Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Used by central banks to increase borrowing in times of economic recession

Negative interest rates are used by central banks to increase borrowing in times of economic recession. By offering a negative interest rate, the central bank decreases the overall economy-wide cost of borrowing, aiming to increase economic activity through increased investment and consumption spending.

Negative interest rates are a monetary policy tool and essentially imply that banks (lenders) will pay interest to borrowers for borrowing money and will collect interest on savings.

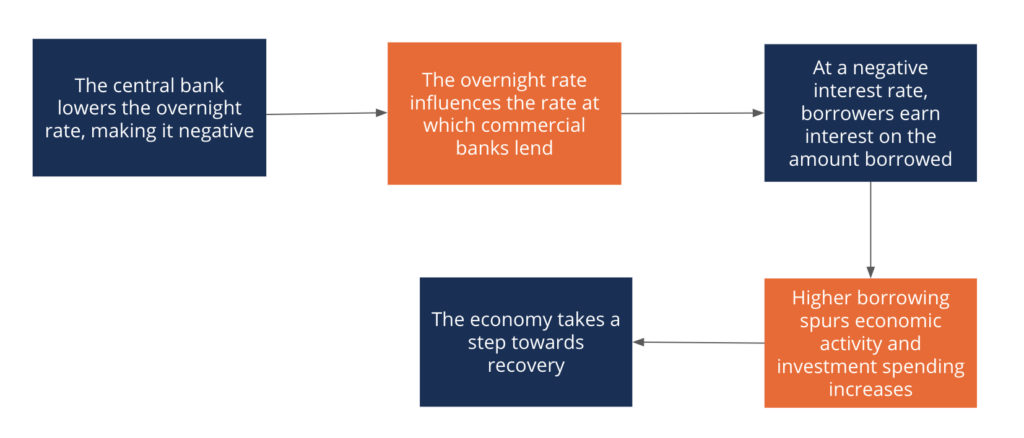

The following diagram shows the channels through which negative interest rates affect the economy (theoretically):

The overnight rate is the rate at which the central bank lends to commercial banks. At a negative overnight rate, commercial banks are encouraged to borrow more as they are paid interest on their borrowings.

The negative overnight rate incentivizes banks to lend more. Similarly, consumers and companies are attracted by the unusually low cost of borrowing – wherein they get paid to borrow money – resulting in higher investment and consumption spending.

Companies also borrow money to improve their cash balances at negative interest rates.

The lower interest rate also influences the exchange rate, devaluing the currency and increasing the demand for domestic goods in foreign markets, i.e., exports.

Increased borrowing and spending in the economy, in addition to higher exports, lead to an increase in aggregate demand, and the economy takes a step out of the recessionary phase.

Negative interest rates imply that instead of earning interest, deposits and savings will be charged by banks. However, in reality, savers may simply not earn any interest on their savings. The idea is to make saving unattractive and encourage consumers and companies to spend more instead of stockpiling cash.

Bonds that yield negative (or close-to-zero) interest rates are unattractive to investors. In times when the central bank chooses to reduce the overnight rate to zero or below, investors typically look for safer, income-earning securities like stocks.

Negative interest rates reduce the profit margins of lending institutions and commercial banks. Prolonged periods of low or negative interest rates may encourage banks to cease or decrease lending as profitability decreases.

Negative (or low) interest rates mean that foreign investors earn lower returns on their investments, which leads to lower demand for the domestic currency – devaluing the currency and reducing the exchange rate.

Currency devaluations may lead to competition among countries that export similar goods, along with unwanted exchange rate fluctuations.

To protect the domestic export industry from an increase in the exchange rate, the Japanese central bank reduced the interest rate in 2016 and announced a 0.1% charge on any reserves that commercial banks deposited in the central bank. This is an example of using negative interest rates as a monetary policy tool.

As of October 2019, several European countries including France, Switzerland, Spain, and Denmark also had negative interest rates as a result of the European Central Banks’ monetary policy to combat signs of economic recession and weakness.

With the COVID-19 pandemic, the US Federal Reserve has reduced overnight rates to almost 0.25%, sparking speculation that the interest rate may turn negative over the next few months. The interest rate has been reduced as a result of expansionary monetary policy.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: