Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

How businesses account for a receivable account that will not be paid

Bad debt expense is the way businesses account for a receivable account that will not be paid. Bad debt arises when a customer either cannot pay because of financial difficulties or chooses not to pay due to a disagreement over the product or service they were sold.

Bad debt can be reported on the financial statements using the direct write-off method or the allowance method.

The direct write-off method involves writing off a bad debt expense directly against the corresponding receivable account. Therefore, under the direct write-off method, a specific dollar amount from a customer account will be written off as a bad debt expense.

However, the direct write-off method can result in misstating the income between reporting periods if the bad debt journal entry occurred in a different period from the sales entry. For such a reason, it is only permitted when writing off immaterial amounts. The journal entry for the direct write-off method is a debit to bad debt expense and a credit to accounts receivable.

The allowance method estimates bad debt expense at the end of the fiscal year, setting up a reserve account called allowance for doubtful accounts. Similar to its name, the allowance for doubtful accounts reports a prediction of receivables that are “doubtful” to be paid.

In contrast to the direct write-off method, the allowance method is only an estimation of money that won’t be collected and is based on the entire accounts receivable account. The amount of money written off with the allowance method is estimated through the accounts receivable aging method or the percentage of sales method. An example of an allowance method journal entry can be found below.

Entry 1: The amount of bad debt is estimated using the accounts receivable aging method or percentage of sales method and is recorded as follows:

Entry 2: When a specific receivables account is deemed to be uncollectible, allowance for doubtful accounts is debited and accounts receivable is credited.

The amount of bad debt expense can be estimated using the accounts receivable aging method or the percentage sales method.

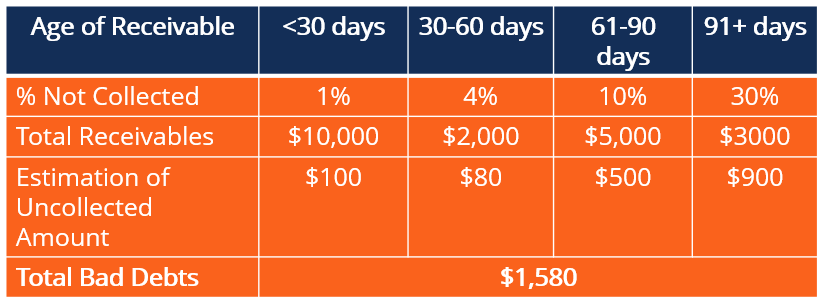

The accounts receivable aging method groups receivable accounts based on age and assigns a percentage based on the likelihood to collect. The percentages will be estimates based on a company’s previous history of collection.

The estimated percentages are then multiplied by the total amount of receivables in that date range and added together to determine the amount of bad debt expense. The table below shows how a company would use the accounts receivable aging method to estimate bad debts.

The percentage of sales method simply takes the total sales for the period and multiplies that number by a percentage. Once again, the percentage is an estimate based on the company’s previous ability to collect receivables.

For example, if a company with sales of $2,000,000 estimates that 2% of sales will be uncollectible, their bad debt expense would be $40,000 ($2,000,000 * 0.02).

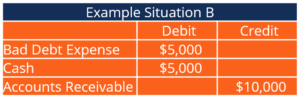

Consider a roofing business that agrees to replace a customer’s roof for $10,000 on credit. The project is completed; however, during the time between the start of the project and its completion, the customer failed to fulfill their financial obligation.

The original journal entry for the transaction would involve a debit to accounts receivable, and a credit to sales revenue. Once the company becomes aware that the customer will be unable to pay any of the $10,000, the change needs to be reflected in the financial statements.

Therefore, the business would credit accounts receivable of $10,000 and debit bad debt expense of $10,000. If the customer is able to pay a partial amount of the balance (say $5,000), it will debit cash of $5,000, debit bad debt expense of $5,000, and credit accounts receivable of $10,000.

Fundamentally, like all accounting principles, bad debt expense allows companies to accurately and completely report their financial position. At some point in time, almost every company will deal with a customer who is unable to pay, and they will need to record a bad debt expense. A significant amount of bad debt expenses can change the way potential investors and company executives view the health of a company.

For the above-mentioned reasons, it is critical that bad debts are recorded timely and accurately. In addition, they help companies recognize customers who defaulted on payments to avoid similar situations in the future.

Additionally, bad debt expense does comes with tax implications. Reporting a bad debt expense will increase the total expenses and decrease net income. Therefore, the amount of bad debt expenses a company reports will ultimately change how much taxes they pay during a given fiscal period.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Bad Debt Expense. To keep advancing your career, the additional resources below will be useful: