Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A guide to fixed vs variable costs

Cost is something that can be classified in several ways, depending on its nature. One of the most popular methods is classification according to fixed costs and variable costs. Fixed costs do not change with increases/decreases in units of production volume, while variable costs fluctuate with the volume of units of production.

Fixed and variable costs are key terms in managerial accounting, used in various forms of analysis of financial statements.

Total fixed costs are the sum total of the producer’s expenditures on the purchase of constant factors of production. The factors of production include capital, land, labor, and enterprise. Examples of fixed factors of production include rent on the factory, interest payments, salary of permanent staff, etc.

Total variable costs are costs that vary with production, and they are also called direct costs. Some examples of variable costs include fuel, raw materials, and some labor costs.

Sunk costs are the costs that cannot be recovered if a company goes out of business. Some examples of sunk costs include spending on advertising and marketing, specialist machines with no scrap value, and other investments whose value cannot otherwise be recovered.

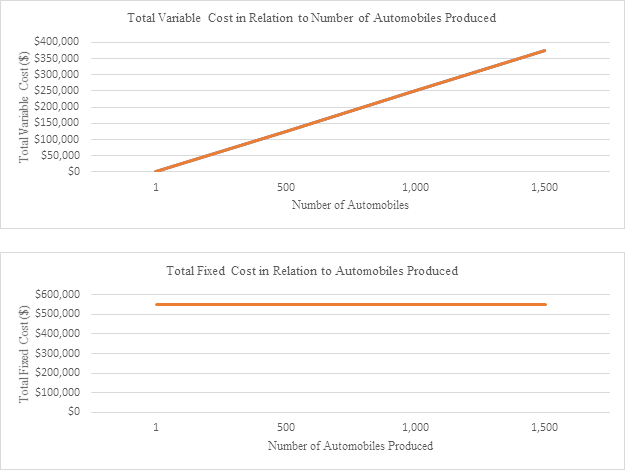

The first illustration below shows an example of variable costs, where costs increase directly with the number of units produced.

In the second illustration, costs are fixed and do not change with the number of units produced.

Graphically, we can see that fixed costs are not related to the volume of automobiles produced by the company. No matter how high or low sales are, fixed costs remain the same.

On the other hand, variable costs show a linear relationship between the volume produced and total variable costs.

Launch our financial analysis courses to learn more!

The table below summarizes the key differences between fixed and variable costs:

| Definition | Costs that vary/change depending on the company’s production volume | Costs that do not change in relation to production volume |

| When Production Increases | Total variable costs increase | Total fixed cost stays the same |

| When Production Decreases | Total variable costs decrease | Total fixed cost stays the same |

| Examples | - Direct materials (i.e., kilograms of wood, tons of cement) - Direct labor (i.e., labor hours) | - Rent - Advertising - Insurance - Depreciation |

The following table shows various costs incurred by a manufacturing company:

| Depreciation of executive jet | ||

| Cost of shipping finished goods to customers | ||

| Wood used in manufacturing furniture | ||

| Sales manager’s salary | ||

| Electricity used in manufacturing furniture | ||

| Packing supplies for shipping products | ||

| Sand used in manufacturing concrete | ||

| Supervisor’s salary | ||

| Advertising costs | ||

| Executive’s life insurance |

Let’s say that XYZ Company manufactures automobiles and it costs the company $250 to make one steering wheel. In order to run its business, the company incurs $550,000 in rental fees for its factory space.

Let’s take a closer look at the company’s costs depending on its level of production.

Launch our financial analysis courses to learn more!

Classifying costs as either variable or fixed is important for companies because by doing so, companies can assemble a financial statement called the Statement/Schedule of Cost of Goods Manufactured (COGM). This is a schedule that is used to calculate the cost of producing the company’s products for a set period of time.

The COGM is then transferred to the finished goods inventory account and used in calculating the Cost of Goods Sold (COGS) on the income statement.

By analyzing variable and fixed cost prices, companies can make better decisions on whether to invest in Property, Plant, and Equipment (PPE). For example, if a company incurs high direct labor costs in manufacturing their products, they may look to invest in machinery, which will reduce these high variable costs in exchange for more stable and known fixed costs.

This decision should be made with volume capacity and volatility in mind as trade-offs occur at different levels of production. High volumes with low volatility favor machine investment, while low volumes and high volatility favor the use of variable labor costs.

If sales were low, even though unit labor costs remain high, it would be wiser not to invest in machinery and incur high fixed costs because the high unit labor costs would still be lower than the machinery’s overall fixed cost.

The volume of sales at which the fixed costs or variable costs incurred would be equal to each other is called the indifference point. Finally, variable and fixed costs are also key ingredients to various costing methods employed by companies, including job order costing, process costing, and activity-based costing.

Launch our financial analysis courses to learn more!

While financial accounting is used to prepare financial statements that benefit external users, managerial accounting is used to provide useful information to people within an organization, mainly management, to help them make more informed business decisions.

A clear comparison can be seen in the following table:

| Purpose of Information | To communicate the company’s financial position to external users (i.e. investors, banks, regulators, government) | To help management make better decisions to fulfill the company’s overall strategic goals |

| Primary Users | External users | Internal (management) |

| Focus and Emphasis | Past oriented | Future oriented |

| Time Span | Annual or quarterly financial reports depending on company | Varies from hourly to years of information |

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Fixed and Variable Costs. To keep learning and advancing your career, the following resources will be helpful: