Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

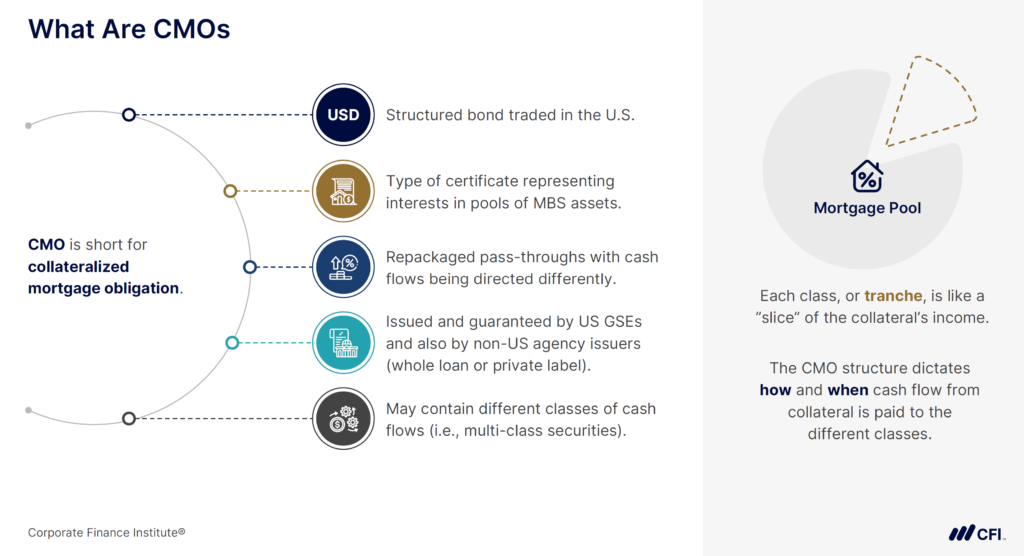

A Collateralized Mortgage Obligation (CMO) is a structured fixed income product that repackages mortgage-backed securities (MBS) into multiple tranches. Each tranche offers a different level of risk, return, and maturity, allowing investors to better manage cash flows and prepayment risk.

Since their creation in 1983, CMOs have become an enormous part of the fixed-income market, widely used by banks, insurance companies, pension funds, and hedge funds. To understand how CMOs function, it’s important to first examine their structure.

Structuring a Collateralized Mortgage Obligation (CMO) involves pooling different MBS together into tranches, or layers, of MBS with different risk and return profiles. CMOs redistribute cash flows to investors according to predefined rules that determine which investors get paid before others.

This CMO structure gives investors more control over:

A tranche is a layer of a CMO that determines when and how investors get paid. Each CMO consists of multiple tranches, each offering a different balance of risk, return, and timing:

By dividing risk among investors, CMOs offer greater predictability than traditional MBS.

CMOs are primarily issued by:

Agency CMOs dominate the market due to their government backing, while non-agency CMOs offer higher yields to compensate for risk.

To ensure tax efficiency and structured cash flow management, CMOs are typically issued through Special Purpose Vehicles (SPVs) or Real Estate Mortgage Investment Conduits (REMICs).

CMOs are widely held by institutional investors looking to manage risk and optimize returns. Examples include:

While CMOs provide customization and strong potential rewards, they also come with risks that investors need to consider.

Collateralized Mortgage Obligations (CMOs) offer structured payouts and tailored investment opportunities, but they also come with unique risks. Investors must weigh these risks against potential rewards before adding CMOs to their portfolios.

The table below breaks down the key risks and rewards associated with CMOs.

| Prepayment Behavior | Prepayment Risk: Homeowners refinancing or paying off mortgages early can return principal sooner than expected, forcing reinvestment at lower rates. | Predictable Cash Flows: Structured payouts help investors plan for steady income despite prepayment variations. |

| Maturity & Timing | Extension Risk: If prepayments slow down, some tranches take longer to mature, delaying expected cash flows. | Customizable Risk Profiles: Investors can choose tranches based on their risk tolerance and investment horizon. |

| Interest Rate Sensitivity | Interest Rate Risk: Rising rates reduce the market value of CMOs, making them less attractive for resale. | Higher Yields: Many CMO tranches offer better returns than comparable government bonds. |

| Creditworthiness | Credit Risk: Agency CMOs (Fannie Mae, Freddie Mac, Ginnie Mae) have low credit risk, but non-agency CMOs may carry default risk. | Government-Backed Options: Agency CMOs carry implicit or explicit government guarantees, lowering default risk. |

| Marketability | Liquidity & Complexity Risk: Some tranches may be difficult to value and harder to sell quickly in secondary markets. | Portfolio Diversification: CMOs provide exposure to mortgage-backed securities, helping investors spread risk across fixed-income assets. |

Understanding how risks like interest rate movements and mortgage prepayment trends affect CMOs helps investors make informed decisions that align with their goals.

While CMOs and traditional pass-through MBS are backed by pools of mortgage loans, their structure, cash flow management, and investor appeal set them apart.

The table below compares CMOs with pass-through MBS, the most common type of mortgage-backed security, to illustrate how these products function differently.

| Structure | Divided into tranches, each with different risk and return profiles. | Single class of securities where all investors receive equal payments. |

| Cash Flow Distribution | Follows a structured payment hierarchy, prioritizing some investors over others. | Mortgage payments are distributed pro-rata to all investors. |

| Prepayment Risk | Managed through tranches — some investors absorb prepayments while others receive predictable cash flows. | Directly affects all investors equally, making returns less predictable. |

| Investor Flexibility | Investors can choose tranches based on risk tolerance and income needs. | Limited customization — investors receive their share of payments with less control over cash flow timing. |

| Yield Potential | Some tranches offer higher yields for taking on prepayment or extension risk. | Typically, lower yields due to equal risk-sharing among all investors. |

| Complexity | More complex — requires investors to understand tranche structures and cash flow modeling. | Easier to understand, making it more accessible to a wider range of investors. |

Collateralized Mortgage Obligations (CMOs) offer the structured cash flows, risk segmentation, and investment flexibility that traditional mortgage-backed securities lack. The tranche structure of CMOs helps investors manage prepayment risk, interest rate exposure, and liquidity needs more effectively.

A solid understanding of CMOs enhances investment analysis, risk management, and investment decision-making. Whether you’re assessing fixed-income securities, trading structured products, or managing portfolio risk, CMOs are a key component of capital markets and corporate finance.

Ready to deepen your expertise in CMOs? Enrolling in CFI’s Collateralized Mortgage Obligations (CMOs) course equips you with the knowledge and confidence to navigate and analyze CMOs.

Enroll in Collateralized Mortgage Obligations (CMOs) today!

Mortgage-Backed Security (MBS)

Commercial Mortgage Backed Securities (CMBS)