Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Describing investors' relationship with risk

In the field of economics, utility (u) is a measure of how much benefit consumers derive from certain goods or services. From a finance standpoint, it refers to how much benefit investors obtain from portfolio performance.

While it may be intuitive to assume that all investors would like to achieve very high returns, it is important to realize that such returns typically require the investor to take on a lot of risks. Risk and return are trade-offs and follow a linear relationship. High-risk investments present a high likelihood of an investor losing all his/her money. Having a solid understanding of one’s u of money can help investors make investment decisions that are more suited to their risk attitudes and investment strategies.

Since the u scale varies widely across individuals and individuals have different u functions, it is quite difficult to quantify u. However, it is sometimes possible to use dollars as a quantitative measure of u. Consider the following example:

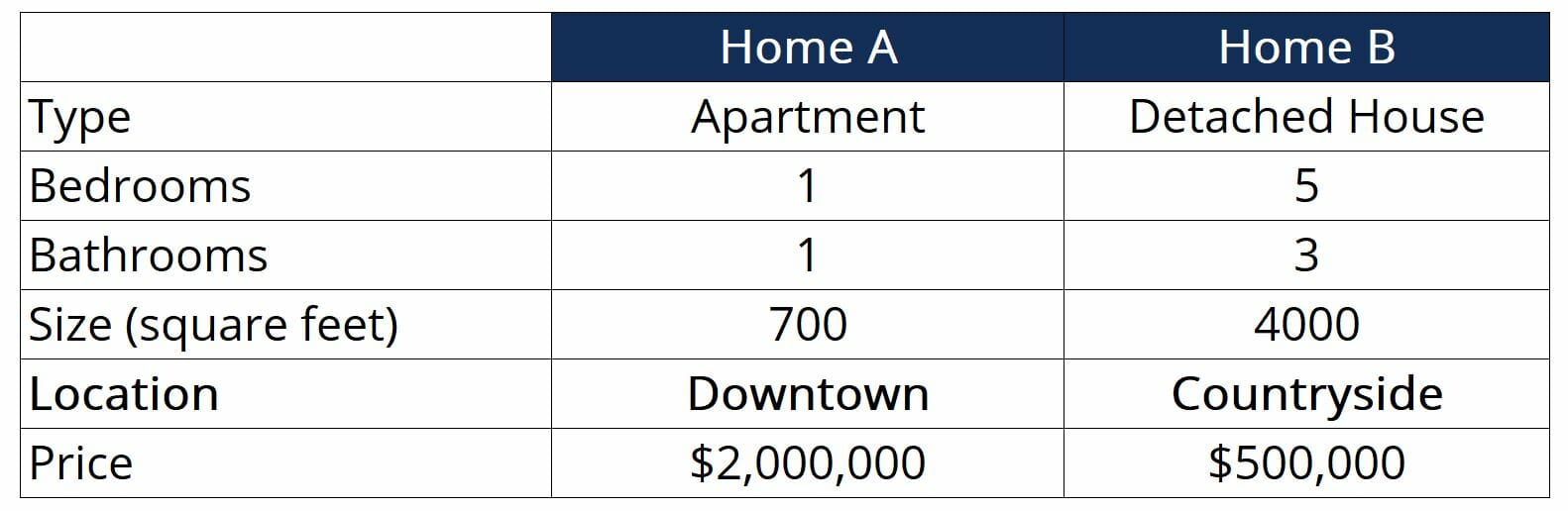

Ben is considering buying a new house. After conducting extensive research, Ben has narrowed down his options to the following:

From a value standpoint, Home B is a better deal since it provides more benefit as a standalone entity. However, Ben works downtown and thus decides to pay $2 million for Home A instead. In such a case, we can say that Ben’s utility of living downtown is $1.5 million (the premium over Home B).

There may be many people like Ben that would pay a large premium to live in a certain area. In such cases, studies can be conducted to further understand consumer behavior and draw additional insights.

Marginal utility refers to how much incremental u an individual derives from obtaining one additional unit of a certain good or service. Consumers derive decreasing marginal u from goods and services available in an economy. This means that after having a certain amount of a particular good or service, the u of acquiring one more unit of the good/service falls.

A recent study has found that people earning $95,000 per year derive just as much u from their salary as people earning $200,000 per year. This illustrates the concept of decreasing marginal u; after $95,000, individuals begin to value other things (such as time) much more than money.

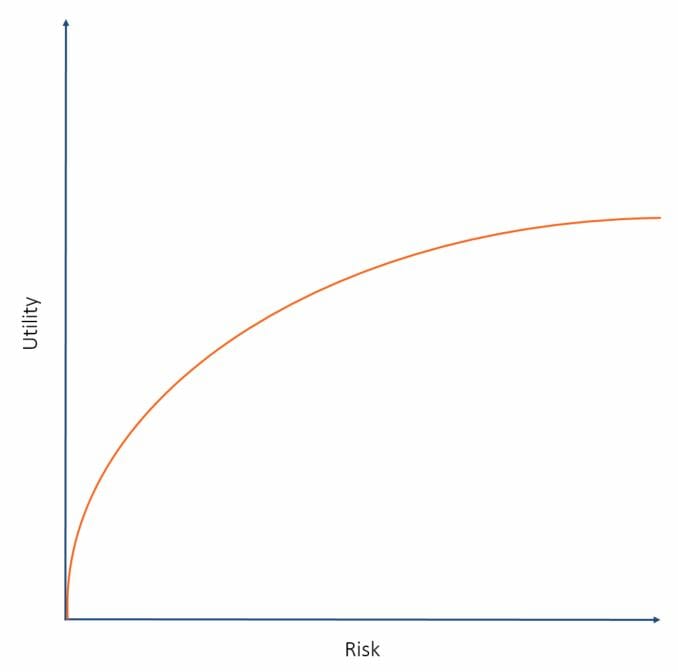

Generally speaking, there are three types of utility curves that explain the relationship investors have with risk.

This type of utility trend is what most individuals experience, according to the study cited above. From a conceptual standpoint, graphing this type of utility would give us the following:

As the investor takes on more risk (and thus the possibility of greater returns), they will start to have a smaller and smaller desire to take on further risk.

This attitude towards risk would be perfectly linear and not face changes in marginal utility. The graph below illustrates this relationship:

In practice, such an investor would continuously take on more risk since this will result in more utility. This type of investing behavior is quite rare.

This attitude towards risk would be exponential, meaning that this investor experiences increasing marginal utility. The graph below illustrates this relationship:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following CFI resources: