Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

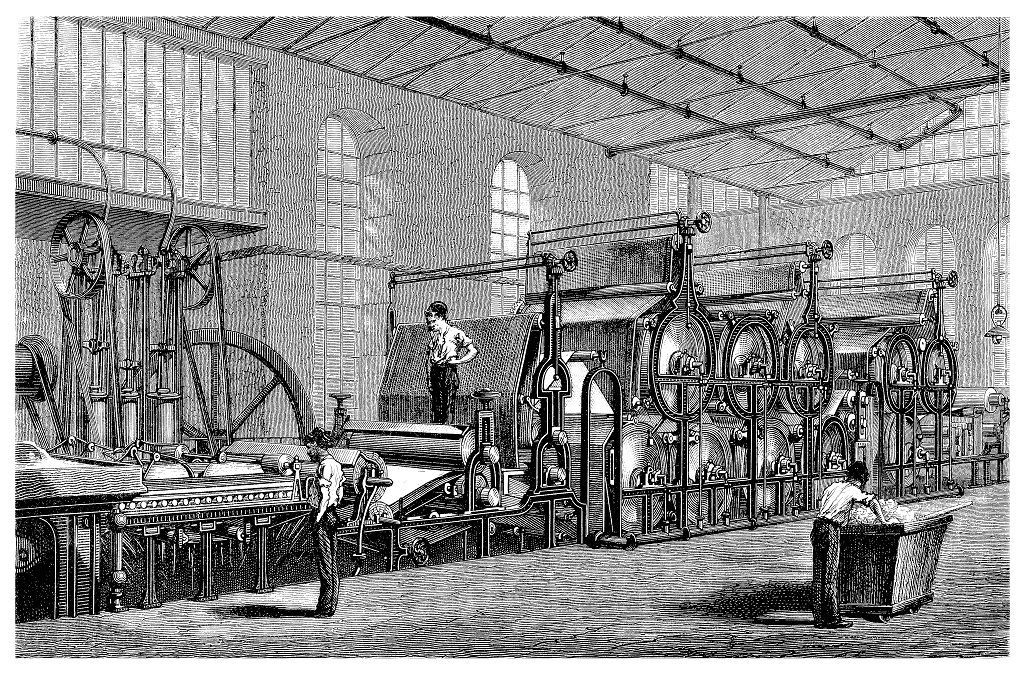

The change from hand production methods to machines to increase productivity

The Industrial Revolution started around 1760 and ended between 1820 and 1840. It originally began in Europe and slowly shifted over to the United States in the early 1800s. The latter half of the 18th century saw massive changes in the production of goods. Manufacturers were turning away from hand production methods towards machines to increase productivity.

The era saw new changes in chemical manufacturing, iron production, textile production, as well as across many other industries. The rapid development of steam power and water power was one of the core driving factors of the Industrial Revolution. It was a turning point in human history, changing how products were produced and the overall standard of living for a vast majority of the population.

The first industrial revolution in the 18th century should not be confused with a subsequent industrialization period, which occurred later in the 19th and 20th centuries and saw changes in metal (specifically, steel), electric, and automobile production.

The original industrial revolution began in England with the British textiles business and spread across other parts of Europe. Thousands of miles of canals and roads sprang up across Britain to assist the growth of the revolution. Also, steam-powered trains, both freight and passenger, became much more popular and helped transport goods across Europe.

The industrial revolution focused on economies of scale and turning to mass production of products. Economies of scale bring fixed and variable cost advantages to increases in production and technological advances.

The Industrial Revolution caused an everlasting impact on society and the living standards that we are familiar with today. It would be challenging to find many aspects of life that were not altered by the first industrialization period in the economy, production, and people.

Employment opportunities and wages increased across various sectors. Factories began to be a more appealing job, given the potential increase in income and benefits. It also increased the demand for housing in cities, subsequently improving the overall city layout, planning, and education systems. Due to increased education and the need for more advanced technologies, new inventions skyrocketed. Such a mindset ultimately continued to accelerate the revolution and all of its beneficiaries.

Gross domestic product (GDP) per capita began to grow with the Industrial Revolution, alongside the development of the modern capitalist economy. It was the beginning of consistent GDP growth for the next century. Countries that capitalized on industrialization started to rely less on imports and became more self-sufficient.

However, there were also some downsides to the Industrial Revolution. As a result of the extremely rapid changes in production, cities and governments saw new problems arise. Inner-city pollution saw an abrupt rise from factories and increased population as more workers moved to the cities. Living conditions in some places plummeted; sewage and waste flooded the streets and rivers.

Additionally, working conditions in factories decreased as companies tried to cut costs and become more profitable to stay ahead of their competitors. Child labor and employee health issues arose. The governments ended up implementing labor, pollution, and other regulations to ensure the safety of their people and the economy.

During the Industrial Revolution, banks saw greater importance in financing, specifically geared towards industrial financing. The growth demanded more capital from entrepreneurs and current business owners. Although technology costs were decreasing, the overall demand for infrastructure funding was on the rise.

Financing came from several sources; merchants, aristocrats, and wealthy families were all key contributors at the start. With the ever-increasing demand, general and specialist banks became more common and would provide long-term loans to these entrepreneurs in the revolution.

The Industrial Revolution, also known as the First Industrial Revolution, changed the way companies operated and resulted in an everlasting impact on the societies we see today. It stretched across the 1700s to 1800s.

Through economies of scale, businesses streamlined their processes and created more products at reduced costs. It increased employment opportunities and the wages associated with them. Workers flocked to cities to find work at the factories being set up, which, in the beginning, often paid more than farming.

Cities saw changes in their planning to adjust for the mass influx of people and to keep living conditions acceptable. Governments put in regulations to keep factory workers safe and reduce the exponential increase in pollution that the era saw.

The change also saw entrepreneurs and current businesses in more need of capital. Banks developed to be able to supply the necessary capital for these high-growth areas.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA®) certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: