Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

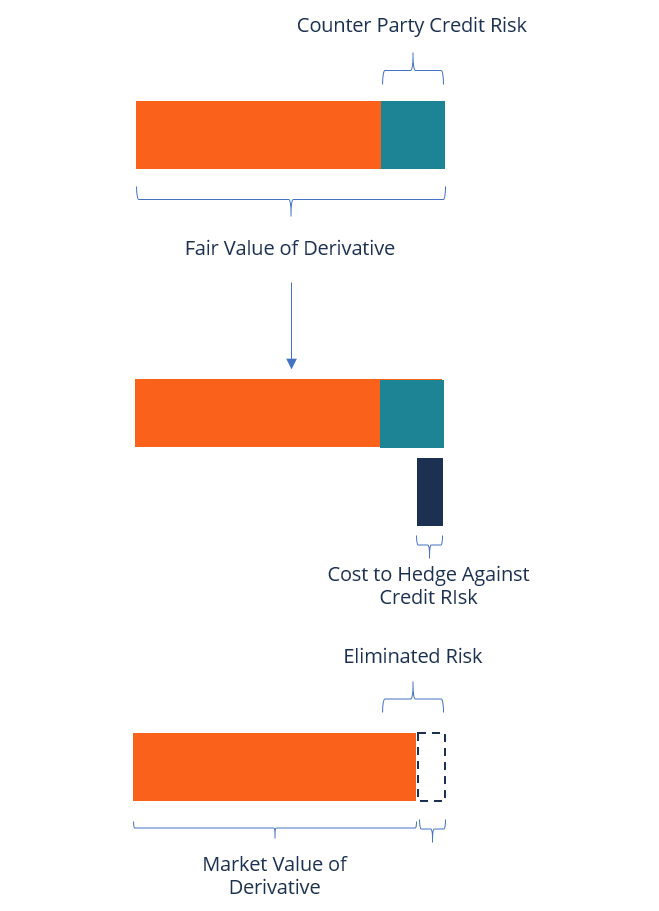

The price that an investor would pay to hedge the counterparty credit risk of a derivative instrument

Credit Valuation Adjustment (CVA) is the price that an investor would pay to hedge the counterparty credit risk of a derivative instrument. It reduces the mark-to-market value of an asset by the value of the CVA.

Credit Valuation Adjustment was introduced as a new requirement for fair value accounting during the 2007/08 Global Financial Crisis. Since its introduction, it has attracted dozens of derivatives market participants, and most of them have incorporated CVA in deal pricing.

The formula for calculating CVA is written as follows:

Where:

The concept of credit risk management, which includes credit valuation adjustment, was developed due to the increased number of country and corporate defaults and financial fallouts. In recent times, there have been cases of sovereign entity defaults, such as Argentina (2001) and Russia (1998). At the same time, a high number of large companies collapsed before, during, and after the financial crisis of 2007/08, including WorldCom, Lehman Brothers, and Enron.

Initially, research on credit risk focused on identifying it. Specifically, the focus was on counterparty credit risk, which refers to the risk that a counterparty may default on its financial obligations.

Prior to the 2008 financial crisis, market participants treated large derivative counterparties as too big to fail and, therefore, never considered their counterparty credit risk. The risk was often ignored due to the high credit rating of counterparties and the small size of derivative exposures. The assumption was that counterparties could not default on their financial obligations, unlike other parties.

However, during the 2008 Global Financial Crisis, the market experienced dozens of corporate collapses, including large derivative counterparties. As a result, market participants started incorporating credit valuation adjustment when calculating the value of over-the-counter derivative instruments.

Derivative instruments can be classified as either unilateral or bilateral, depending on the nature of the payoff.

For a unilateral derivative instrument holder, exposure to loss occurs if a counterparty defaults on their financial obligations. The amount of loss that an investor incurs is equal to the fair value of the instrument at the time of default.

Bilateral derivatives are more complex than unilateral derivatives, since the former includes two-way counterparty risk. This means that both the counterparty and the investor are exposed to counterparty risk. The advantage of bilateral derivatives is that the derivative may adopt an asset or liability position at any valuation date.

For example, if Counterparty A is at a positive asset position today, it is exposed to Counterparty B. If A defaults on his obligation, he will owe the positive asset to B. The same applies if B is in a negative liability position because, in case of default, he owes the negative liability position to A.

There are several methods used to value derivatives, ranging from simple to advanced. Determining the credit valuation adjustment method to use depends on the organization’s sophistication and resources available to the market participants.

The simple method calculates the instrument’s mark-to-market value. The calculation is then repeated to adjust the discount rates by the counterparty’s credit spread. Calculate the difference between the two resulting values to obtain the credit valuation adjustment.

The swaption-type is a more complex credit valuation adjustment methodology that requires advanced knowledge of derivative valuations and access to specific market data. It uses the counterparty credit spread to estimate the asset’s replacement value.

Simulation modeling involves simulating market risk factors and their scenarios. The derivatives are then revalued using multiple simulation scenarios. The expected exposure profile of each counterparty is determined by aggregating the resulting matrix. Each counterparty’s expected exposure profile is adjusted to derive the collateralized expected exposure profile.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Credit Valuation Adjustment (CVA). To keep learning and advancing your career, the following resources will be helpful: