Adjusted Gross Income (AGI)

An individual's total gross income less specific deductions

What is Adjusted Gross Income (AGI)?

Adjusted Gross Income (AGI) refers to an individual’s total gross income less specific deductions. AGI is the starting point to compute the tax due from an individual taxpayer in the United States. The Internal Revenue Code (IRC) defines two concepts – gross income and adjusted gross income in 26 U.S.C. §61 and §62, respectively.

According to 26 U.S.C §61, the gross income of an individual taxpayer is defined as income in the form of compensation, tips, revenues from business, royalties, annuities, interest, rents, interest from an estate, etc.

To the gross income, we make a few adjustments to arrive at the adjusted gross income, which is required for the purposes of calculating taxes payable. The adjustments fall into certain categories, as defined in 26 U.S.C. §61. Some of the major categories are discussed below.

Modified Adjusted Gross Income (MAGI) vs. Adjusted Gross Income

It is important to make a distinction between Modified AGI and AGI, which is a related concept and affects the final AGI number.

Modified Adjusted Gross Income (MAGI) is arrived at by adding back certain deductions made during the calculation of the adjusted gross income. The MAGI is used to check if the taxpayer is eligible for certain deductions. For example, if a taxpayer reports a MAGI above $80,000, then they are not eligible for deductions on interest paid on student loans.

Types of Deductions

1. Trade and business deductions

They are the deductions applicable to individual business owners for services performed as owners and not employees.

2. Trade and business deductions of employees

They are the deductions that can be claimed by employees for their services performed as part of a trade or business. The IRC defines many such deductions, such as:

- Reimbursed expenses of employees: They are the expenses incurred by the taxpayer in the performance of services as an employee. For example, an employee may claim deductions if they paid accommodation while on a business trip, and the benefit is paid by the employer and included in gross income.

- Certain expenses of performing artists: The expenses incurred by a performing artist in relation to the delivery of their performances. For example, a touring artist may claim deductions for their travel expenses.

- Certain expenses of officials: Government officials can claim deductions for expenses in the performance of their duties only if the officials are paid on a fee basis.

- Certain expenses of school teachers: School teachers are allowed to claim deductions on their income for expenses incurred in providing their services as educators. For example, a school teacher can claim deductions for stationery purchased for use in the classroom.

- Certain expenses of armed forces reserves: Members of the armed forces reserves of the United States can claim expenses incurred in the performance of their duties if such duties require them to travel more than 100 miles away from home.

3. Retirement savings

Taxpayers who contribute to Individual Retirement Accounts (IRAs) can claim deductions as mandated by 26 U.S.C. §219. Currently, the deductible amount is a maximum of $5,000 for those below the age of 50. The taxpayers who are 50 or older can claim another $1,000 for a total of up to $6,000.

4. Penalties for forfeiture of savings account

There are often penalties for withdrawing funds from a savings account earlier than the stipulated date. The penalties can be deducted from the gross income. It reduces the tax burden on those who may need to draw on their savings due to an emergency.

5. Health savings accounts

Individual taxpayers who contribute to a Health Savings Account (HSA) can claim deductions up to the limits as defined in 26 U.S.C §223. An HSA is a savings account where the amount from which will only be used for qualified medical expenditures.

6. Higher education expenses

A taxpayer can claim deductions for tuition paid for higher education or university. According to 26 U.S.C. §222, a taxpayer with a modified adjusted gross income of less than $65,000 can claim $4,000. A taxpayer with a modified adjusted gross income between $65,000 and $80,000 can claim $2,000. An individual with a modified adjusted gross income above $80,000 cannot make any deductions.

7. Interest on student loans

A deduction is allowed under 26 U.S.C. §221 for interest paid on student loans. The amount is equal to the interest paid during the year up to a maximum of $2,500.

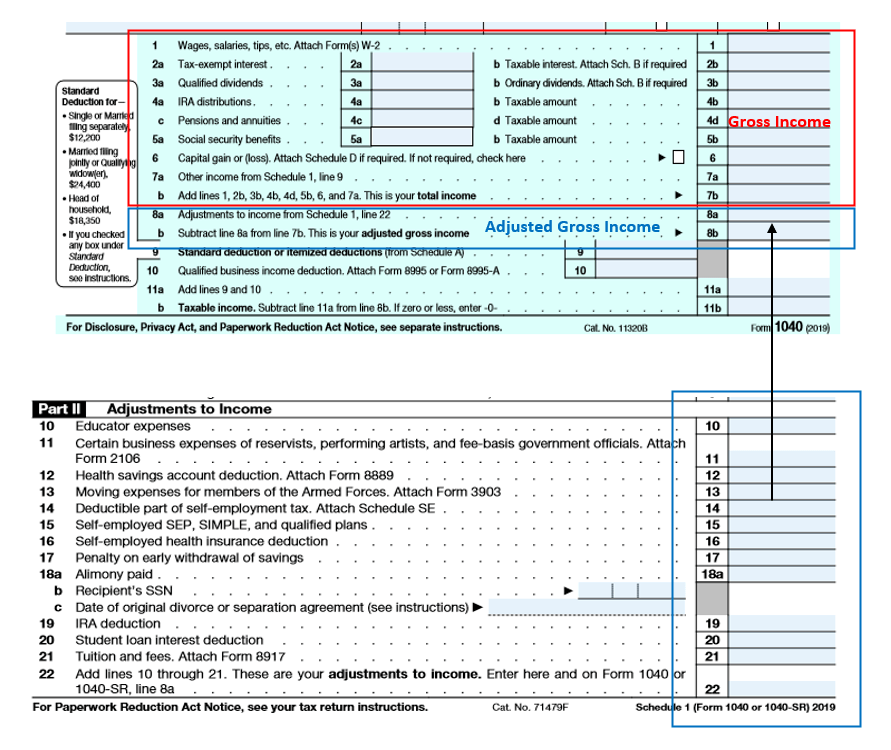

Form 1040

Form 1040 is the form that an individual taxpayer uses to file their taxes. The first item in the form is the gross income. After calculating the gross income, the deductions from Schedule I of the form are subtracted from the gross income to arrive at the adjusted gross income.

Schedule I is the part of Form 1040, where many of the deductions discussed above are claimed. The figure below reproduces the Form 1040 and the corresponding part of Schedule I.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.