Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Money already spent and cannot be recovered

A sunk cost is a cost that has already occurred and cannot be recovered by any means. Sunk costs are independent of any event and should not be considered when making investment or project decisions. Only relevant costs (costs that relate to a specific decision and will change depending on that decision) should be considered when making such decisions.

All sunk costs are considered fixed costs. However, it is important to realize that not all fixed costs are considered sunk costs. Recall that sunk costs cannot be recovered. Take, for example, equipment (a fixed cost). Equipment can be resold or returned at a determined price. Therefore, it is not a sunk cost.

Sunk cost is also known as past cost, embedded cost, prior year cost, stranded cost, sunk capital, or retrospective cost.

The sunk cost fallacy reasoning states that further investments or commitments are justified because the resources already invested will be lost otherwise. Therefore, the sunk cost fallacy is a mistake in reasoning in which the sunk costs of an activity are considered when deciding whether to continue with the activity. This is also often known as “throwing good money after bad.”

Assume you spend $200 on a snowboarding trip at Grouse Mountain. Later on, you find a better snowboard trip at Cypress Mountain that costs $100 and you purchase that ticket as well. Unknowingly, you find out that the two dates clash and you are unable to get a refund on the tickets. Would you attend the $200 good snowboard trip or the $100 great snowboard trip?

A majority of people would choose the more expensive trip because, although it may not be more fun, the loss seems greater. The sunk cost fallacy prevents you from realizing what the best choice is and makes you place greater emphasis on the loss of unrecoverable money.

In the following examples, you can clearly see how sunk costs affect decision-making. Sunk costs cause people to think irrationally.

It’s a lot easier to avoid the sunk cost fallacy in financial modeling, as DCF models only look at future cash flows, and don’t give any consideration to the past.

For this reason, it can be helpful for a financial analyst to perform the exercise of building a financial model in Excel to remove any emotion (related to sunk costs) and look at whatever decision maximizes the Net Present Value going forward.

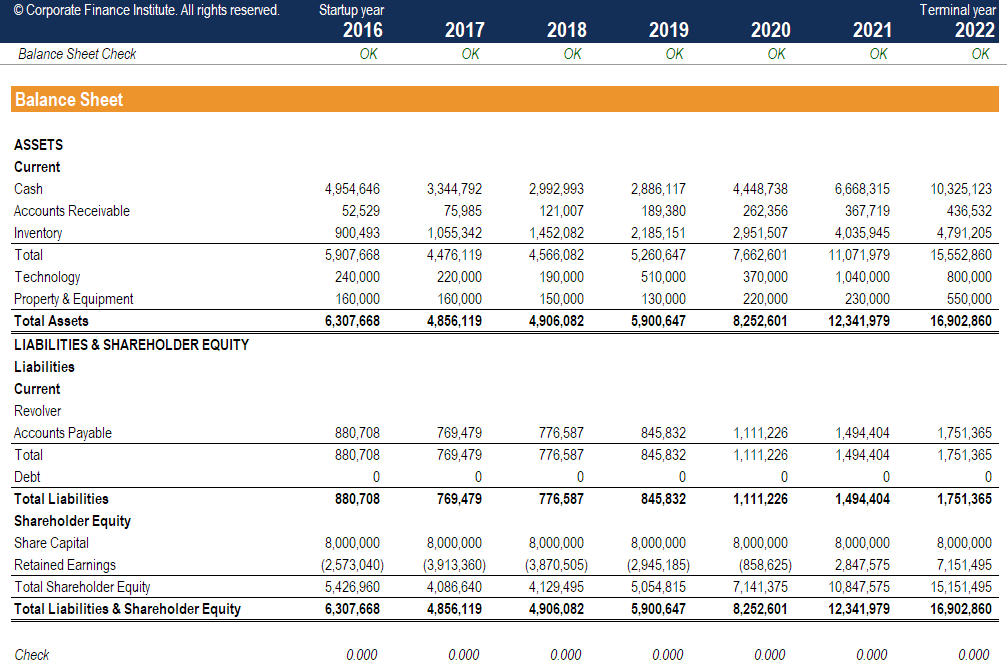

Source: CFI Financial Modeling courses

In both economics and business decision-making, sunk cost refers to costs that have already happened and cannot be recovered. Sunk costs are excluded from future decisions because the cost will be the same regardless of the outcome.

The sunk cost fallacy arises when decision-making takes into account sunk costs. By taking into consideration sunk costs when making a decision, irrational decision-making is exhibited.

Thank you for reading CFI’s guide to Sunk Cost. To keep learning and developing your knowledge base, please explore the additional relevant resources below: