Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

A mathematical formula used to determine the conditional probability of events

In statistics and probability theory, the Bayes’ theorem (also known as the Bayes’ rule) is a mathematical formula used to determine the conditional probability of events. Essentially, the Bayes’ theorem describes the probability of an event based on prior knowledge of the conditions that might be relevant to the event.

The theorem is named after English statistician, Thomas Bayes, who discovered the formula in 1763. It is considered the foundation of the special statistical inference approach called the Bayes’ inference.

Besides statistics, the Bayes’ theorem is also used in various disciplines, with medicine and pharmacology as the most notable examples. In addition, the theorem is commonly employed in different fields of finance. Some of the applications include but are not limited to, modeling the risk of lending money to borrowers or forecasting the probability of the success of an investment.

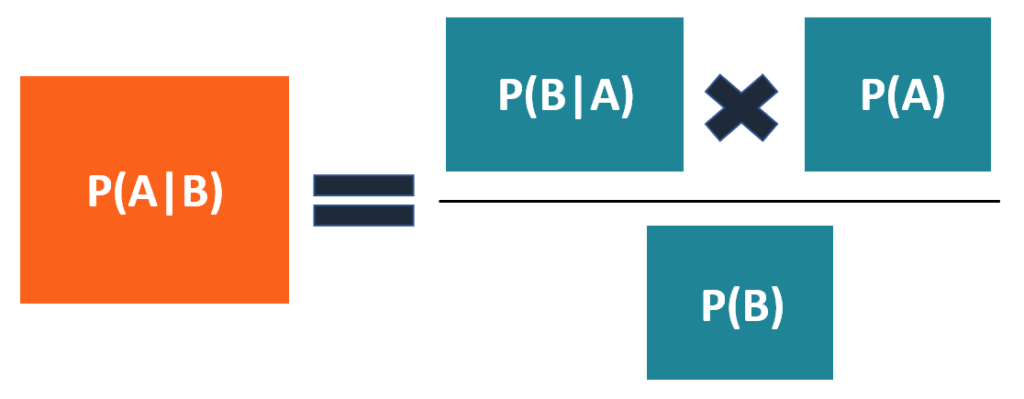

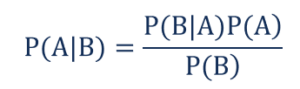

The Bayes’ theorem is expressed in the following formula:

Where:

Note that events A and B are independent events (i.e., the probability of the outcome of event A does not depend on the probability of the outcome of event B).

A special case of the Bayes’ theorem is when event A is a binary variable. In such a case, the theorem is expressed in the following way:

Where:

In the special case above, events A– and A+ are mutually exclusive outcomes of event A.

Imagine you are a financial analyst at an investment bank. According to your research of publicly-traded companies, 60% of the companies that increased their share price by more than 5% in the last three years replaced their CEOs during the period.

At the same time, only 35% of the companies that did not increase their share price by more than 5% in the same period replaced their CEOs. Knowing that the probability that the stock prices grow by more than 5% is 4%, find the probability that the shares of a company that fires its CEO will increase by more than 5%.

Before finding the probabilities, you must first define the notation of the probabilities.

Using the Bayes’ theorem, we can find the required probability:

Thus, the probability that the shares of a company that replaces its CEO will grow by more than 5% is 6.67%.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Bayes’ Theorem. To keep learning and advancing your career, the following resources will be helpful: