Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The calculation, management, recording, and analysis of employees’ compensation

Payroll accounting is essentially the calculation, management, recording, and analysis of employees’ compensation. In addition, payroll accounting also includes reconciling for benefits, withholding taxes, and deductions related to compensation. The calculation of payroll is highly influenced by each country’s legal requirements (it may also depend on state or local city requirements).

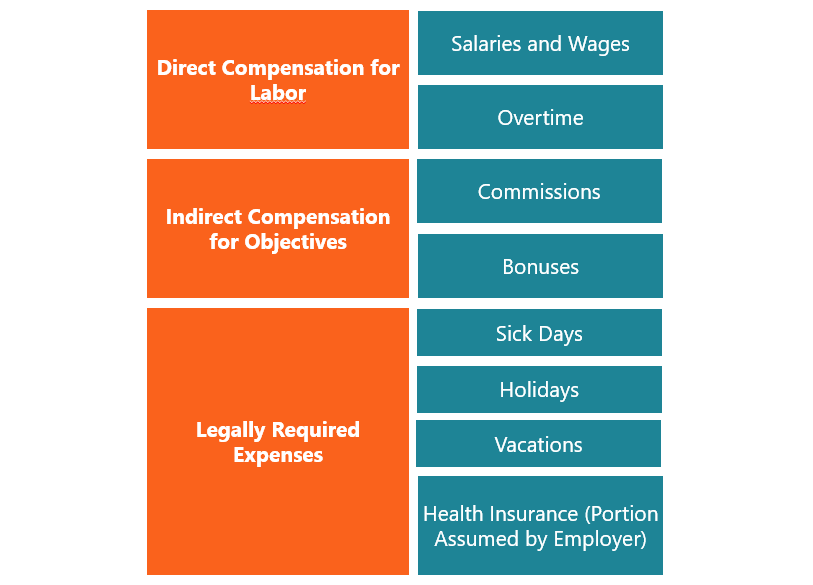

Payroll costs are related to obligations (expenses) assumed by an employer. They fund compensation paid to employees for their direct labor or as a consequence of mandatory benefits defined by legal requirements.

The sum of all the concepts listed above forms the accrued expense for keeping an employee on the payroll.

Under accounting principles, all accrued expenses must meet the matching principle. The matching principle states that all expenses need to match in the period when all the related revenues are reported (it does not depend on the payment date). For example, if an employee is hired on the first day of December but paid on the first week of January, the expense related to the labor of the employee must be recognized in December.

Note: Compensation for employees’ labor is not always recognized as an expense. For example, if the labor of employees is used for manufacturing a product or asset, the compensation (including provisions) should be registered as the cost of manufacturing the product (inventory) or asset and recognized as an expense when the inventory is sold (through cost of sales).

Performance obligations are related to withholdings or deductions from employees’ wages. These retained amounts are not paid directly to employees, but they are paid later to government institutions or private companies. The most common withholdings according to US laws are:

Other withholdings include:

Before starting the hiring process, employers must meet certain requirements or considerations. They comply with US federal legislation and may vary from state to state.

The Federal Employment Identification Number is used to track federal tax payments. A company must get an EIN from the IRS.

After deciding the salary level (based on position, experience, industry, etc.) and the type (hourly or annual wage), select the period during which employees will be paid. Payments are usually scheduled weekly, biweekly, or monthly. Payment periods should not be longer than a monthly basis.

If employers offer extra benefits such as insurance or a 401(k) retirement plan, they will have to decide how much to contribute as the employer and how much the employee must assume to get the benefit.

When hiring employees, it is important to gather all the information related to the right to work in the US and personal information. The most important forms are the I-9 Form (to verify if the employee has the citizenship or the right to work in the US under a work permit), the W-4 form (Employees’ Personal information – by completing this form, you obtain the information needed to calculate the withholding applicable to an employee), and the Direct Deposit Form.

After setting up the company to hire employees and gathering all the information related to the employees, the company will need to follow these steps:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Payroll Accounting. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: