Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Human-created tangible assets or inputs that are used to support the production of goods and services

Physical capital refers to the human-created tangible assets or inputs that are used to support the production of goods and services. It is one of the main factors of production in classical and neoclassical economics. Examples of physical capital include machinery, buildings, vehicles, equipment, etc.

In economics, capital represents the man-made assets that support economic activities. Physical capital, as a subset, refers to the durable non-financial assets used in the process of producing goods and services. It is also known as real capital, capital stock, or capital assets. Examples of physical capital include machinery, tools, buildings, inventory, and so on.

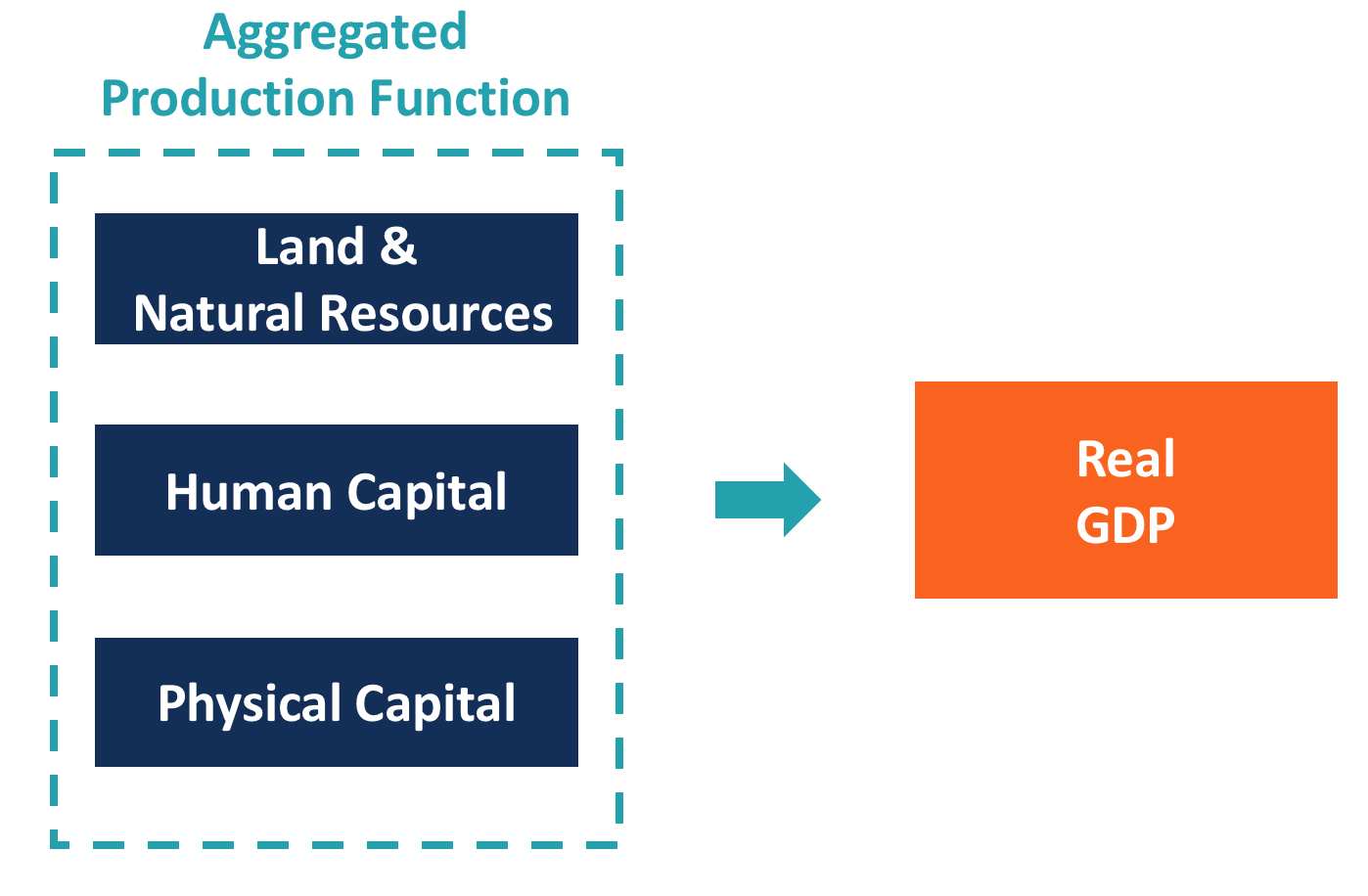

Physical capital is one of the factors of production in Adam Smith’s Classical Economics theory. Together with land and natural resources as well as human capital, the three factors will support the process of production and contribute to the real GDP growth of an economy.

The distribution of cost among land and natural resources, human capital, and physical capital can be used to price the product or service produced. These factors together can also be used to value a company.

As a tangible asset on the balance sheet, physical capital is an important component of a company’s valuation. However, it is quite difficult to properly assess the physical capital of a business because of the ambiguous boundary among the factors of production.

For example, some analysts consider the headquarters building of a company a part of its physical capital, but some might classify it as land. Economists remain divided on the exact classification criteria for each factor of production.

Many types of physical capital, such as machines and equipment, are fixed assets with years of economic life. Although the physical capital is not consumed out or destroyed during the production process, its value often diminishes over time due to depreciation. The book value (historical cost minus accumulated depreciation) is subject to depreciation assumptions, such as the remaining life, salvage value, and depreciation methods. A fixed asset’s book value can be very different from its fair market value.

The illiquid nature of physical capital provides another challenge in its valuation. Sometimes, machines and equipment are customized and can only be used for certain purposes. For example, a beverage company owns a particular bottle design. The bottling machine that it uses might be designed to fit the special shape of the bottles. It makes the resale of the machine more difficult and thus affects its fair market value.

Human capital refers to the labor hours and other resources or value-adds that humans can provide, including education, specialty skills, or even innovative ideas. Unlike physical capital, human capital is intangible.

While manufacturing companies typically own a large proportion of physical capital, technology companies rely more on intellectual or human capital. This also partially explains the high price-to-book ratios of many tech firms, as the value of human capital is not reflected on the balance sheet.

The value of human capital is difficult to measure because of its intangible nature. The extent to which a company’s value creation can be attributed to its human capital is ambiguous and can only be assumed. One of the methods to evaluate human capital is through market-ups in the goods or services a company produces. Premiums on salary and costs of employee benefit programs are another commonly used method.

Land and natural resources are also an essential part and often appear as raw materials in the production process. It includes naturally existing goods such as land, soil, minerals, and water resources. Both physical capital and land and natural resources are tangible assets of a company. The major difference is that physical capital is created by humans, while land and natural resources exist in nature.

Some goods might even show features of both factors, which can cause conflicts regarding the categorization. In the corporate building example discussed above, the building itself is man-made, but a large portion of the value of the building comes from the land, which naturally exists.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: