Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Purchase price contingent on the future performance of the target

An earnout is a risk allocation mechanism for the acquirer wherein the purchase price is contingent on the “future performance” of the target company. The acquirer pays a majority of the purchase price upfront, at the time of closing the deal, and the remainder is contingent on the performance of the target.

For example, if the seller thinks the business is worth $100 million and the acquirer believes it is worth $70 million, they can agree on an initial price of $70 million and the remaining $30 million can form part of the earnout. The $30 million may be contingent on factors such as revenue, EBITDA margins, earnings per share, or retention of key employees.

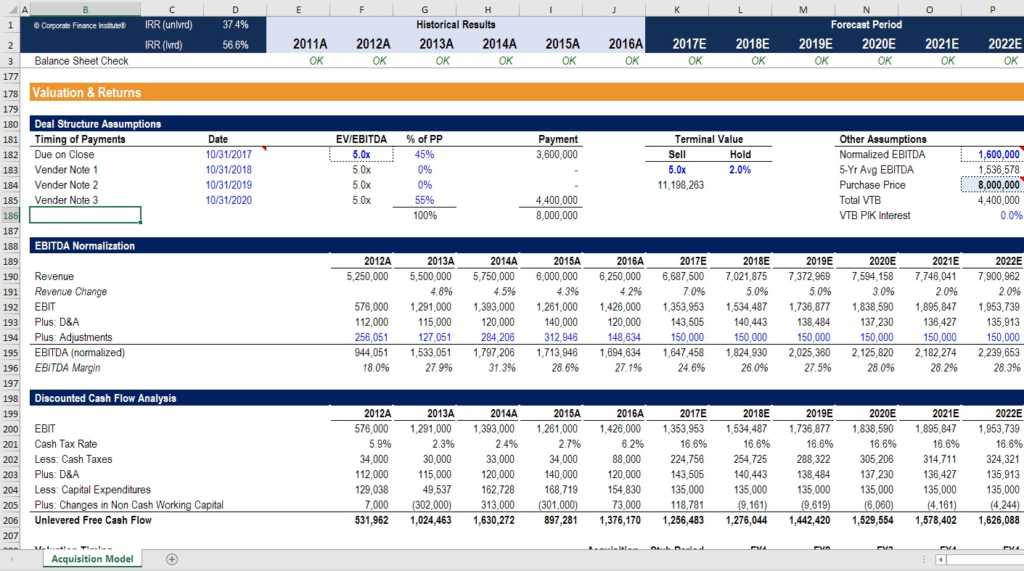

Source: Private Equity Acquisition Model from CFI’s Financial Modeling Templates Course

Disagreements about a company’s valuation in any deal are not something new. The seller wants to get the highest possible price, and he/she may believe that the business is worth more than the acquirer thinks. The acquirer, on the other hand, is wary about the target company’s growth or retention of key employees or major customers. One possible solution to this dilemma is earnouts, which help bridge the gap between an optimistic seller and a skeptical buyer.

Structuring the earnout is an important part of the M&A process.

Structuring an earnout is very important, as it involves how the business will run, who will have what kind of control over the business, and other key elements. A combination of all these decides what the company achieves in terms of revenue, EBITDA, contribution from top customers, etc., which in turn decides the payout for the seller. Below are a few considerations for structuring earnouts:

Technology and service companies with high growth potential are some of the companies that are mostly tied to earnouts in an M&A deal.

Generally speaking, the buyers prepare and present the financial statements and other factors on which earnouts depend. However, the sellers are afforded the complete opportunity to review the same and question the calculation of the earnouts. The definitive agreements will also include arbitration clauses to resolve any dispute in an effective and timely manner, such as the appointment of an independent accountant or auditor.

CFI is the official provider of the Financial Modeling & Valuation Analyst designation and on a mission to help you advance your career. To continue learning and developing your skills, these additional free CFI resources will be helpful: