Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Learn how and when to capitalize research and development costs

Under the United States Generally Accepted Accounting Principles (GAAP), companies are obligated to expense Research and Development (R&D) expenditures in the same fiscal year they are spent. It often creates significant volatility in profits (or losses) for many companies, as well as difficulty in measuring their rates of return on assets and investments.

A lack of R&D capitalization could mean that their total assets or total invested capital do not accurately reflect the amount invested in them. As a result, the company’s Return on Assets (ROA) and Return on Invested Capital (ROIC) may be affected. Below, we analyze the practice of capitalizing R&D expenses on the balance sheet versus expensing them on the income statement.

Let us compare GAAP with the International Financial Reporting Standards (IFRS). Under IFRS rules, research spending is treated as an expense each year, just as with GAAP. By contrast, though, development costs can be capitalized if the company can prove that the asset in development will become commercially viable (meaning the technology or product in development is likely to make it through the approval process and generate revenue).

The benefit of the IFRS approach is that at least some research and development costs can be capitalized (i.e., turned into an asset on the company’s balance sheet) instead of being incurred as an expense on the statement of Profit and Loss (P&L). The trade-off, however, is that IFRS requires judgment and subjectivity, which creates a risk that managers will be overly optimistic about how commercially viable a new technology is, which can cause inconsistencies in different companies’ financial statements.

R&D spending can vary widely from one year to another, which has a significant impact on a company’s profitability. Many businesses in the technology, healthcare, consumer discretionary, energy, and industrial sectors experience this problem.

If a company doesn’t capitalize research and development, its net income can be significantly higher or lower because of the timing of R&D spending. It’s important to note that net income doesn’t include the significant investments in R&D under its cash flow from investing activities. Additionally, this issue seems to contradict one of the main accounting principles, which is that expenses should be matched to the same period when the corresponding revenue is generated.

Research and development is a long-term investment for most companies resulting in many years of revenue, cash flow, and profit, and, thus, should theoretically be capitalized as an asset, not expensed. Without the capitalization of R&D spending, it is more challenging to compare companies in the same industry, as the timing of their research spending can have a big impact on their bottom line in a given year.

From an economic perspective, it seems reasonable that research and development costs should be capitalized, even though it’s unclear how much future benefit they will create. To capitalize and estimate the value of these assets, an analyst needs to estimate how many years a product or technology will generate benefit for (its economic life) and use that as an assumption for the amortization period.

The amortizable life will differ from asset to asset and reflects the economic life of the various products. For example, R&D products developed by a pharmaceutical company would likely last many years (and thus have a long amortization period), since it takes a long time for patents to be approved and there is also some patent protection they can enjoy monopolistic sales for several years. R&D amortization for a mobile phone company, however, should be amortized much faster (a smaller number of years) since new phones tend to emerge much more quickly and, thus, come with shorter shelf lives.

After estimating the economic life of an asset with a life of seven years, a company would then amortize the capitalized R&D expenses equally over the seven-year life. In the example below, we will assume the amortization of the asset uses the straight-line approach.

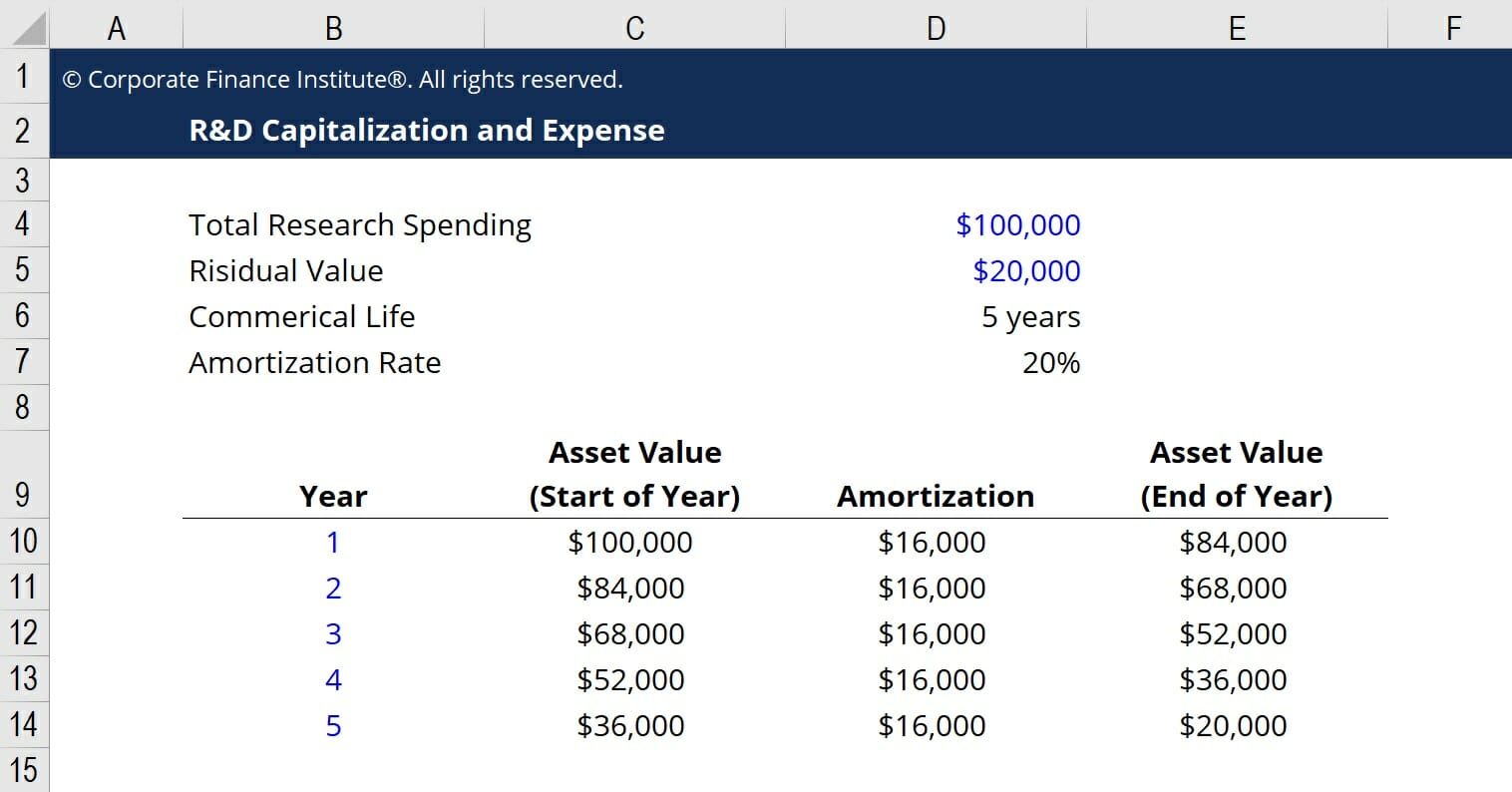

Below is an example of the R&D capitalization and amortization calculations in an Excel spreadsheet. The key assumptions are that a total of $100,000 has been spent on research and development, there is a $20,000 residual value, the product developed has a commercial life of 5 years, and the amortization expense uses the straight-line method.

Based on these assumptions, the company would have a $16,000 amortization expense each year, for five years, until it reaches the residual value of $20,000. By amortizing the cost over five years, the net income of the business is smoothed out and expenses are more closely matched to revenues.

Download CFI’s Excel template to advance your finance knowledge and perform better financial analysis.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to capitalizing R&D expenses. To advance your career, these additional CFI resources will help: