All Risks Yield (ARY)

A conventional real estate metric that uses annual rental revenue to determine the capital value of an investment

What is All Risks Yield (ARY)?

All Risks Yield (ARY) is a conventional real estate metric that uses annual rental revenue to determine the capital value of an investment. ARY comprises both gross and net yields. The net yield includes the deduction of some expenses – surveyors’ fees, management fees, repairs, running costs – which are not deducted in the gross yield. Investors and valuers use ARY in decision-making to pinpoint probable risks in any investment. The metric offers a holistic assessment of the property market‘s general condition.

Summary

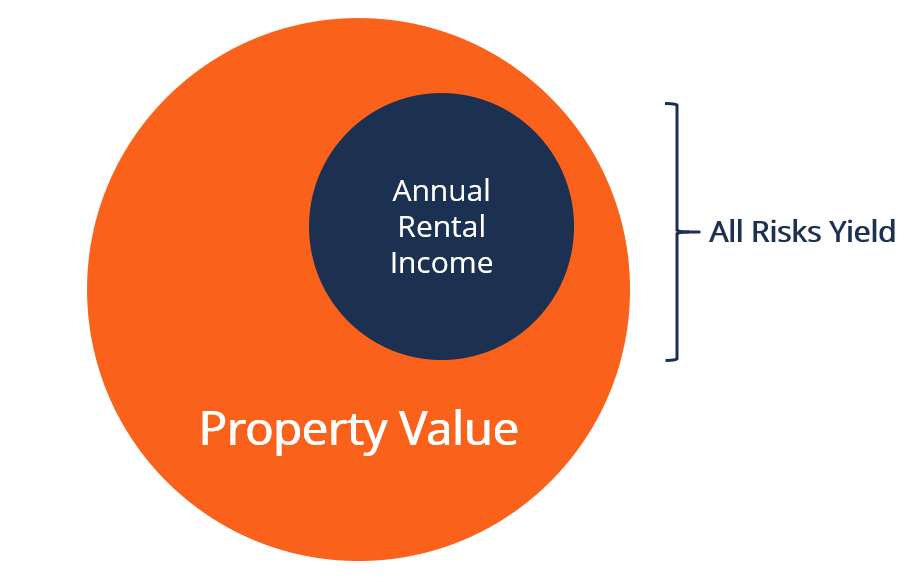

- All Risks Yield (ARY) shows the rental revenue of an investment as an annual percentage of the property cost.

- ARY is calculated by dividing the annual rental income by the property’s value and multiplying the value by 100% to get the percentage result.

- ARY is derived from comparable records and incorporates the investor’s expectations on capital growth and income.

How to Calculate All Risks Yield

The formula for calculating All Risks Yield is as follows:

Good ARY vs. Bad ARY

A good All Risks Yield is relative. To conclude that an ARY is either good or not good depends on a variety of factors. A low percentage of the ARY means that the property lacks the adequate cash flow to cater for the operational costs of running the entity, service mortgage repayments, provide for future emergencies, etc.

Higher percentages mean that the business can adequately cater for all its expenses without overburdening its cash flow. However, it’s difficult to tell whether a certain percentage points to a good or bad ARY. Nevertheless, a yield of 8% and above can be termed as the minimum adequate percentage.

Yield, Price, and Growth

The best investment choice should strike a balance between yield, price, and growth potential. A good investment property should have at least 8% ARY, a suitable geographical location, steady capital growth, and significant tenant demand. Additionally, other essential elements in real estate investment are an exit strategy, capital growth potential, tenant demand, and achievable discounts.

An exit strategy is crucial in any investment so that if it turns out otherwise than anticipated, one can leave hastily. The strategy includes investigating in detail the probable resale value of the property and the ease of a resale. If reselling the property is easy (because it is on high demand), then the exit strategy is sound.

Also, the capital growth of the property the investor intends to buy should be a key consideration. The capital growth can be retrieved from evidence on the property’s performance in the most recent earnings reports history.

Tenant demand is another crucial factor. Real demand, unlike imposed demand, should be imminent for a lucrative investment opportunity. Imposed demand means that it is short-lived, probably due to a short-lived gathering in a given location, hence raising the demand momentarily. A high genuine demand is preferred. Striking a balance between yield, price, and growth makes for a perfect investment strategy.

All Risks Yield vs. Cap Rate

Capitalization Rate is the proportion of the net operating revenue to the property value while ARY is the proportion of annual revenue to the property cost. The Cap Rate and the ARY, therefore, can be used in collaboration to determine whether an investment is profitable.

Assessors and investors require both metrics to come up with the ratios of the annual operating income compared to the value and the total costs of running the property per annum. The higher the Cap Rate and the ARY, the more favorable the investment is to the investor.

All Risks Yield vs. Net Initial Yield

The Net Initial Yield is the proportion of the rental revenue of a property to the total purchase value of the property. Unlike the ARY, the Net Initial Yield incorporates some aspects of non-recoverable costs in operations, some of which are derived from acquisition costs.

The Net Initial Yield comes with an easy calculation method and is a key indicator of performance while assessing property acquisition. It gives the assessor an upper hand in obtaining sensitive indicators of cost-effectiveness. However, the ARY is more useful in indicating the future performance of a property more than the Net Initial Yield.

The Net Initial Yield does not take into account vital assessment aspects such as the current demand situation in a rental property. Therefore, it does not enable forecasting the future performance of the property, and that’s the point where the ARY assists.

Also, the Net Initial Yield does not show current property information such as the possibility of rent increases in the future, the current condition of the premises, and probable repairs to be undertaken. Therefore, the two can be used to compare analysis for a better inference on the state of an investment opportunity.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below: