Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A ratio that measures how efficiently a company uses its assets to generate sales

The asset turnover ratio, also known as the total asset turnover ratio, measures the efficiency with which a company uses its assets to produce sales. The asset turnover ratio formula is equal to net sales divided by the total or average assets of a company. A company with a high asset turnover ratio operates more efficiently as compared to competitors with a lower ratio.

The formula for the asset turnover ratio is as follows:

Where:

Company A reported beginning total assets of $199,500 and ending total assets of $199,203. Over the same period, the company generated sales of $325,300 with sales returns of $15,000.

The asset turnover ratio for Company A is calculated as follows:

Therefore, for every dollar in total assets, Company A generated $1.5565 in sales.

Enter your name and email in the form below and download the free template now!

Download the free Excel template now to advance your finance knowledge!

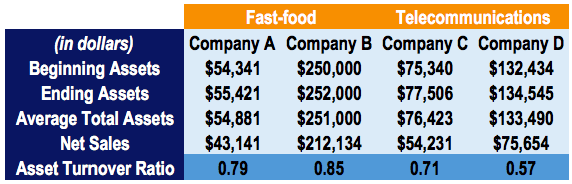

Consider four hypothetical companies: Company A, Company B, Company C, and Company D. Companies A and B operate in the fast-food industry, while companies C and D operate in the telecommunications industry:

The asset turnover ratio for each company is calculated as net sales divided by average total assets.

Ratio comparisons across markedly different industries do not provide a good insight into how well a company is doing. For example, it would be incorrect to compare the ratios of Company A to that of Company C, as they operate in different industries.

It is only appropriate to compare the asset turnover ratio of companies operating in the same industry. We can see that Company B operates more efficiently than Company A. This may indicate that Company A is experiencing poor sales or that its fixed assets are not being utilized to their full capacity.

The ratio measures the efficiency of how well a company uses assets to produce sales. A higher ratio is favorable, as it indicates a more efficient use of assets. Conversely, a lower ratio indicates the company is not using its assets as efficiently. Obsolete inventory or sluggish sales can lower the ratio. Same with receivables – collections may take too long, and credit accounts may pile up. Fixed assets such as property, plant, and equipment (PP&E) could be unproductive instead of being used to their full capacity.

All of these categories should be closely managed to improve the asset turnover ratio.

The asset turnover ratio can vary greatly depending on the industry. Industries with low profit margins tend to generate a higher ratio and capital-intensive industries tend to report a lower ratio.

Watch this short video to quickly understand the definition, formula, and application of this financial metric.

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: