Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The exchange of principal and interest between counterparties for cheaper foreign rates

A foreign exchange swap (also known as an FX swap) is an agreement to simultaneously borrow one currency and lend another at an initial date, then exchanging the amounts at maturity. It is useful for risk-free lending, as the swapped amounts are used as collateral for repayment.

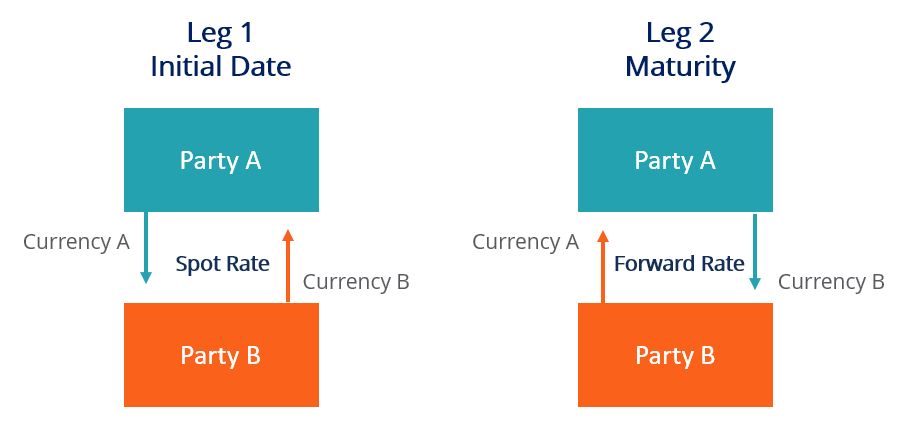

For a foreign exchange swap to work, both parties must own a currency and need the currency that the counterparty owns. There are two “legs”:

The first leg is a transaction at the prevailing spot rate. The parties swap amounts of the same value in their respective currencies at the spot rate. The spot rate is the exchange rate at the initial date.

The second leg is a transaction at the predetermined forward rate at maturity. The parties swap amounts again, so that each party receives the currency they loaned and returns the currency they borrowed.

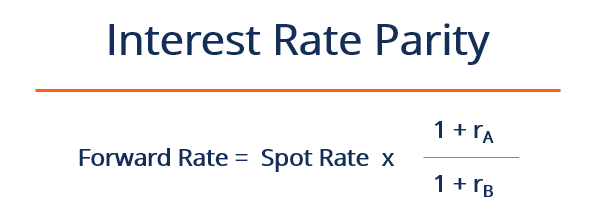

The forward rate is the exchange rate on a future transaction, determined between the parties, and is usually based on the expectations of the relative appreciation/depreciation of the currencies. Expectations stem from the interest rates offered by the currencies, as demonstrated in the interest rate parity. If currency A offers a higher interest rate, it is to compensate for expected depreciation against currency B and vice versa.

Foreign exchange swaps are useful for borrowing/lending amounts without taking out a cross-border loan. It also eliminates foreign exchange risk by locking in the forward rate, making the future payment known.

Party A is Canadian and needs EUR. Party B is European and needs CAD. The parties enter into a foreign exchange swap today with a maturity of six months. They agree to swap 1,000,000 EUR, or equivalently 1,500,000 CAD at the spot rate of 1.5 EUR/CAD. They also agree on a forward rate of 1.6 EUR/CAD because they expect the Canadian Dollar to depreciate relative to the Euro.

Today, Party A receives 1,000,000 Euros and gives 1,500,000 Canadian Dollars to Party B. In six months’ time, Party A returns 1,000,000 EUR and receives (1,000,000 EUR * 1.6 EUR/CAD = 1,600,000 CAD) from Party B, ending the foreign exchange swap.

Short-dated foreign exchange swaps refer to those with a maturity of up to one month. The FX market uses different shorthands for short-dated FX swaps, including:

Foreign exchange swaps and cross currency swaps are very similar and are often mistaken as synonyms.

The major difference between the two is interest payments. In a cross currency swap, both parties must pay periodic interest payments in the currency they are borrowing. Unlike a foreign exchange swap where the parties own the amount they are swapping, cross currency swap parties are lending the amount from their domestic bank and then swapping the loans.

Therefore, while foreign exchange swaps are riskless because the swapped amount acts as collateral for repayment, cross currency swaps are slightly riskier. There is default risk in the event the counterparty does not meet the interest payments or lump sum payment at maturity, meaning the party cannot pay their loan.

Thank you for reading CFI’s guide on Foreign Exchange Swap. To keep learning and advance your career, the following resources will be helpful: