Amortizable Bond Premium

The excess amount paid for a bond over its face value or par value

What is an Amortizable Bond Premium?

An amortizable bond premium refers to the excess amount paid for a bond over its face value or par value. Over time, the amount of premium is amortized until the bond reaches its maturity.

What are Bonds?

A bond is a type of fixed-income investment that represents a loan made from a lender (investor) to a borrower. It is an agreement to borrow money from the investor and pay the investor back at a later date.

An investor will agree to lend their money because a bond specifies compensation in the form of interest. The interest terms on a bond will vary, but essentially the lender will demand interest to compensate for the opportunity cost of providing the funding and the credit risk of the borrower.

Bond Pricing

Generally, a bond will come with a face value of $1,000 or some other round number. It is the amount that is promised to be repaid by the borrower. However, the actual price paid to purchase the bond usually is not $1,000. Based on market conditions, the price could be less than or greater than $1,000.

Bond prices are represented as a percentage of the face value. So, a bond trading at 100 would be priced at $1,000. A bond trading for less than 100 would be priced for less than $1,000; it is considered a discount. A bond trading for more than 100 would be priced for more than $1,000; it is considered a premium.

Bonds come with an associated coupon rate, which indicates the amount of cash paid in the form of interest payments to investors. The coupon rate is an important factor in pricing the bond.

Bond prices are inversely related to market interest rates. If market interest rates increase, bond prices fall. If market interest rates decrease, then bond prices increase. It is because stated coupon rates are fixed and do not fluctuate.

When market interest rates rise, for any given bond, the fixed coupon rate is lower relative to other bonds in the market. It makes the bond more unattractive, and it is why the bond is priced at a discount.

When market interest rates decrease, for any given bond, the fixed coupon rate is higher relative to other bonds in the market. It makes the bond more attractive, and it is why the bond is priced at a premium.

Bond Premiums

As mentioned earlier, if market interest rates fall, any given bond with a fixed coupon rate will appear more attractive, and it will result in the bond trading at a premium. So, if a bond comes with a face value of $1,000, and is trading at $1,080, it offers an $80 premium.

As the bond reaches maturity, the premium will be amortized over time, eventually reaching $0 on the exact date of maturity.

Amortizing the Bond

A method of amortizing a bond premium is with the constant yield method. The constant yield method amortizes the bond premium by multiplying the purchase price by the yield to maturity at issuance and then subtracting the coupon interest.

In order to calculate the premium amortization, you must determine the yield to maturity (YTM) of a bond. The yield to maturity is the discount rate that equates the present value of all coupons and principal payments to be made on the bond to its initial purchase price.

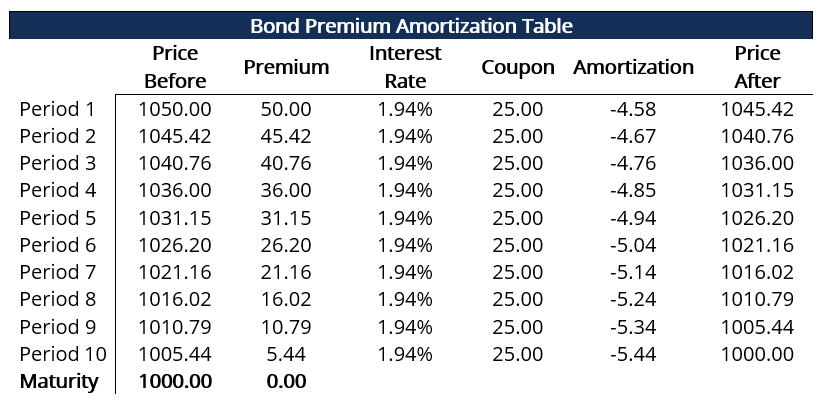

Example

For example, consider that an investor purchases a bond for $1,050. The bond comes with five years until maturity and a par value of $1,000. It offers a 5% coupon rate that is paid semi-annually and with a yield to maturity of 3.89%

Since the coupon rate is paid semi-annually, it means that every six months, a coupon of $25 ($1,000 x 5/2) will be paid. Also, the yield to maturity is stated in annual terms, so semi-annually the yield to maturity is 1.945% (3.89% / 2).

Plugging into the constant yield method formula, we get:

($1,050 x 1.945%) – $25 = –$4.58

The bond amortizes by $9.25 in the first period of six months. The bond’s value is now at $1,045.52 ($1,050 – $4.58).

If you continue it for the remaining nine periods, the bond will eventually be valued at $1,000 exactly. It is shown in the amortization table below:

More Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.