is unsatisfied months after the end of the grace period, the lender may have the option to seize the property.

- Damage to credit score: Missing a payment, or paying late, will generally negatively impact an individual’s credit score. A low credit score may impact an individual’s ability to secure credit at favorable rates.

Example of Grace Period

On January 1, 2021, Tim took out a $10,000 loan to grow his small business. The following are the key terms within the loan contract:

- The principal of $10,000 is due on January 1, 2022 (one-year maturity);

- A grace period of 15 days after the due date of January 1, 2022;

- $500 late fee if the loan is not paid by the end of the grace period; and

- Interest-free, but with a 10% weekly interest rate if the loan is not paid in full by the due date of January 1, 2022.

Consider the following scenarios:

How much does Tim pay under each scenario?

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: