Modified Accrual Accounting

An accounting method that combines cash-basis accounting and accrual-basis accounting

What is Modified Accrual Accounting?

Modified accrual accounting refers to an accounting method that combines cash-basis accounting and accrual-basis accounting. It follows the cash-basis method to record short-term events and follows the accrual method to record long-term events.

The modified accrual method of accounting is created by the Government Accounting Standards Board (GASB). It does not comply with the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS).

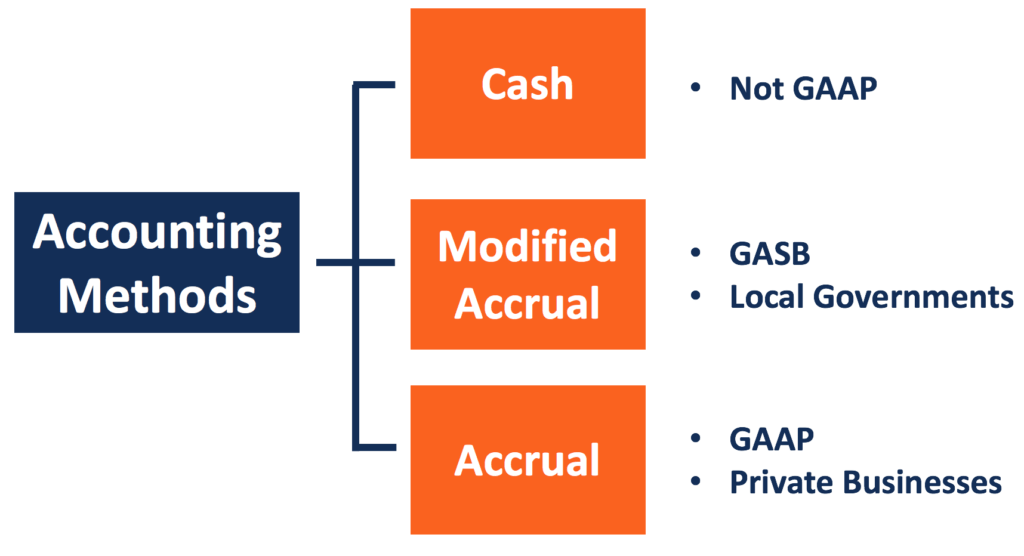

Summary

- Modified accrual accounting follows the cash-basis method to record short-term events. It follows the accrual method to record long-term events.

- The modified accrual accounting method recognizes revenues when they are available and measurable. It recognizes expenditures as they are incurred.

- The method does not comply with GAAP, so it is not used by public companies.

Basic Rules of Modified Accrual Accounting

The modified accrual accounting combines the features of the cash method and the accrual method. Under the cash method of accounting, revenues, and expenses are recorded when the cash is received or paid.

Under the accrual method, revenues are recorded when they are earned (goods or services are delivered), and expenses are recorded when they are incurred (products are consumed). Modified accrual accounting distinguishes short-term and long-term events and recognizes them in different ways.

Short-Term Events

Modified accrual accounting follows cash-basis accounting to report short-term events. The short-term items on the balance sheet include account receivables, inventory, and account payables. The economic events that affect the items are regarded as short-term events.

The events are recorded when the cash balance is changed. Therefore, almost all the income statement items are recorded in cash-basis accounting. The short-term assets and liabilities are no longer recorded on the balance sheet.

Long-Term Events

Fixed assets (PP&E) and long-term debts are some examples of long-term assets and liabilities. In contrast to short-term events, economic events that affect the items, or affect more than one accounting period, are known as long-term events.

Modified accrual accounting treats long-term events as accrual accounting does. Long-term assets and liabilities are recorded on the balance sheet. Depreciation, amortization, and debt repayments are reported over the life of the assets and debts.

However, there are some differences between modified accrual accounting and full accrual accounting in terms of recognizing the current portion of long-term debt. In full accrual accounting, the portion is recognized in the period and value when it is incurred. Modified accrual accounting recognizes the current portion of long-term debt as it matures. It can also be reported to the extent of liquidation with available financial resources that are expendable.

Revenues and Expenditures

Modified accrual accounting recognizes revenues when they are available and can be reasonably estimated. Revenues are available when they can finance the current expenditures paid within 60 days. Expenditures are reported in the same way as accrual accounting. They are recognized in the period when they are incurred, regardless of when the cash payments take place.

Some items take on different names in modified accrual accounting. For example, net income is named as excess or deficiency, and expenses are named as expenditures.

Modified Accrual Accounting and the GASB

Like the cash-basis accounting method, modified accrual accounting does not comply with the GAAP or IFRS. Thus, for-profit public companies do not use the cash-basis method; some may use it for internal reference.

Modified accrual accounting is set by the GASB with the purpose to measure the current-year revenues, expenditures, and financial resources in government funds.

The accounting purpose and requirements of government agencies are different from those of non-governmental entities. A company uses the accrual method to record its business activities and show its financial health to stakeholders more accurately.

A local government agency focuses on reflecting whether the current-year revenues are enough to cover the current-year expenditure. It tells whether the government is experiencing a surplus or deficit. A government agency should also be able to track whether it is using its financial resources according to the budget plan. The modified accrual method can meet such requirements.

By recording short-term events on a cash basis, the modified accrual method reflects the recent revenues and expenditures more clearly. The government agency can also categorize the fund into its internal entities. It helps the local government to better track whether it is spending the money as planned. It is also easier for the government to adjust its budget.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.