Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

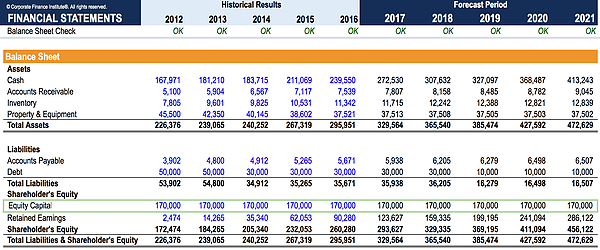

The cash invested by shareholders and investors

Share capital (shareholders’ capital, equity capital, contributed capital, or paid-in capital) is the amount invested by a company’s shareholders for use in the business. When a company is first created, if its only asset is the cash invested by the shareholders, the balance sheet is balanced with cash on the left and share capital on the right side.

Share capital is a major line item but is sometimes broken out by firms into the different types of equity issued. There can be common stock and preferred stock, which are reported at their par value or face value. Note that some states allow common shares to be issued without a par value.

Share capital is separate from other types of equity accounts. As the name “additional paid-in capital” indicates, this equity account refers only to the amount “paid-in” by investors and shareholders, and is the difference between the par value of a stock and the price that investors actually paid for it.

Through the fundamental equation where assets equal liabilities plus equity, we can see that assets must be funded through one of the two. One method for a company to fund its assets is to create liabilities (borrow money or issue debt) and, therefore, create obligations that must be paid back. The other option is to issue equity through common shares or preferred shares. In exchange for an ownership interest claim to the company, the company receives cash from investors and shareholders.

Share capital may also include an account called contributed surplus or additional paid-in capital.

Contributed Surplus is an accounting item that’s created when a company issues shares above their par value or issues shares with no par value. If a company raised $1 million from shares that had a par value of $100,000 it would have a contributed surplus of $900,000. The par value of shares is essentially an arbitrary number, as shares cannot be redeemed for their par value.

Additional Paid-in Capital is the same as described above.

In summary, if a company issued $10 million of common shares with $100,000 par value, it’s equity capital would break down as follows:

Thank you for reading CFI’s guide to Share Capital. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: