Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Securities that are backed by a pool of loans

Collateralized loan obligations (CLO) are securities that are backed by a pool of loans. In other words, CLOs are repackaged loans that are sold to investors. They are similar to a collateralized mortgage obligation (CMO), except that the underlying instruments are loans instead of mortgages.

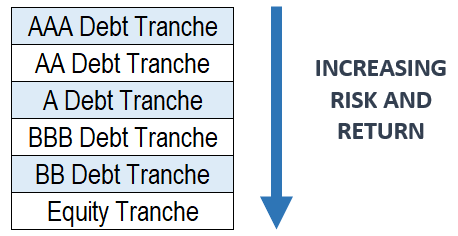

With a collateralized loan obligation, debt payments from the underlying loans are pooled together and distributed to investors of various tranches in the CLO. In a CLO, there are several tranches, as illustrated below:

Investors can choose to invest in whichever tranche meets their risk/return profile. The higher rated the tranche, the less risky and lower the return. For example, the AAA debt tranche comes with the lowest default rate and the lowest return. On the other end of the spectrum, the equity tranche offers the highest default rate and the highest return.

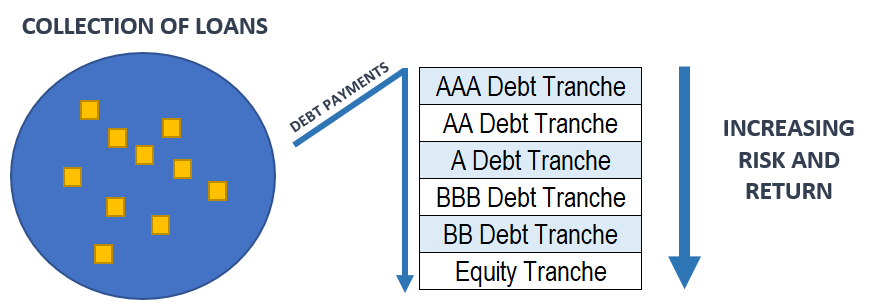

The underlying loans of a CLO are majority comprised of first-lien senior-secured bank loans. Other types of loans that can be found in a CLO are second-lien and unsecured debt. Debt payments made on the underlying loans are pooled together and distributed to investors starting at the top of the tranche to the bottom. The fact is illustrated below:

The illustration above explains why the bottom of the tranche is riskiest but generates the highest return. Investors at the bottom of the tranche face the highest risk. If borrowers in a collateralized loan obligation default and are unable to make their debt payments, investors at the bottom of the tranche would be the first to suffer losses. To compensate for such risks, investors at the bottom of the tranche are provided a higher return.

The creation of a collateralized loan obligation can be simplified as follows:

As mentioned above, collateralized loan obligation managers use the capital raised from investors to purchase loans. However, how are such loans sourced?

It is important to note that CLOs are crucial to the loan markets. According to Reuters, CLO managers are the largest buyers of leveraged loans.

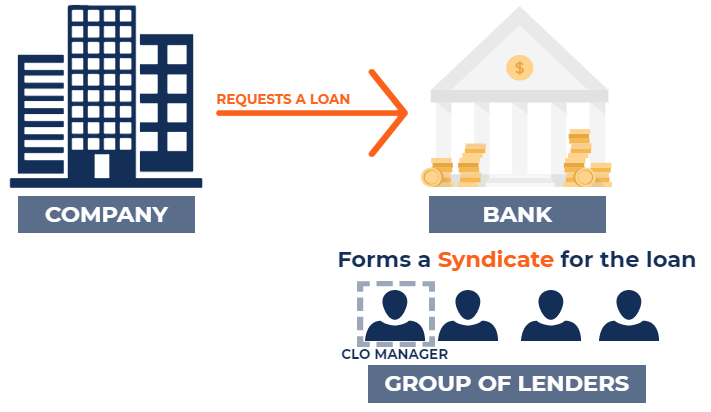

Managers purchase loans through a syndication process. For example, a company may be looking for money to expand their operations and approaches a bank for a $100-million loan. The bank approves the $100-million loan, but to reduce risk, breaks the loan to smaller bits and looks for other lenders to help contribute the $100 million (forms a syndicate). Lenders such as the collateralized loan obligation manager purchase the loans. The process is illustrated below:

To an investor, there are several advantages to investing in a CLO:

The higher-ranking tranches in a CLO are over-collateralized in that even if a number of loans default, the higher-ranking tranches would not be affected. In the event of loan defaults, the lower tranches are the first to suffer losses.

The underlying loans of a collateralized loan obligation are floating-rate loans. This, in effect, results in a low duration. Therefore, collateralized loan obligations are subject to risk from changes in interest rates.

CLOs are actively managed and monitored by a loan manager (or loan managers). Although the managers collect management fees, they are usually linked to the performance of the collateralized loan obligation.

Due to CLOs consisting of floating-rate loans, they can be used as a hedge against inflation.

Over the long term, according to PineBridge, CLO tranches significantly outperformed other corporate debt categories (bank loans, non-investment-grade bonds, investment-grade bonds, etc.).

Thank you for reading CFI’s guide on Collateralized Loan Obligations (CLO). To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below: