Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The act of acquiring funds from outside the country’s borders

Cross-border financing is the process of sourcing funds from outside the home country’s border. It is useful for multinational businesses to conduct international trade without needing to hold a large reserve of working capital.

Cross-border loans work similarly to regular loans – the difference is exposure to two currencies instead of one.

Letters of credit are a guarantee between the buyer, seller, and bank. When the previously agreed-upon conditions are met (such as the seller shipping the merchandise), the seller is guaranteed to be paid. If the borrower defaults on payments, the bank steps in to pay the outstanding amount owed.

LOCs are useful to mitigate the default risk of counterparties, especially in the international business context, where it is harder to personally gauge the creditworthiness of the parties to the contract.

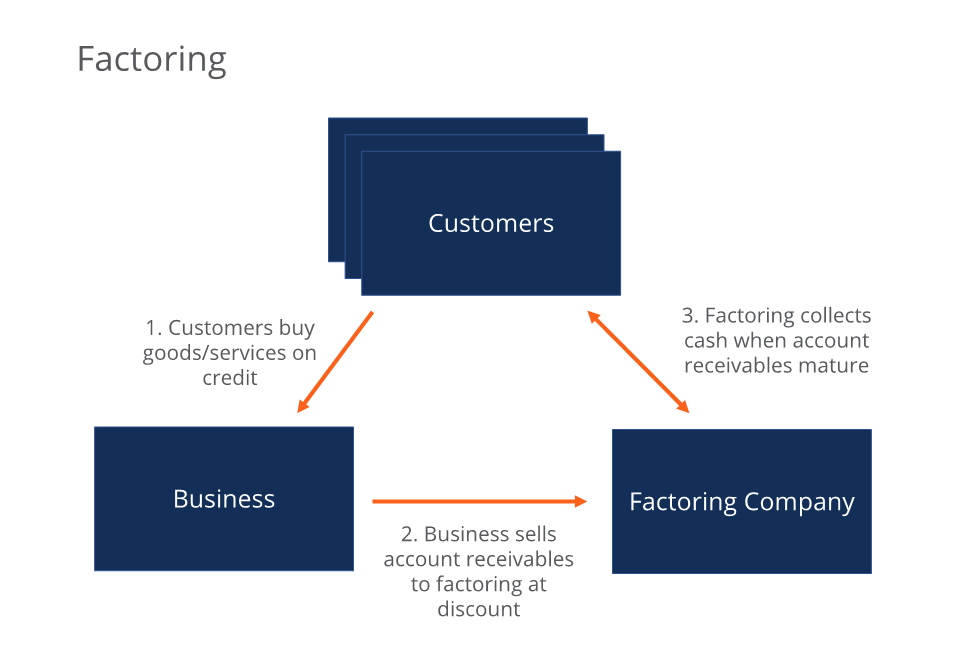

In cross-border factoring, a factoring company buys the business’ accounts receivable in the foreign currency at a discount. The risk of bad debt expense (customers not fulfilling their accounts receivable) is shifted to the factoring company, which makes a profit between the discounted value they pay to the business, minus any bad debt expenses.

Cross-border factoring is useful for businesses that wish to receive immediate cash flows to pay outstanding debt obligations, operating expenses, and investments for growth.

Due to the foreign jurisdiction, borrowers are faced with different laws and tax consequences.

Borrowers are subject to foreign currency exposure due to the fluctuating nature of the exchange rate.

For businesses in foreign countries that are politically unstable, there is uncertainty regarding disruptions in business operations due to events such as riots & coups, regulatory changes, government intervention, and more.

For any debt or loan, default risk is an important factor to consider. The creditworthiness of the business (and end customers in factoring) are crucial in determining whether to lend and at what rate.

It is common for borrowers to hire an expert team of accountants and lawyers to determine ways to minimize taxes and legal risks. Currency risk can be hedged with derivatives such as options.

For lenders, they can determine if they are willing to accept the risks associated with each case. There are two ways they can manage risks:

Lenders can price in the risks by increasing their interest rates. As a general rule, a higher risk is compensated by higher returns. In the case of factoring, lenders can discount the value paid for the accounts receivable.

Lenders can decrease risks by requiring collateral or recourse. With collateral, the lender can legally take the collateralized asset if the lender fails to make their payments. With recourse, the lender can go after other assets of the lender that were not collateralized. Alternatively, lenders can buy insurance in case the borrower defaults.

The cross-border financing market has grown remarkably over the years, with $7 trillion outstanding loans worldwide. The increase can be attributed to multiple intertwined factors. The improvement of IT and globalization of business has greatly driven demand.

Furthermore, emerging markets seeking to penetrate the global market need capital to grow. Due to the political instability and currency risk of emerging markets, lenders get higher returns, which is attractive to those who prefer higher risk and returns.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: