Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

The discount rate that equates a project’s present value cash flows to its initial investment

In many areas of finance, where investors and other stakeholders often make decisions based on profitability and returns, it’s critical to accurately assess how well investments, investment strategies, and portfolios are performing. A key skill for this assessment is being able to calculate what is called the “weighted return” of an investment.

The purpose of calculating a weighted return is to assess the true performance of an investment, considering both the timing and size of cash flows. In this article, we explore the two primary types of weighted returns — Money Weighted Rate of Return (MWRR or just money weighted return) and Time Weighted Return (TWR) — to discuss their significance and provide clarity in navigating the complex landscape of investment evaluation.

The fundamental concept that underpins both the money weighted rate of return and time weighted return is the time value of money (TVM). The TVM asserts that the value of money changes over time due to factors such as inflation, interest rates, and investment opportunities. To accurately assess the profitability of an investment, it is important to consider the timing of cash flows and the associated opportunity costs.

Discount rates play a pivotal role in the TVM. These rates, often influenced by prevailing interest rates and the perceived risk of an investment, help determine the present value of future cash flows. Net Present Value (NPV) is a metric derived from discounting future cash flows to their present values. A positive NPV indicates a potentially profitable investment, while a negative NPV suggests the opposite.

The Internal Rate of Return (IRR) is the discount rate that makes the NPV of an investment zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

Weighted returns, both money weighted and time weighted, are metrics designed to evaluate the performance of investment portfolios. These returns account for the impact of cash inflows and outflows, acknowledging that the timing of these transactions can significantly affect the overall return.

Understanding the significance of weighted returns is crucial for investors seeking a comprehensive assessment of their investment or portfolio performance. Unlike simple returns, which only consider the beginning and ending values of an investment, weighted returns provide a more nuanced perspective by factoring in the influence of cash outflows and cash inflows.

As previously highlighted, there are two primary types of weighted returns: money weighted rate of return and time weighted return. Both metrics cater to different aspects of investment performance evaluation.

Money weighted rate of return is equivalent to the internal rate of return (IRR) and accounts for the impact of cash flows on a portfolio’s performance.

The money weighted rate of return takes into consideration the size and timing of cash inflows and outflows, providing a more personalized measure of an investor’s experience with a particular investment.

On the other hand, the time weighted return isolates the impact of external cash flows by measuring the compound rate of growth in a portfolio over a specific period instead. TWR is more focused on the fund manager’s performance, excluding the influence of investor behavior.

Let’s look at a couple of examples to demonstrate.

An investment manager purchases a stock today for $100. He intends to hold the stock for three years and collects $5 in dividends each year. At the end of the third year, he expects to be able to sell the stock for $150. What is the money weighted return on this investment portfolio?

Step 1: Identify inflows and outflows

Inflows: Dividends ($5 in Years 1, 2, and 3) and the sale of stock ($150 in Year 3). Outflows: Purchase of stock (Year 0).

Step 2: Set PV inflows = PV outflows

Step 3: Solve for r

Using a financial calculator, Goal Seek in Excel, or through trial and error, we arrive at a value for the money weighted rate of return of approximately 18.88%.

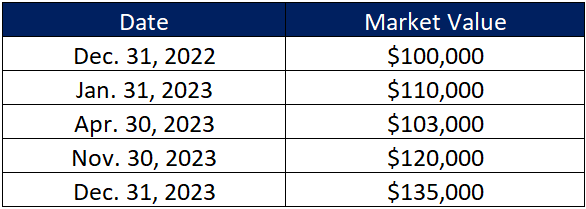

The table below describes the market value of a certain portfolio at different dates:

We also learn that the client made a $12,000 withdrawal on March 3, 2023, and a $20,000 deposit on December 20, 2023. What is the time weighted return of this investment portfolio?

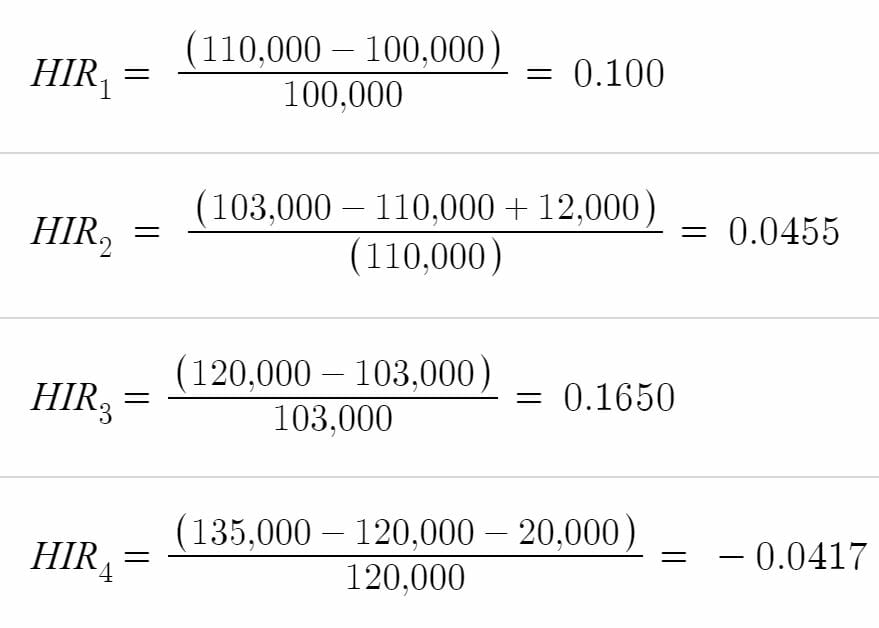

Step 1: Identify all holding intervals

Based on the given information, there are four holding intervals (HIs):

Step 2: Identify all withdrawals and deposits

Step 3: Calculate the holding interval return (HIR) for each interval

Step 4: Add 1 to HIRs, multiplying them together, then subtracting 1

![]()

Step 5: Annualize returns

The data provided above is for one year; thus, there is no need to conduct the annualization calculation. Therefore, the time weighted return on this portfolio is 28.40%.

One key distinction between MWRR and TWR lies in their sensitivity to the timing of cash flows. MWRR can be heavily influenced by the timing of large cash inflows or large cash outflows, making it more volatile than TWR. TWR, being less sensitive to cash flow timing, provides a clearer picture of the investment manager’s skill.

Another critical difference concerns investor behavior. MWRR reflects the actual experience of an investor, incorporating the impact of their buying and selling decisions. In contrast, TWR measures the pure performance of the investment itself, offering a more objective evaluation.

The choice between MWRR and TWR depends on the specific objectives of the evaluation. If the goal is to assess the investor’s experience and the impact of their cash flows, MWRR is more suitable. On the other hand, for evaluating the investment manager’s skill and the investment’s inherent performance, TWR provides a clearer picture.

MWRR reflects the investor’s actual experience, taking into account the timing and size of cash flows. TWR, on the other hand, isolates external factors to evaluate the investment’s pure performance.

Weighted returns find applications in various investment scenarios. MWRR is often employed in assessing the performance of individual investors, especially in the context of personal investment decisions and the timing of contributions or withdrawals.

TWR, being more focused on investment managers, is widely used in the institutional investment space to evaluate the performance of mutual funds, hedge funds, and other professionally managed portfolios.

Selecting the right return measure is crucial for obtaining a comprehensive understanding of investment performance. Investors and fund managers should carefully consider their objectives and the nature of their portfolio when choosing between MWRR and TWR. By aligning the chosen metric with the intended evaluation criteria, stakeholders can make more informed decisions, leading to better-informed investment.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

To keep learning and advance your career, the following resources will be helpful: