Overcollateralization

The situation where an asset (or assets) value used as collateral on a loan exceeds the loan value

What is Overcollateralization?

Overcollateralization is used to define the situation where an asset (or assets) value used as collateral on a loan exceeds the loan value. It is commonly used by borrowers to reduce credit risk for the creditor and enhance the loan’s credit rating.

Summary

- Overcollateralization is used to define a situation where the collateral value exceeds the loan value.

- The collateralization ratio is calculated as collateral value/loan value.

- Overcollateralization is a credit enhancement technique.

The Collateralization Ratio

The collateralization ratio is outlined below:

A collateralization ratio that exceeds one indicates an overcollateralization loan. The collateral value used is generally the liquidation value – the asset’s value if it were to be sold quickly. The fair value could also be used but may not be relevant for the lender if they plan to quickly sell the asset instead of deriving a fair value from the open market.

Determining the Collateral Value

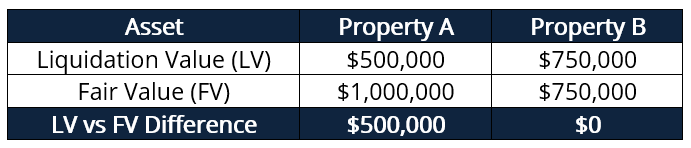

A borrower approaches a lender to obtain a $1,000,000 loan. The borrower is willing to pledge one of the following assets (Property A or Property B) as collateral for the loan:

Property A is situated in a real estate market with infrequent property transactions, resulting in a liquidation value and fair value differential of $500,000. On the other hand, Property B is situated in a real estate market with frequent property transactions, resulting in an identical liquidation and fair value.

The lender lacks a real estate background and would choose to sell the property quickly should the borrower default on its loan. With the information provided above, which property would the lender want the borrower to pledge as collateral?

Answer: Given that the lender is looking to quickly sell the property in the case of default, the lender would most likely want the borrower to pledge Property B. Although Property A’s fair value is $1,000,000, the real estate market it is situated in sees infrequent property transactions. As a result, it may take some time for Property A to be sold on the market for its fair value.

Overcollateralization and Credit Enhancement

Overcollateralization is a credit enhancement technique and limits the credit risk faced by the creditor. By posting collateral value that is greater than the loan value, credit risk is eliminated – the lender could liquidate the collateral to redeem any potential loan losses.

For example, if the collateral value were $500,000 and the borrower defaults on a loan with a face value of $400,000, the lender would see an easier time redeeming the defaulted loan amount than a collateral value of $300,000.

Overcollateralization is a common credit enhancement technique in securitized products such as mortgage-backed securities (MBS) and collateralized loan obligations (CLO). Even if some of the underlying payments are late or in default, holders of securitized products can still receive their principal and interest payments.

Practical Example

A business owner is seeking a $100,000 loan. The business owner finds a lender who can lend the full amount but with an interest rate per annum of 10%. To help reduce credit risk faced by the lender and negotiate a lower interest rate, the business owner offers property with a liquidation value of $150,000 as collateral for the loan.

Due to the collateral value exceeding the loan value (overcollateralized), thereby reducing the lender’s credit risk, the lender happily agrees to lower the interest rate per annum to 8%.

Related Readings

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: