Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Picture this: Your meticulously crafted budget, built on five years of historical data and precise financial models, falls apart just three months into the fiscal year. When this happens, it’s typically because financial plans rely solely on quantitative budgeting without considering the strategic insights from qualitative budgeting.

Financial planning and analysis (FP&A) professionals need to create reliable plans, but fast-changing assumptions and business drivers can make this an enormous challenge. Accurate, reliable budgeting requires a balance of hard numbers and adaptability for when conditions change.

Learning how quantitative vs. qualitative budgeting work together is key to making financial plans that can handle unexpected market changes and still help the company grow. This guide shows how to leverage both approaches to build resilient financial strategies aligned with broader business objectives.

Budgeting in FP&A serves multiple functions — allocating resources, setting financial performance expectations, and guiding decision making. Some budgets are built on historical data. Others prioritize market trends, business strategy, and leadership priorities.

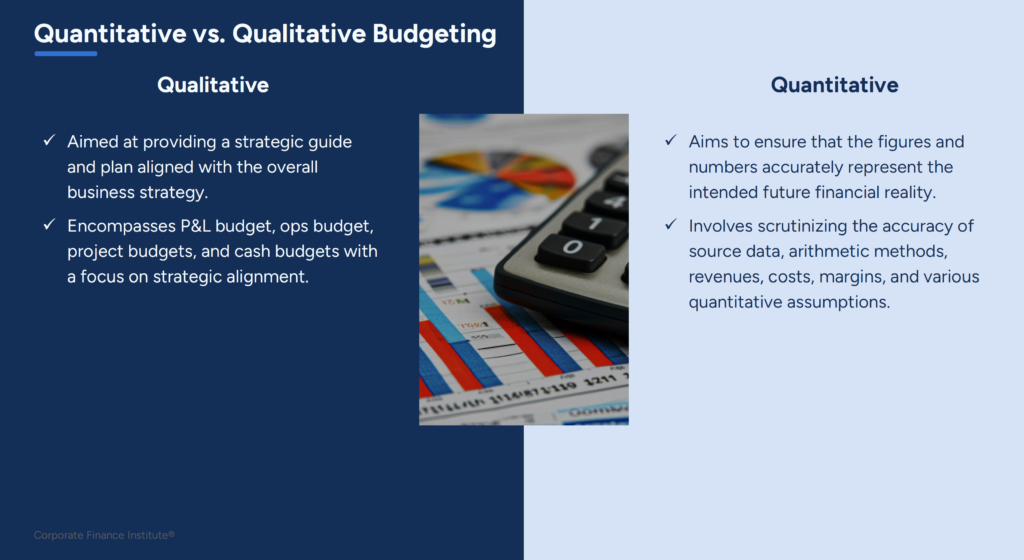

While different, both quantitative and qualitative budgeting provide unique benefits and limitations. The table below outlines how each method works, along with its applications, advantages, and potential challenges:

| Definition | Relies on numerical accuracy, historical data, and financial models to ensure predictability and control. | Prioritizes business strategy, market trends, and leadership priorities over historical financial data. |

| How It Works in FP&A | – Uses past financial trends to forecast revenue, expenses, and cash flow. – Applies formula-based modeling for precision. – Provides structured financial planning. | – Adapts to market trends, leadership insights, and company priorities. – Allows for adjustments. – Focuses on long-term strategic goals rather than historical patterns. |

| Example | A manufacturing company sets its budget by analyzing the past five years of operational costs, applying a 3% inflation rate, and maintaining strict expense controls. | A tech startup expands into a new market, allocating resources to product development and hiring despite a lack of supporting historical data. |

| Advantages | – Data-driven decision-making. – Structured and repeatable budgeting process. – Works well for cost efficiency and financial discipline. | – Supports strategic decision making beyond financial metrics. – Greater flexibility and adaptability. – Helps companies prioritize growth and innovation. |

| Limitations | – Over-reliance on historical data — past trends may not predict future performance. – Lack of flexibility — doesn’t account for sudden economic shifts. – Ignores qualitative insights — misses strategic decisions and market changes. | – Highly subjective — can be influenced by bias. – Difficult to measure accuracy — lacks precise financial tracking. – Potential for unrealistic expectations — may allocate resources without financial justification. |

| Limitation Example | A company using a strict quantitative budgeting model underestimates the impact of a new competitor entering the market, leading to overly optimistic sales projections. | A startup overestimates its ability to expand into a new market based on executive insights, failing to account for unexpected costs due to lack of quantitative analysis. |

Quantitative and qualitative budgeting play a role in corporate FP&A. The most effective FP&A professionals understand how to leverage both approaches to create budgets that are both financially sound and strategically aligned with business objectives.

Incorporating both quantitative data and qualitative insights enables you to create flexible budgets that can adapt to uncertainty while maintaining financial discipline.

Pro Tip: Challenge budget assumptions for better accuracy: To keep budgets realistic and aligned with business goals, ask clarifying questions like:

The best FP&A professionals view quantitative vs. qualitative budgeting as complementary tools, not competing methodologies. Relying solely on historical financial data can lead to missed opportunities while prioritizing strategic vision without financial discipline can compromise stability. The key is knowing when and how to apply each effectively.

Building skills in both quantitative and qualitative budgeting will help you advance in FP&A. You can develop this expertise through continuing professional education (CPE), practical skills training, and exposure to diverse budgeting scenarios.

Ready to level up your FP&A skills? CFI’s FP&A Specialization equips you with practical skills and deep expertise in financial modeling, budgeting, forecasting, and more — so you can drive better decision-making and advance your career.

Budgeting vs Forecasting in FP&A: Key Differences, Use Cases, and Tips

How to Analyze Budget Variances with 10 Essential Questions