Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A field of finance that seeks to de-risk the timing and trust issues that are inherent in commercial transactions conducted on credit terms

Trade Finance is a broad term with many important sub-topics – all revolving around structuring transactions to de-risk as many elements as possible for the parties involved: sellers, buyers, and the finance community. Trade finance risks include (but are not limited to) payment risk, performance risk, and currency risk.

Conducting business on credit terms with any counterparty requires a lot of trust, particularly when the two parties are unknown to each other. Conducting trade with a foreign partner in another country makes the process even more complicated. The concept of Trade Finance has evolved to help resolve as many of these trust issues as possible.

Trade partners, their advisors, and the financial institutions that represent them use a variety of insurance products, creative payment terms, and financing structures to try and create optimal conditions for each party.

You’ll note that there is very little trade risk for a restaurant that serves its customer a meal and then receives payment for that meal before the customer leaves the premises. It is called a “cash” transaction since the goods and the payment are exchanged in real-time.

Trade risks emerge specifically where there is a timing gap between when a product is sold (or a service is rendered) and when payment for this product or service is received; a longer gap tends to correlate with greater risk, though that is not a universal rule. These transactions are conducted on what’s called credit terms.

Let’s look at an example in order to illustrate some of the most important trade risks that arise from transactions conducted on credit terms.

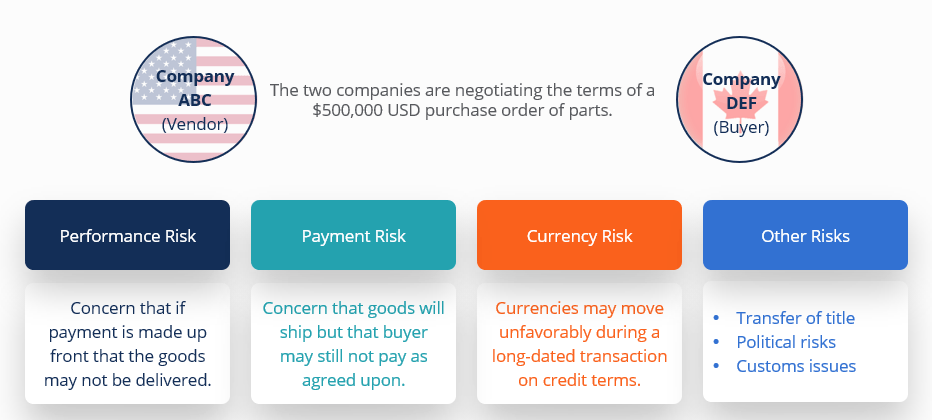

Company ABC (the vendor) is in the United States; it’s a manufacturer of aftermarket automotive parts. Company DEF (the buyer) is in Canada – it’s a high-end auto shop. ABC and DEF have never done business together.

The two companies are negotiating the terms of a USD$500,000 purchase order of parts. The parts are mostly in stock, but the full order is unlikely to ship for a month. ABC expects that the shipment itself will then take another 30 days. The vendor wants cash upfront, but the buyer wants net 30 credit terms. For simplicity, let’s say that the CAD/USD spot rate is 1.25, which means that transaction would cost Company DEF the equivalent of CAD$625,000 (500,000 * 1.25).

Performance Risk – Company DEF (the buyer) is worried that if they pay upfront, ABC (the vendor) may not deliver the goods. This is performance risk, the idea that the counterparty may not perform.

Payment Risk – Company ABC (the vendor) is worried that if they agree to credit terms that the goods will be shipped, but then Company DEF may not pay. This is payment risk – the notion that a vendor may uphold its obligation in the transaction but that the buyer still doesn’t settle the invoice.

Currency Risk – Let’s assume that the two parties do move forward on credit terms, then there’s an estimated 90 days between signing the purchase order (PO) today, and the expected payment date (30 days to ship, 30 days in transit, followed by 30-day payment terms). What if (for example) during that 90-day period, the CAD/USD spot rate moved from 1.25 to 1.3?

While in this case, ABC (the vendor) doesn’t care since the deal was denominated in USD, this same USD$500,000 transaction would now cost Company DEF the equivalent of CAD$650,000 (500,000 * 1.3) – which is $25,000 more in its home currency. This is currency risk (often called FX risk), the idea that two currencies may move unfavorably during a long-dated credit transaction.

“Other” Risks – There are many “other” trade risks and questions that may arise from a transaction of this nature. These include but are not limited to:

Financial service providers participate in Trade Finance in a number of important ways. The first is as a general steward of the transaction, which includes supporting FX needs and the facilitation of payments. The second is as a provider of credit to help facilitate transactions – typically through pre-shipment or post-shipment financing structures. A third critical role is as a trusted intermediary by issuing guarantees and supporting document reviews.

Financial institutions, especially global banks, offer a wide variety of services. When it comes to supporting global trade, perhaps most importantly, banks facilitate the actual payments upon settlement of terms by the two parties – often by way of a wire transfer. Global banks are typically members of international payment networks, the largest and most notable of which is SWIFT (the Society for Worldwide Interbank Financial Telecommunication).

Global banks also have Capital Markets or Securities divisions. These groups support clients with a variety of FX needs – most importantly, spot transactions for other global currencies. These Securities groups can also support more advanced risk mitigation techniques, including FX hedging strategies using Forwards and Futures contracts. Hedging is a suitable strategy for a client like our example company DEF.

As you may imagine, financing trade in this context can be pretty nuanced. For instance, a particularly large purchase order from a brand new overseas customer may set off alarm bells for a vendor’s bank representatives; however, it’s potentially at the same time that the vendor most needs working capital support to execute the contract.

Another example is a domestic borrower that has 90% export clients; it may be hard for that firm’s lender to get comfortable with the borrower’s accounts receivable as security for the operating line of credit since the customers are located in other countries. The lender may require its client to seek out foreign receivables insurance to help offset this risk.

Lenders extend different types of trade finance-related credit products; typically, these are classified as either pre-shipment or post-shipment (sometimes called pre-receivable and post-receivable). An example of a pre-shipment credit solution is Purchase Order (PO) Financing. An example of post-shipment financing is Accounts Receivable (A/R) Factoring (sometimes called Invoice Discounting). While some traditional financial institutions provide these credit products, many non-bank, private lenders have emerged as specialists in the field.

Another common Trade Finance instrument is a Letter of Credit (LC). LCs can be financial in nature, or they can be what’s called a Documentary (or Standby) LC – both are a guarantee of funds being available. Financial LCs are similar to a certified cheque in retail banking and are meant to be cashed; Standby LCs serve as a guarantee of payment should actual payment not be made. This type of trusted intermediary role is the third important category of bank participation in trade finance.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Trade Finance. To keep learning and developing your knowledge base, explore the additional relevant resources below, including taking our Trade Finance Course: