Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The starting point of the income statement

Sales revenue is the income received by a company from its sales of goods or the provision of services. In accounting, the terms “sales” and “revenue” can be, and often are, used interchangeably to mean the same thing. It is important to note that revenue does not necessarily mean cash received. A portion of sales revenue may be paid in cash and a portion may be paid on credit, through such means as accounts receivables.

Sales revenue can be shown on the income statement by either the gross revenue amount or net revenue. Gross revenue is before contra-revenue accounts like allowance for sales returns, bad debt expense, any potential sales discounts, etc. Gross revenue is reduced to net revenue after accounting for all of the previously discussed contra-revenue accounts.

Most companies simply report net revenue. However, if gross revenue is shown it will have the contra-revenue deductions listed below gross revenue, and a subtotal for net revenue below that.

The very first line of the income statement is sales revenue. This is important for two reasons. First, it marks the starting point for arriving at net income. From revenue, cost of goods sold is deducted to find gross profit. Depreciation and SG&A expenses are deducted from gross profit to find the operating margin, also known as EBIT. EBIT less interest expense is pre-tax income, and pre-tax income minus taxes is net income.

Secondly, as the first item on the income statement, sales revenue is an important line item in the top-down approach of forecasting the income statement (and also why revenue is often known as the “top line”). The historic trend of revenue is analyzed, and revenue for future periods is forecasted. All expenses below sales revenue are often found expressed as a percentage of that revenue. As the first item listed on a financial statement, it becomes the pivot or anchor from which other line items are proportional to.

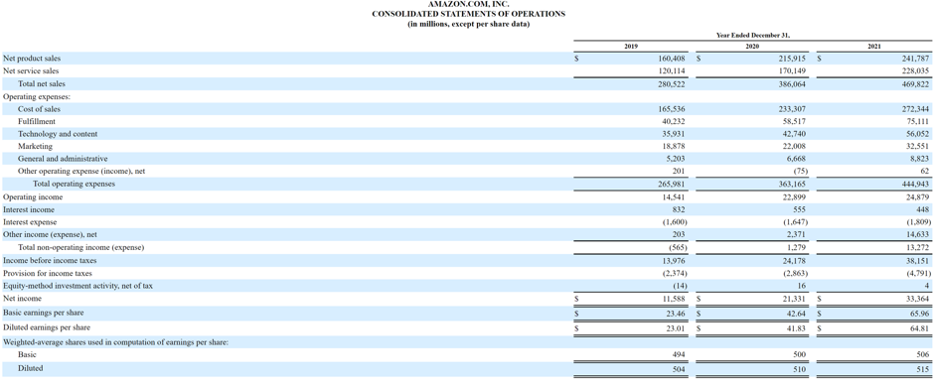

Below is an example from Amazon’s 2017 annual report (10-k) which shows a breakdown of its sales according to products and services. In 2017, Amazon had net sales of $119 billion from products and $59 billion from services, for a combined total of $178 billion. As you can see, this forms the top of the income statement, and all expenses and profits or losses are located below that level in the report.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.