Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A derivative contract between two counterparties to transfer inflation risk by exchanging fixed cash flows

An inflation swap is a derivative contract between two counterparties to transfer inflation risk by exchanging fixed cash flows. The mechanics involve one party paying fixed payments, while the other makes payments based on the floating rate on an inflation index.

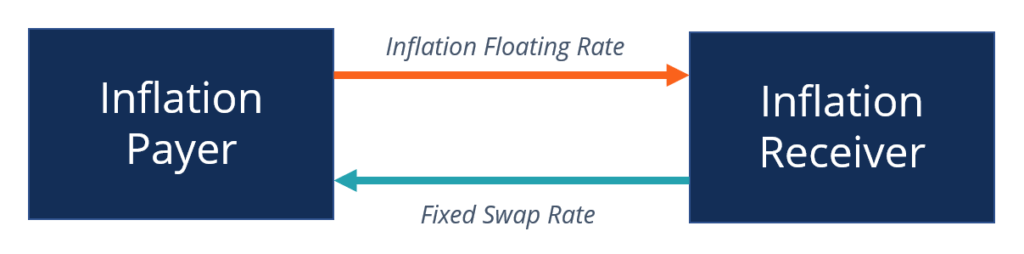

Inflation swaps are a type of swap contract used specifically to transfer inflation risk. One party to the contract seeks to reduce their risk (by hedging), while the other increases exposure to the risk (by speculating).

The party looking to hedge their inflation risk pays the floating rate linked to an inflation index – such as the Consumer Price Index (CPI) – while receiving fixed cash flows. By swapping floating for fixed, it reduces the hedging party’s exposure to inflation risk and increases their certainty of future cash flows.

The counterparty that believes that inflation will rise will agree to pay fixed-rate cash flows in exchange for receiving the floating rate cash flows. The speculating party increases their inflation risk, which will pay off if the inflation rate rises above the fixed rate they agreed to swap.

Before the start of the contract, the parties must agree on the terms. They choose a notional amount – the principal amount from which cash flows are calculated but usually not exchanged. They also determine a maturity date and the fixed rate to be exchanged. Both parties put up collateral to prevent counterparty default risk.

The most common form of inflation swap is zero-coupon, whereby a lump sum payment on the notional amount is exchanged only at maturity. Swaps with coupon payments (cash flow over the duration) are more common with other types of swaps, such as interest rate swaps or cross currency swaps.

Unlike other financial derivatives traded on an exchange, swaps are traded over-the-counter (OTC), meaning that parties can customize specific details of the contract to better suit their needs. Swaps also usually involve a swap bank that acts as an intermediary to help find the parties and facilitate the swap. In return for its services, the swap bank takes a premium from both parties.

Swaps can be terminated before the stated maturity date by calculating the market value and buying out the counterparty. At the start of the contract, the terms are based on the current market conditions at the time, so its initial value is at par. As time goes on and inflation changes, the market value of the positions to the contract changes positively or negatively.

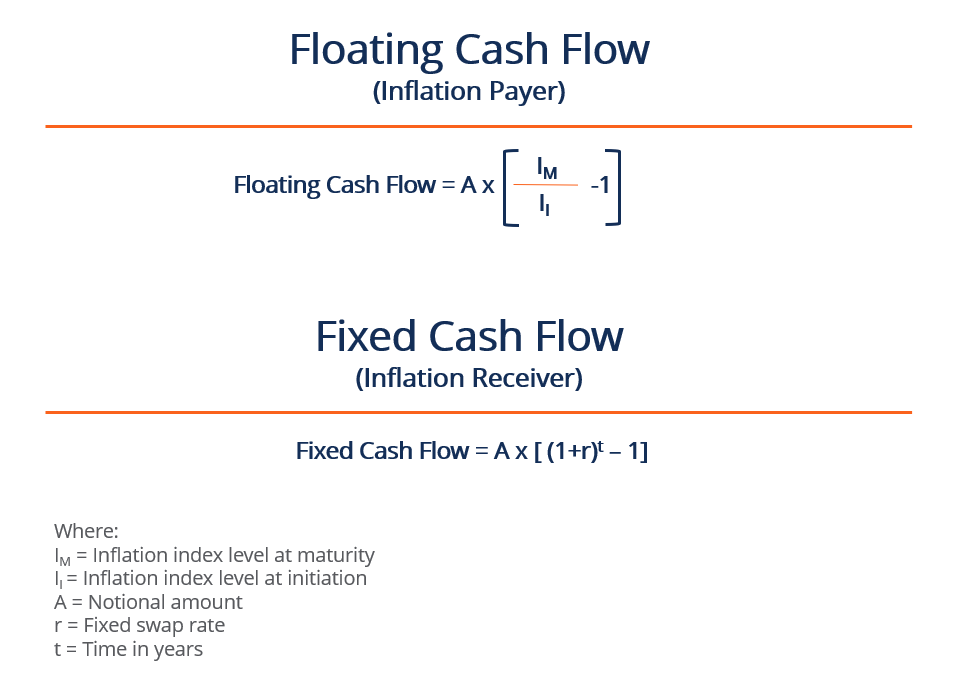

Two parties enter into a zero-coupon inflation swap. They agree on a 2% fixed rate and a floating rate linked to the CPI. The contract’s notional amount is $10M and a maturity date of five years from today. At inception, the CPI level is at 128.

At maturity, the parties swap the lump sum cash flow. Suppose that the CPI rose to 139.

The inflation payer must pay cash flow on the floating rate: 10M x [(139/128) – 1] = $859,375

The inflation receiver must pay cash flow on the fixed swap rate: 10M x [(1+0.02)5 – 1) = $1,040,808

In this scenario, the inflation payer benefits from the swap because the inflation rate cash flow they are paying is less than the fixed-rate cash flow they are receiving.

In an alternate scenario, suppose that the CPI rose to 143 instead.

The inflation payer pays cash flow: 10M x [(143/128) – 1] = $1,171,875

The inflation receiver’s cash flow remains the same: $1,040,808

Because the CPI index rose above the fixed swap rate, the inflation receiver benefits from the swap contract.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: