Duration Drift

A representation of the change in duration as a result of the passage of time

What is Duration Drift?

Duration drift represents the change in duration as a result of the passage of time. It is a problem in asset-liability management, which makes it necessary to regularly monitor and recalculate the duration of a financial instrument. To better understand duration drift and its effects, you need to first understand what duration is and how it is applied in asset-liability management.

Summary

- Duration drift is the change of duration due to the passage of time.

- Duration drift causes a problem for asset-liability management with a mismatched duration between the portfolio assets and liabilities.

- It is necessary to implement a dynamic portfolio immunization strategy by regularly monitoring and re-matching the durations.

What is Duration?

The value of a bond or other fixed-income instrument is sensitive to the change in interest rates. When the interest rate increases (decreases), the bond price falls (raises). The interest rate risk is measured by the duration of the bond.

Factors Affecting Duration

The following factors affect the duration of a bond:

1. Coupon Rate

Coupon rate is the rate at which bondholders receive a fixed income on their bonds. A bond costing $100 with a 5% coupon rate will pay the investor $5 every year. Between bonds with the same cost and maturity period, the one with a higher coupon rate will repay its actual cost in less time. Therefore, bonds with higher coupon rates come with lower durations, and consequently, lower risk.

2. Maturity Period

The longer it takes for a bond to mature, the higher will be its duration. Intuitively, between bonds with the same cost and yield, the one with a lower maturity period will repay its cost in lesser time. Naturally, bonds with less time to maturity pose less risk for investors.

Types of Duration

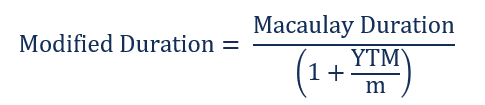

The two fundamental types are Macaulay duration and modified duration. The Macaulay duration of a bond measures the time it takes to pay back the investor the amount of the bond price with the present value of all the cash flows. The modified duration indicates the sensitivity of the bond price to the change in the interest rate. It can be calculated based on Macaulay duration.

Where:

- n = Total number of periods

- PV(CFt) = Present value of coupon at period t

- m = Number of coupons per year

Consider a bond with a modified duration of five years. For every 1% increase (decrease) in the interest rate, the bond price is expected to drop (raise) approximately by 5%. The larger the duration, the more sensitive the bond price is to the change in interest rate, and the larger the interest risk is.

The factors that affect the duration of a bond include the time to maturity and coupon rate. The bond with a longer time to maturity or lower coupon rate has a higher duration, and thus larger interest rate risk.

As shown in the diagram below, the zero-coupon bond has the highest duration, which is equal to the term of maturity. Also, the duration of the bond with a higher coupon rate (8% coupon) increases slower compared with the bond with a lower coupon bond (4% coupon).

Uses of Duration in Asset-Liability Management

Asset-liability management is the process used to solve the interest rate risk mismatch between the cash inflows received from the financial assets and outflows paid for the liabilities. There are two major approaches for asset-liability management: portfolio immunization and cash-flow matching.

Portfolio immunization implements a duration-matching strategy by matching the Macaulay duration of assets and liabilities. When the duration of the assets equals that of the liabilities in the portfolio, the timing of the cash inflows and outflows moves perfectly together as the market interest rate changes. Thus, the company can immunize from the exposure to interest rate risk.

Understanding Duration Drift

Duration drift represents the change of duration as a result of the passage of time. It causes a problem of matching the duration of the set of assets and liabilities for the asset-liability management purpose. A mismatch of duration leads to the exposure to interest rate risk.

If the duration of assets is greater (smaller) than that of liabilities, an increase (decrease) in the market interest rate leads to a larger decrease (smaller increase) in the value of assets than the value of liabilities, which causes a loss in the value of the portfolio.

Duration drift causes a mismatch of duration in several situations. The most common one is when the portfolio assets and liabilities come with different coupon rates. As mentioned above, the duration and term to maturity do not decrease at the same rate for coupon bonds.

The duration of the bond with a higher coupon rate moves slower as the change of term to maturity. For example, a company owns a portfolio of assets with a 4% coupon and a portfolio of liabilities with an 8% coupon. The durations of assets and liabilities are managed to match at the original point of time, but as time passes and term to maturity decreases, the duration of the assets declines slower than that of the liabilities. In such a situation, if the interest rate rises, the assets lose more value than the liabilities, and the value of the company falls.

Duration drift also happens to a portfolio consisting of a set of constant-maturity assets (liabilities) and a set of fixed-maturity liabilities (assets). The remaining life of fixed-maturity liabilities (assets) becomes shorter as time passes, and thus, its duration decreases. However, remaining term to maturity and duration of the assets (liabilities) with constant maturity is unchanged. It leads to a mismatch of duration and leaves the portfolio exposed to the interest rate risk.

For example, an auto finance portfolio comes with five years of average constant maturity. It is financed with a five-year fixed-maturity debt. Since the assets are replaced, the duration of assets remains unchanged, but the duration of the debt declines along with time. The duration drift of the fixed-maturity liability causes a duration gap.

The mismatch of duration caused by duration drift makes it necessary to constantly monitor and recalculate the duration of the portfolio assets and liabilities. Dynamic portfolio immunization strategies should be implemented to rebalance the drift in a timely manner.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: