Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An American style call option to buyback a convertible bond

The term ASCOT is short for Asset Swapped Convertible Option Transaction. It is an American-style call option to buy back a convertible bond. It falls under the category of financial products called structured products, which are a combination of two or more financial products combined to meet the needs of the buyer.

The purpose of using an ASCOT is to separate the two risk components of a convertible bond – equity and credit. The coupon payments from the convertible bond constitute the credit or fixed income part of a convertible bond, while the option to convert to shares of the issuing company is the equity part.

If an investor in a convertible bond wishes to hold onto the equity part but wants some extra cash, they can initiate an ASCOT with a financial institution.

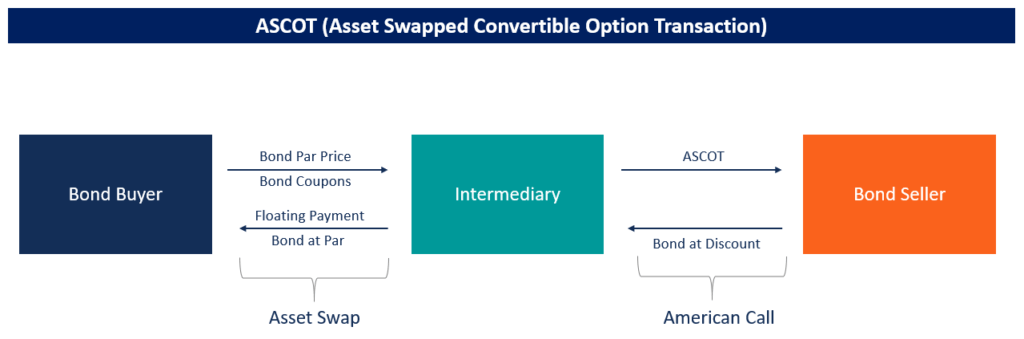

An ASCOT comprises two parts – an American call with a floating strike price and an asset swap.

An American call option is the right to buy the underlying asset at a given price anytime during the life of the option. In the case of an ASCOT, the American call option is on the reference convertible bond.

An ASCOT buyer owns the right to buy back the convertible bond when they wish to convert it to equity, but they must agree to a floating strike price to buy back the bond. A floating strike implies that the strike is determined at the time when the owner of the option decides to exercise.

An asset swap involves swapping an underlying asset for cash and exchanging cash flows to maintain exposure to the asset. In an asset swap, the owner of a convertible bond acts as a swap seller and sells the convertible bond at par to the swap buyer.

The asset swap is structured so that one party exchanges the bond’s fixed coupon payments for a floating-rate stream based on a market benchmark such as SOFR, plus an asset swap spread (ASW).

The ASW is based on the credit and liquidity risk of the underlying bond. This structure allows one party to retain economic exposure to the bond’s credit risk without holding the bond directly.

Assume a fixed income strategy fund owns a convertible bond that they do not want to carry on its balance sheet. On the other hand, they wish to continue to have exposure to the bond. To accomplish this task, they can initiate an ASCOT with a financial institution, which will be the intermediary in the transaction.

The ASCOT buyer is the bond seller. They sell the bond to the intermediary financial institution in exchange for an option to buy back the bond at a future date. This way, they can have exposure to the equity part of the convertible bond by being able to buy the bond back when they want to convert to equity.

The buyer also incurs reduced balance sheet risk, as they do not need to mark-to-market the value of the bond.

The bond buyer is another investor who likes to invest in the credit-only part of the convertible bond. The investor enters an asset swap with an intermediary institution, where they buy the bond at par and pass on the coupon payments to the intermediary or swap seller.

In exchange, the bond buyer receives a floating-rate payment based on a market benchmark such as the Secured Overnight Financing Rate (SOFR), plus an asset swap spread. The spread reflects the credit risk and liquidity profile of the convertible bond and is set by market pricing.

The net present value of this asset swap is used to determine the price that the ASCOT buyer receives for the convertible bond.

A financial intermediary is a counterparty between the bond seller and the bond buyer. They buy the bond at a discount to par from the ASCOT buyer – the discount to the price is determined by the net present value of the asset swap between the intermediary and the bond buyer.

This discount acts as a premium paid by the ASCOT buyer for the option to buy back the underlying convertible bond. The intermediary then enters into an asset swap transaction with the credit buyer, where they sell the bond to the buyer at par and exchange payments as described in the asset swap section above.

An ASCOT can be valued using a tree model in the same way as options since an ASCOT is essentially an option to buy back the convertible bond. It involves constructing three trees – one for the stock price to account for if the bond will be called, the second one for valuing the convertible bond, and a third one for the ASCOT.

The three-layered model above is similar to option tree models for options, where a tree for the underlying stock is created, and the option valuation tree is layered on top of it.

The risk management for an ASCOT is similar to managing options. The risk is managed using Greeks, just like in options. In the case of an ASCOT, the two most important greeks are the delta and the rho.

Delta measures the sensitivity of the ASCOT value to the underlying stock price, while the rho measures the sensitivity to interest rates.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA®) certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: