Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Dividends that are paid out from spare cash or excess earnings

A business with a residual dividend policy holds zero excess cash at any given point in time. All spare cash must be either reinvested in the business or redistributed among the shareholders.

Imperfections in the capital market make it rare for a company to follow a pure residual dividend policy. Most businesses instead follow smooth dividend policies that call for regular dividends that show some correlation with the business’ past and present earnings.

Shareholders receive a dividend, which is a portion of current profits, for investing in the company. They can receive dividends in many different ways, including receiving additional stock or cash payments. The board of directors of a company decides how much of a dividend the company will pay out and follows a certain dividend policy when distributing the company’s profits.

Many investors find dividends attractive because they provide a regular stream of income. Usually, dividends are paid out quarterly (in line with the company’s earnings reports), but in certain instances, a company may choose to pay out a special or irregular dividend.

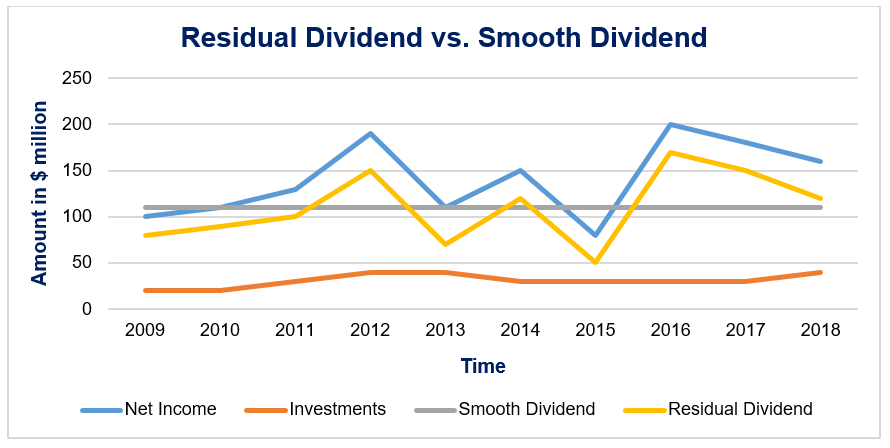

The graph below shows the dividends paid out by two companies over a 10-year period. The companies show identical earnings and investments but follow different dividend policies.

The company following a smooth dividend policy pays out $110 million as dividend payments each year of the 10-year period. The company following a residual dividend policy makes varying dividend payments over the same period of time. In 2015, it paid out only $50 million in dividend payments, whereas, in 2016 it paid out $170 million in dividends.

It should also be noted that, in 2009, the company following a smooth dividend policy spent $20 million on investments and $110 million on dividend payments despite only reporting a net income of $100 million. The additional $30 million in dividend payments must have been financed either through past earnings of the business or through short-term borrowing from a bank. This is consistent with empirical evidence that suggests that businesses tend to prefer a smooth dividend payout profile and use financial institutions to finance such dividends when necessary.

In theory, a residual dividend policy is more efficient than a smooth dividend policy. If at any point in time a business can find no further profitable investments, then they should return any spare cash available to the shareholders so that the shareholders may use the cash to invest in other projects that they believe will be profitable.

Thus, a residual dividend policy ensures that cash is efficiently distributed toward profitable investments. Under a smooth dividend policy, the management of a business may invest spare cash into unprofitable or unnecessarily risky projects only because funds are available.

Consider a business with a capital budget of $8,000,000. The business follows a 60-40 debt-equity split that they wish to maintain. The company makes a net income forecast of $5,000,000. Also, the business reports total equity of $3,200,000 (Total Equity = 40% of $8,000,000 = $3,200,000). The residual dividend paid is $1,800,000 ($5,000,000 – $3,200,000). The business shows a payout ratio of 36% ($1,800,000/$5,000,000). Consider the following alternative cases:

Net income drops to $3,000,000. Since the total equity of the business is $3,200,000, the entire amount is retained. Dividends paid and the dividend payout ratio are both 0.

Net income rises to $8,000,000. Since the total equity of the business is $3,200,000, $4,800,000 ($8,000,000 – $3,200,000 = $4,800,000) is paid out as dividends. The dividend payout ratio is 60% ($4,800,000/$8,000,000).

A residual dividend policy usually requires fewer new stock issues and lower flotation costs. However, a variable dividend policy may send conflicting signals to investors. It also represents an increased level of risk for investors, as dividend income remains uncertain.

Thank you for reading CFI’s guide to the Residual Dividend Policy. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: