Down Payment

An initial non-refundable payment that is paid upfront for the purchase of a high-priced item

What is a Down Payment?

A down payment is an initial non-refundable payment that is paid upfront for purchasing a high-priced item – such as a car or a house – and the remaining payment is paid by obtaining a loan from a bank or financial institution. Since the customer is paying a portion of the purchase price upfront, it gives the lending institution a sense of security.

A down payment is primarily used for real estate purchases, where homebuyers pay 5%-20% of the total value of the purchase price. The balance is covered by the bank, or any financial institution, in the form of a mortgage. A down payment is also common in car purchases.

For example, a two-bedroom apartment in Toronto will cost around $1 million at an interest rate of 2.49% per year. If the builder requires the homeowners to pay a down payment of 20% or $200,000, the buyer will need to obtain a 30-year mortgage of $800,000 at an interest rate of around 2.39% per year.

Summary

- A down payment helps the buyer to obtain ownership of the property or vehicle and also helps them to reduce the monthly payment towards the mortgage principal and interest.

- The buyer can get a lower interest rate by paying a higher down payment. It is because the risk taken by the bank has been reduced with a higher down payment.

- A down payment can also impact the buyer if the property’s price goes down in the future, as the buyer may incur a loss while selling the property.

Obtaining a Good Down Payment

Below are some of the common ways that a home buyer can obtain funds for a down payment:

1. Use a tax-free savings account

The home buyer can use the money saved in a tax-free savings account towards the down payment.

2. Save systematically

Saving a fixed amount of money each month will help accumulate a substantial to put towards a down payment.

3. Borrow from family members

The home buyer can borrow money from family members and pay a higher down payment. It will allow the home buyer to secure a lower interest rate and avoid paying mortgage insurance.

4. Join a first-time home buyers program

The program provides first-time homebuyers with a percentage of the purchase price to put towards the down payment

Advantages of a Down Payment for a Home Purchase

Below are some of the advantages of providing a down payment when buying a house:

1. Lower monthly payments

Paying a high down payment will lower the amount of the mortgage/loan that needs to be taken from the bank. It results in a lower monthly installment (partial principal and interest) on the loan.

2. Avoiding private mortgage insurance

In some countries like Canada, when a buyer makes a very low down payment – 5%, for example – the bank requires them to provide a guarantee/security in case of default. Hence, the buyer needs to obtain mortgage insurance, which provides insurance to the lending institution from default by the buyer.

3. More equity in the home

A down payment of 20% would mean that the buyer owns 20% of the property, and the lending institution owns the remaining 80%.

For example – let’s say that after five years, a $100,000 home is now worth $200,000, and the buyer made a down payment of 10% ($10,000). When selling the home, the owner will need to pay back the loan of $90,000, along with interest, and will keep $110,000 as their equity amount.

Disadvantages of a Down Payment

Below are some of the disadvantages of making a down payment:

1. Less money for other costs

Paying a higher down payment means that less money will be available for other expenses, such as moving costs, renovations, or decorating the house.

2. More time to save money

Paying a down payment results in the depletion of savings, which will take some time to save once again.

3. Money tied up in equity

A down payment results in the buyer owning part of the property, which leads to profits in the future when property prices go up. However, real estate prices go up gradually, which takes a lot of time. Hence, money that could be invested in other financial products is tied up for a very long time.

Impact of Down Payment on Interest Rates

The size of the down payment impacts several factors. First, it determines whether the buyer needs to pay private mortgage insurance for paying a lower down payment. A down payment also impacts the interest rate that is provided to the buyer by the lending institution. A larger investment by the purchaser could result in a lower interest rate.

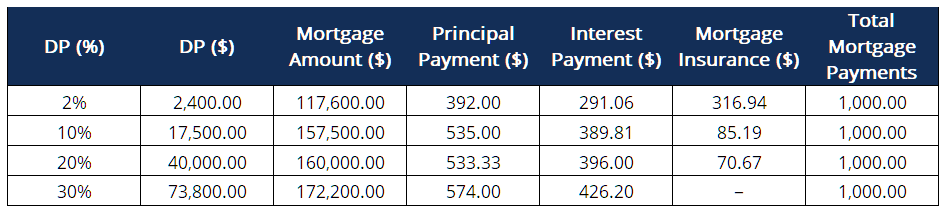

The table below shows how a higher down payment (DP) can help a buyer purchase a bigger house.

If a buyer wants to make a monthly payment of $1,000 towards the mortgage (25-year mortgage at 2.97% per annum), with a down payment of 2% or $2,400, they will be able to afford a house costing $117,600. Because of the lower down payment, they will be expected to pay mortgage insurance of around $316.94.

However, with a higher down payment, not only does the mortgage amount go down and become zero with a 30% or more down payment, the value of the house that they can afford also goes higher.

The example above clearly shows the importance of paying a higher down payment.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: