Get In-Demand Finance Certifications

A digital database of transactions shared by a network of users

A blockchain is digital database of transactions that is maintained by a network of computer servers, who can all easily verify and agree on the contents of the database in a way that makes it difficult for anyone to hack or change.

Each one of these users, called a node, stores a copy of the blockchain database (also called a digital ledger). Any new entries to this digital ledger must be first agreed upon before being added to the blockchain. Any blocks that are not agreed upon will not be added to the blockchain and discarded instead.

Once added, new version of the digital ledger is sent to all nodes. As the digital ledger is held by all nodes, it makes it very difficult to tamper with the blockchain and even harder to go back.

The technology was developed to allow a secure way for two parties to deal directly with each other without the need for a third party in between to intermediate. As there isn’t a centralized party, such as a bank or financial institution, that keeps the sole copy of the ledger, you will also hear that blockchains are known as distributed ledgers.

Blockchain is currently predominantly used in cryptocurrency networks. This technology was popularized with the advent of Bitcoin, but is used by all cryptocurrencies to ensure security and transparency. Other cryptocurrencies, like Ethereum, have made changes to their blockchain network by adding features such as Smart Contracts and Decentralized Applications (DApps).

Blockchains can also be for a variety of purposes, such as issuing and maintaining real estate titles and records, medical record keeping, tracking produce, livestock and medicine throughout the supply chain, verifying ownership or validity of assets or rights, trade finance and even voting mechanisms.

Blockchains can be understood as something simple, like an analogy of an on-line purchase, say from Amazon.

After your purchase, you will receive an order confirmation on your email. Then, you might next receive an email confirmation that your order has been processed. The next email after that might be your order has left the warehouse and has been shipped. You might then get another email tracker that says your purchase is en route. Finally, you might get that last email that your purchase has been delivered to your door by the delivery person.

That’s basically how a blockchain works. Each one of those emails or notifications you received from Amazon has been triggered each time it passes through a step and each time it does that, the action causes the order tracker to update the status of your purchase. You can also log into your Amazon account and verify each of those steps.

The chain works in one direction only via a time-stamp, just like your Amazon order tracker, which means that no one can go back and tamper with earlier steps so the delivery person can’t go back and status the order to steal your purchase. This type of sequence is also called “append-only”.

Think of each of the emails in the above example as a discrete block and the entire order process as a “mini”-blockchain.

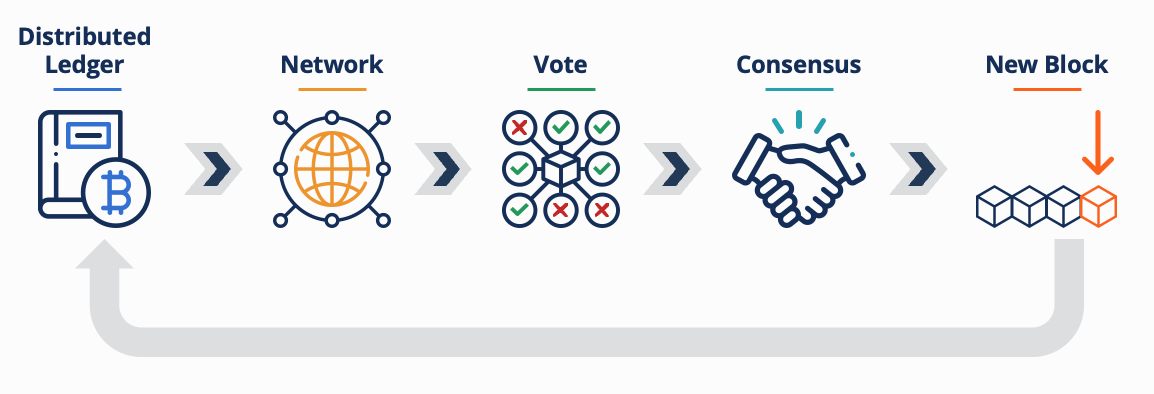

A blockchain is simply a database of transactions, often called a distributed ledger, that has been duplicated and broadcast to network of users, who can all verify and agree on the database.

Each new block, which in cryptocurrencies contains a list of transactions, that comes afterwards is time-stamped and has to be approved by a network of computer servers, called nodes, each of whom checks its validity.

Once every node has checked a block, there is a sort of electronic vote, as some nodes may think the transaction is valid and others think it is a fraud. This is called consensus.

If a majority of nodes say that a block is valid, then it is written into the blockchain, literally stringing together a chain of blocks. This new accepted version of the blockchain ledger is broadcast over the entire network of nodes that run the same blockchain software. All the nodes have the same copy and then the process repeats again to verify the next block to add onto the chain.

As more blocks are added, the transaction becomes increasingly difficult to reverse or alter, making the blockchain tamper-resistant, but not tamper-proof.

Old blocks cannot be modified without also changing the data in subsequent blocks that follow it in the chain. Furthermore, all computers in the network must agree to change this old block. This is what prevents fraudulent data.

If a counterfeiter attempts to create a fake record of cryptocurrency, the computers in the network will disagree with the change in an old block. The fake record will be invalid and not recorded in the network.

In certain cryptocurrencies such as Bitcoin, the blockchain technology depends on nodes to race in search for a correct answer to a complicated computation in order to earn the right to ‘validate’ or add the block to the blockchain. This process is called “proof of work.”

The first node to solve the computation and validate the block is also rewarded with new Bitcoins (where the term Bitcoin “mining” comes from) and the difficulty of solving these computations increases over time. The act of mining, thus, involves offering your computing power to the network in exchange for some cryptocurrency.

Different cryptocurrencies have different verification and recording protocols. Because of this, the computing power and hardware required for each block network can differ. Additionally, the confirmation speeds for transactions under different cryptocurrencies can also differ.

Bitcoin confirmations may take anywhere between 10 minutes to an hour or more per confirmation. In contrast, Ethereum confirmations are generally much quicker – in the order of around 15 seconds or so.

Newer blockchains, such as Ripple’s XRP Ledger, only require 3 to 6 seconds for transactions to be sorted, agreed, and added to the blockchain, even for payments internationally.

Different cryptocurrency blockchains also have different throughput, called scale. While Bitcoin’s blockchain is only capable of processing 7-10 transactions per second, Ripple can process more than 1,500 transactions per second.

When it comes to cryptocurrencies, an important distinction is that the digital asset is actually never held by the owner but rather remains on the blockchain. The proof of ownership of the cryptocurrency is in the form of your private key, which is created when you create your account. Your private key is stored on a digital cryptocurrency wallet, which will also have a public key, which is a string of numbers and letters. It is an address that will appear within the blockchain as your transactions take place—no visible records of who did what transaction with who, only the number of a wallet.

The concept of blockchain technology first appeared in David Lee Chaum’s Berkeley PhD dissertation in 1982 entitled ”Computer Systems Established, Maintained and Trusted by Mutually Suspicious Groups”[1]. However, blockchains came to the forefront in 2008 in the Bitcoin whitepaper published pseudonymous Satoshi Nakamoto titled “Bitcoin: A Peer-to-Peer Electronic Cash System”[2].