Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An accounting process that is used to prove that the transactions adding up to the ending balance are correct

Reconciling an account is an accounting process that is used to ensure that the transactions in a company’s financial records are consistent with independent third party reports. Reconciliation confirms that the recorded sum leaving an account corresponds to the amount that’s been spent and that the two accounts are balanced at the end of the reporting period.

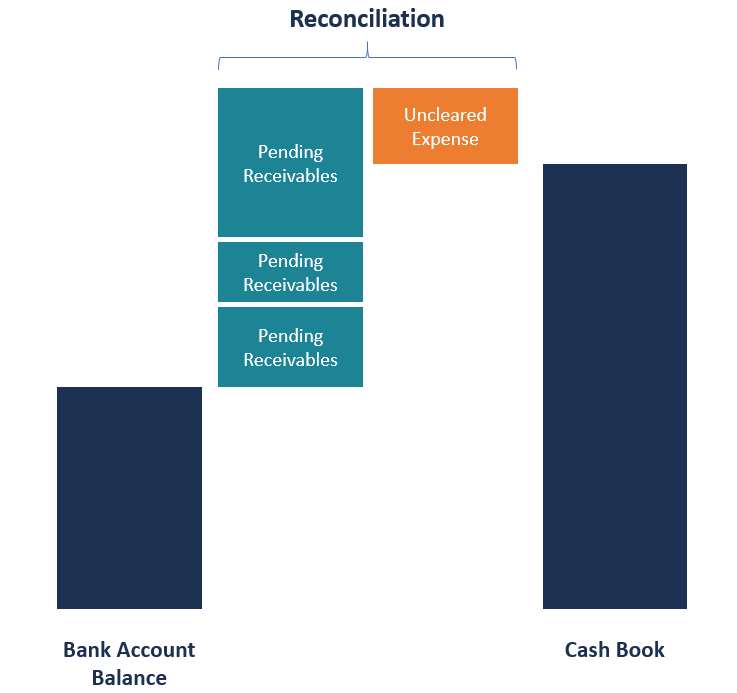

Reconciliation is used by accountants to explain the difference between two financial records, such as the bank statement and cash book. Any unexplained differences between the two records may be signs of financial misappropriation or theft.

Account reconciliation is necessary for asset, liability, and equity accounts since their balances are carried forward every year. During reconciliation, you should compare the transactions recorded in an internal record-keeping account against an external monthly statement from sources such as banks and credit card companies. The balances between the two records must agree with each other, and any discrepancies should be explained in the account reconciliation statement.

The following are the two main ways of reconciling an account:

Documentation review is the most commonly used account reconciliation method. It involves calling up the account detail in the statements and reviewing the appropriateness of each transaction. The documentation method determines if the amount captured in the account matches the actual amount spent by the company.

For example, a company maintains a record of all the receipts for purchases made to make sure that the money incurred is going to the right avenues. When conducting a reconciliation at the end of the month, the accountant noticed that the company was charged ten times for a transaction that was not in the cash book. The accountant contacted the bank to get information on the mysterious transaction.

The bank discovered that the mysterious transaction was a bank error, and therefore, reimbursed the company for the incorrect deductions. Rectifying the bank errors bring the bank statement balance and the cash book balance into an agreement.

The analytics review method reconciles the accounts using estimates of historical account activity level. It involves estimating the actual amount that should be in the account based on the previous account activity levels or other metrics. The process is used to find out if the discrepancy is due to a balance sheet error or theft.

For example, a company can estimate the amount of expected bad debts in the receivable account to see if it is close to the balance in the allowance for doubtful accounts. The expected bad debts are estimated based on the historical activity levels of the bad debts allowance.

Most companies use accounting software to record transactions and reconcile any differences that arise between the bank statement and the cash book. However, reconciliation may require human intervention to record transactions that might have been entered incorrectly, were omitted, or were a result of bank errors. Here is the step-by-step process of conducting an account reconciliation:

Tick all transactions recorded in the cash book against similar transactions appearing in the bank statement. Make a list of all transactions in the bank statement that are not supported, i.e., are not supported by any evidence, such as a payment receipt.

The transactions may include ATM transactions and checks. The transactions should be deducted from the bank statement balance. Also, transactions appearing in the bank statement but missing in the cash book should be noted. Some of the transactions affected may include ATM service charges, check printing fees. overdrafts, uncleared checks, etc.

Find direct deposits and account credits that appear in the cash book but not in the bank statement, and add them to the bank statement balance. Similarly, if there are deposits appearing in the bank statement but are not in the cash book, add the entries to the cash book balance.

A bank error is an incorrect debit or credit on the bank statement of a check or deposit recorded in the wrong account. Bank errors are infrequent, but the company should contact the bank immediately to report the errors. The correction will appear in the future bank statement, but an adjustment is required in the current period’s bank reconciliation to reconcile the discrepancy.

After finding evidence for all differences between the bank statement and the cash book, the balances in both records should be equal. You should prepare a bank reconciliation statement that explains the difference between the company’s internal records and the bank account.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: