Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Commercial mortgage-backed securities (CMBS) are a niche but impactful part of the fixed income securities market. If you’re eager to expand your fixed income or capital markets knowledge, understanding CMBS can set you apart. This guide delves into what CMBS are, how they work, their benefits and risks, and how they stack up against other fixed income securities.

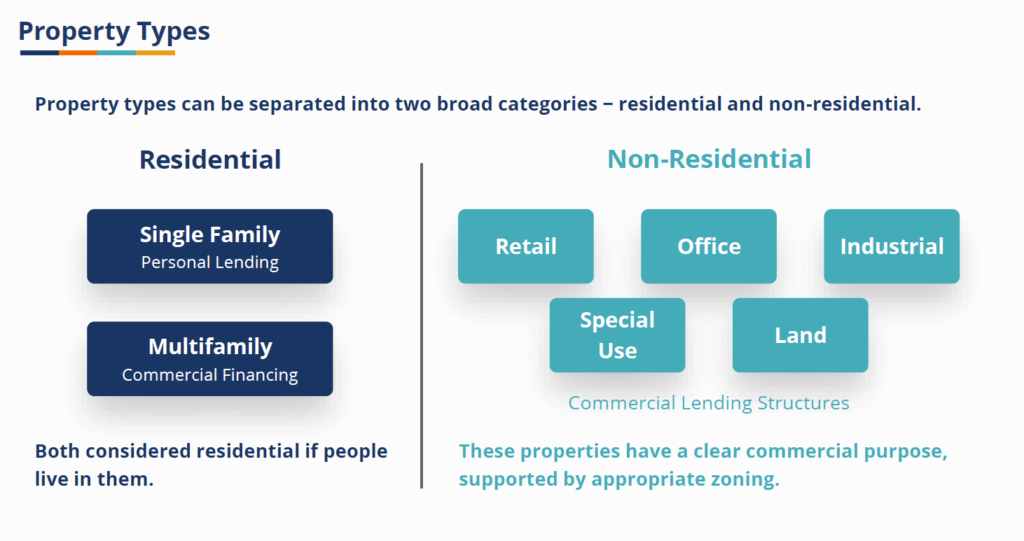

CMBS are a type of fixed income security backed by commercial real estate loans. These loans might include commercial mortgages on properties like office buildings, retail spaces, industrial facilities, or hotels.

Here’s how it works: lenders originate commercial real estate loans and package them into a trust. The trust then issues securities, known as CMBS, which institutional investors purchase. Each bond represents a share of the cash flow generated by the loan payments.

The structure of CMBS typically includes tranches, or layers, which determine the risk and return for investors. Senior tranches (the safest) get paid first, while subordinate tranches (riskier) absorb losses first but offer higher yields.

At the core of CMBS lies the transformation of mortgage loans on commercial properties into tradeable securities, offering investors access to the commercial real estate market without direct ownership. The mechanics of this process revolve around cash flow generation, allocation, and market dynamics.

The primary source of cash flow for CMBS comes from interest payments and principal repayments on the underlying mortgage loans. Borrowers — such as property owners of office buildings, hotels, or shopping malls — make these payments to the loan originators. These funds are then funneled into a trust, which distributes the cash flows to CMBS investors based on the tranching structure.

The predictability of fixed interest rates on loans can make cash flows more stable, appealing to conservative investors. However, variable-rate loans introduce additional uncertainty, as their payments fluctuate with market conditions.

The relationship between interest rates and CMBS is complex, influencing both primary and secondary markets. When interest rates rise, two major effects come into play:

These dynamics make it critical for CMBS investors to consider the broader interest rate environment when evaluating CMBS. For example, during periods of rising rates, the appeal of higher-yield subordinate tranches may increase as they offer a potential hedge against inflation.

The allocation of interest payments and the structure of fixed interest rates versus variable loans give CMBS their unique appeal. By understanding how changing economic conditions, such as fluctuating interest rates, affect the cash flow and market value of CMBS, investors can better align their portfolios with their risk tolerance and financial goals.

The underlying loans in a CMBS pool are diverse, reflecting the wide-ranging nature of commercial real estate. These pools often consist of commercial mortgage loans secured by commercial properties such as office buildings or shopping malls.

Common loan types include:

The diversity of commercial mortgages helps spread risk but can also introduce unique challenges depending on economic conditions.

Investing in CMBS offers several advantages:

Investing in CMBS comes with its own set of risks, making it important for investors to understand the potential challenges before diving into this market. Key risks include credit risk, market volatility, and the complexity of the securitization structure.

One of the primary risks in CMBS is credit risk, which reflects the likelihood of borrowers defaulting on their mortgage loans. This risk is managed through the use of credit ratings, which assess the quality and reliability of the various tranches within a CMBS structure.

For investors, these credit ratings provide a clear framework for assessing the relative risk and return of each tranche, enabling them to choose investments that align with their risk tolerance.

Beyond credit risk, CMBS investors face challenges such as:

Understanding the nuances of credit ratings and comparing CMBS to instruments like collateralized loan obligations can provide a clearer picture of where CMBS fit within a diversified investment portfolio. By carefully evaluating these risks, you can make more informed decisions and better manage potential downsides.

Ready to build in-demand risk management expertise? CFI’s Risk Management Specialization equips you with practical skills to identify, assess, and manage risks in financial institutions. Enroll today!

CMBS are a unique category within the broader universe of fixed-income securities, offering investors exposure to the commercial real estate market. However, they differ in key ways from other instruments like debt securities and residential mortgage-backed securities (RMBS).

While CMBS focuses on commercial properties, RMBS centers on residential real estate, such as single-family homes and multi-family units. The primary distinction lies in the underlying assets and their associated risk profiles:

For investors seeking stable income, RMBS may be a better fit than the higher-risk CMBS.

While CMBS focus on commercial properties, mortgage-backed securities (MBS) include loans backed by a broader range of real estate assets, including residential properties.

For investors seeking exposure to commercial real estate, CMBS offers a more specialized option than the broader, more stable focus of MBS.

Like CMBS, collateralized loan obligations (CLOs) pool loans into tranches with varying levels of risk and return. However, CLOs differ in their focus:

For investors looking to diversify into corporate debt, CLOs provide an alternative to CMBS.

Compared to debt securities such as government or corporate bonds, CMBS offers exposure to the commercial real estate sector.

For investors diversifying beyond traditional bonds, CMBS offers a unique opportunity.

By comparing CMBS with other types of fixed-income securities, you can better understand its place in a diversified portfolio. Whether you prioritize yield, stability, or sector-specific exposure, CMBS offers a compelling alternative for investors seeking diversification beyond traditional debt securities.

The CMBS market operates within a regulatory framework that ensures transparency and protects investors. In the U.S., the Securities and Exchange Commission (SEC) monitors the issuance and trading of CMBS, requiring full disclosure of credit ratings and cash flow projections. This oversight is essential for maintaining investor confidence, especially in a market where credit risk can be complex due to the layered nature of CMBS tranches.

Globally, regulatory bodies like the Securities and Futures Commission in Hong Kong enforce laws under frameworks such as the Securities and Futures Ordinance, requiring issuers to provide detailed information about loan pools, tranches, and associated risks.

The CMBS market has evolved significantly in response to economic shifts and interest rate fluctuations. As interest rates rise, the demand for fixed income securities like CMBS can fluctuate, impacting both yields and bond prices. At the same time, the market has benefited from innovations such as the securitization of diverse asset classes and improvements in credit ratings transparency.

Looking ahead, the future of CMBS will be shaped by how the market adapts to new challenges, including shifts in the commercial real estate sector. For instance, the growing prominence of CLOs may influence the structuring of CMBS, offering investors more nuanced ways to manage risk and return. Staying informed about these trends is vital for professionals exploring fixed-income opportunities.

Understanding CMBS is valuable knowledge for anyone entering the world of finance. Whether you’re building expertise as a student or looking to specialize as a professional, grasping how CMBS works opens doors to careers in real estate finance, investment management, or fixed-income trading. As you explore this fascinating market, consider how CMBS aligns with your goals and risk tolerance.

Looking for more insights into financial instruments? Explore CFI’s Capital Markets resources to deepen your expertise and gain the practical skills employers value.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Credit Risk Analyst Career Profile

Mortgage-Backed Securities (MBS)

Commercial Real Estate Lending