Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The direct write-off and allowance methods of recording bad debt expense

First, let’s determine what the term bad debt means. Sometimes, at the end of the fiscal period, when a company goes to prepare its financial statements, it needs to determine what portion of its receivables is collectible. The portion that a company believes is uncollectible is what is called “bad debt expense.”

The two methods of recording bad debt are 1) the direct write-off method and 2) the allowance method.

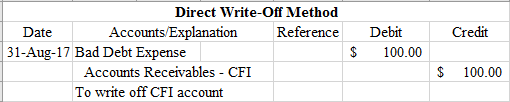

The method involves a direct write-off to the receivables account. Under the direct write-off method, bad debt expense serves as a direct loss from uncollectibles, which ultimately goes against revenues, lowering your net income.

For example, in one accounting period, a company can experience large increases in its receivables account. Then, in the next accounting period, a lot of their customers could default on their payments (not pay them), thus making the company experience a decline in its net income.

Therefore, the direct write-off method can only be appropriate for small immaterial amounts. We will demonstrate how to record the journal entries of bad debt using MS Excel.

When it comes to large material amounts, the allowance method is preferred compared to the direct write-off method. However, many companies still use the direct write-off for small amounts.

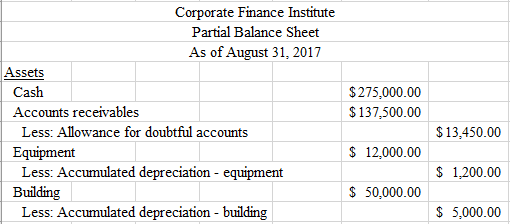

The reason for the preference is that the method involves a contra asset account that goes against accounts receivables. A contra asset account is basically an account with an opposite balance to accounts receivables and is recorded on the balance sheet as such:

This contra account is important because it has no effect on the income statement accounts. It means, under this method, bad debt expense does not necessarily serve as a direct loss that goes against revenues.

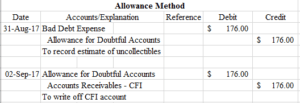

The three primary components of the allowance method are as follows:

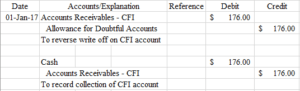

Sometimes, people or businesses pay back the amount but at a later date, which means that you need to reverse the write off you made and record the collection of the receivables. It would involve the following entry:

As mentioned earlier in our article, the amount of receivables that is uncollectible is usually estimated. Why? This is because it is hard, almost impossible, to estimate a specific value of bad debt expense.

Companies cannot control how or when people pay. Sometimes, people encounter hardships and are unable to meet their payment obligations, in which case they default.

The same thing happens to companies as well. Therefore, there is no guaranteed way to find a specific value of bad debt expense, which is why we estimate it within reasonable parameters.

The two methods used in estimating bad debt expense are 1) Percentage of sales and 2) Percentage of receivables.

Percentage of sales involves determining what percentage of net credit sales or total credit sales is uncollectible. It is usually determined by past experience and anticipated credit policy. Once management calculates the percentage, they multiply it by their net credit sales or total credit sales to determine bad debt expense. Here’s an example:

On March 31, 2017, Corporate Finance Institute reported net credit sales of $1,000,000. Using the percentage of sales method, they estimated that 1% of their credit sales would be uncollectible.

As you can see, $10,000 ($1,000,000 * 0.01) is determined to be the bad debt expense that management estimates to incur.

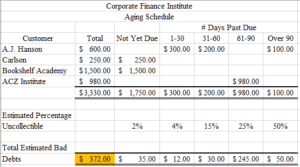

Under the percentage of receivables method of estimating bad debt expense, companies prepare an aging schedule, as shown below:

Again, the percentages are determined by past experience and past data. The most important part of the aging schedule is the number highlighted in yellow. It represents the amount that is required to be in the allowance of doubtful accounts. However, if there is already a credit balance existing in the allowance of doubtful accounts, then we only need to adjust it.

For example, let’s assume that there was a $100 credit already existing in the allowance account. In order to record the adjustment, we simply take the $372 and subtract the $100, giving us $272 and we record it as follows:

What if, instead of a credit balance in the allowance account, we posted a debit balance prior to the adjustment? Well, in this case, we would simply add. For example, let’s say there was a $175 debit existing in the allowance account. In order to record the adjustment, we simply take the $372 and add the $175 to get $547, and we record it as follows:

Every fiscal year or quarter, companies prepare financial statements. The financial statements are viewed by investors and potential investors, and they need to be reliable and possess integrity. Investors are putting their hard-earned money into the company, and if companies are not providing truthful financial statements, it means that they are cheating investors into placing money into their company based on false information.

Bad debt expense is something that must be recorded and accounted for every time a company prepares its financial statements. When a company decides to leave it out, they overstate their assets, and they could even overstate their net income.

Bad debt expense also helps companies identify which customers default on payments more often than others. If a company does decide to use a loyalty system or a credibility system, they can use the information from the bad debt accounts to identify which customers are creditworthy and offer them discounts for their timely payments.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

If you think you have mastered bad debt expense and how to record it, make sure to check out these related articles to get a deeper understanding of other accounting concepts:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: