Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

When a bank or other mortgage lender agrees to temporarily either forego a borrower’s mortgage payments or reduce them

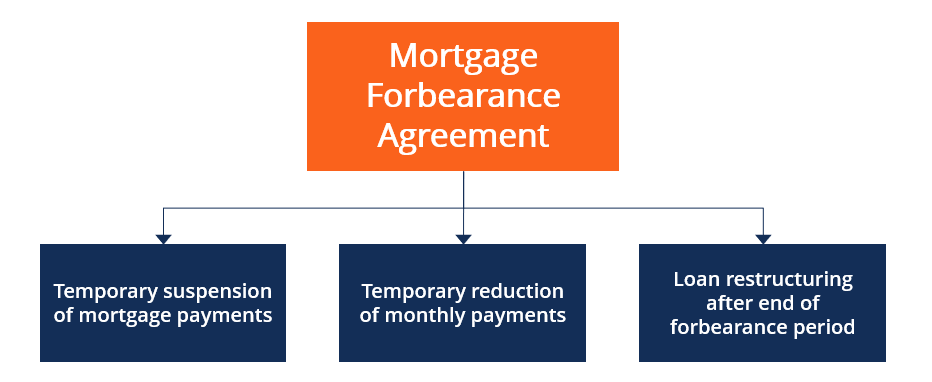

A mortgage forbearance agreement is made when a bank or other mortgage lender agrees to temporarily either forego a borrower’s mortgage payments or reduce them. Lenders are open to making such agreements during times of economic crisis, such as the Global Financial Crisis of 2008 or the COVID-19 pandemic in 2020. When a mortgage forbearance agreement is in place, the lender will not initiate foreclosure proceedings against the mortgage borrower.

The agreement does not mean that the mortgage borrower doesn’t have to eventually make all the required payments per their original mortgage loan agreement. They will have to make up the deficit in payments at some point in the future. The forbearance agreement is only intended to provide temporary financial relief for the borrower.

The agreement details how the payment deficit will be made up by the borrower. The terms vary from one lender to another and may also vary based on the individual borrower’s financial situation.

The options for making up the missed payments include paying a lump sum all at once by a designated future date, making additional payments with your regular monthly mortgage payment, or making additional payments that are added onto the end of your original mortgage agreement. The repayment structure can be negotiated with your mortgage lender.

A mortgage forbearance agreement may go as far as a complete restructuring of your original mortgage agreement. Your lender may be willing to offer a variety of options to assist you in paying off your home loan after the period of forbearance expires (loan modification plans are not typically offered during the forbearance period – only after it is concluded). Commonly offered options include the following:

In response to the COVID-19 pandemic, which left many people suddenly unemployed or with a severely reduced income, the U.S. Congress passed the CARES Act – the Coronavirus Aid, Relief, and Economic Security Act – to help struggling homeowners with mortgage loans. The provisions of the legislation offered help to anyone with a mortgage loan that is backed by the federal government, such as an FHA loan, or backed by a Government Sponsored Enterprise (GSE), such as Freddie Mac or Fannie Mae.

The first key provision of the law prohibits the mortgage lender or servicer from initiating foreclosure proceedings against the protected mortgage borrowers before at least June 30, 2020 – it is expected that Congress will extend the date to a point further in the future. Secondly, the act enables mortgage borrowers to request a mortgage forbearance agreement extending for up to 12 months.

Another key provision of the act is that it prohibits lenders from reporting past-due payments to credit bureaus during the period of forbearance. It is important because normally, in a mortgage forbearance agreement, the lender will still report past due payments to credit bureaus, thereby negatively impacting the borrower’s credit score. However, the effect on the borrower’s credit score will be considerably less damaging than a foreclosure.

It is important for mortgage borrowers to understand that they are not automatically granted a mortgage forbearance. They must contact their lender or mortgage servicer and request such an agreement. An important provision of the CARES Act precludes the mortgage borrower from being charged any extra interest or loan-related fees in conjunction with the forbearance agreement.

The CARES Act only offers mortgage assistance for borrowers with mortgage loans backed by a federal government agency. However, mortgage borrowers with loans that are not backed by any federal agencies may still be able to obtain a mortgage forbearance agreement.

To do so, they must contact their lender or mortgage servicing company and request a forbearance arrangement. If an individual does not know which company services their mortgage loan, they can find out by searching on the Mortgage Electronic Registration Systems (MERS) website.

Most lenders and mortgage service companies would prefer to help borrowers in paying off their mortgage rather than initiate foreclosure proceedings. Therefore, if the borrower explains their current financial situation to them and requests a forbearance agreement, most lenders will be willing to work out such an arrangement with their customers, tailored to fit their situation and ability to make payments.

Again, a forbearance agreement may not be a total suspension of payments, but only a temporary reduction in the required monthly payment amount.

Some lenders are also offering forbearance agreements on home equity loans that a mortgage borrower has taken out.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: