Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A guide to understanding T Accounts

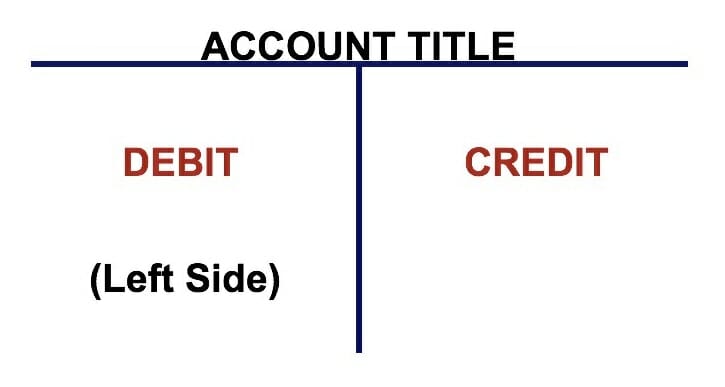

If you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts in the form of a “T,” making it so that all additions and subtractions (debits and credits) to the account can be easily tracked and represented visually.

Each account will have its own individual T Account, which looks like the following:

Image: CFI’s Accounting Courses.

Download CFI’s Excel template to advance your finance knowledge and perform better financial analysis.

When most people hear the term debits and credits, they think of debit cards and credit cards. In accounting, however, debits and credits refer to completely different things.

Debits and Credits are simply accounting terminologies that can be traced back hundreds of years, which are still used in today’s double-entry accounting system. A double-entry accounting system means that every transaction that a company makes is recorded in at least two accounts, where one account gets a “debit” entry while another account gets a “credit” entry.

These entries are recorded as journal entries in the company’s books.

Debits and credits can mean either increasing or decreasing for different accounts, but their T Account representations look the same in terms of left and right positioning in relation to the “T”.

The left side of the Account is always the debit side and the right side is always the credit side, no matter what the account is.

For different accounts, debits and credits can mean either an increase or a decrease, but in a T Account, the debit is always on the left side and credit on the right side, by convention.

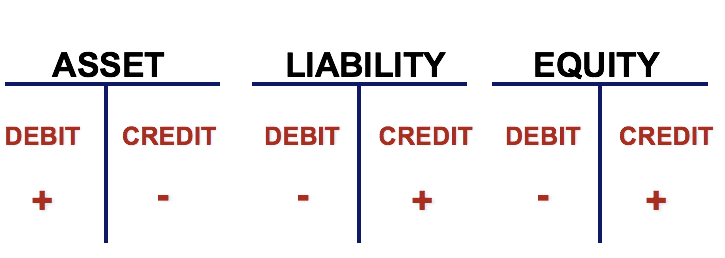

Let’s take a more in-depth look at the T accounts for different accounts, namely, assets, liabilities, and shareholder’s equity, the major components of the balance sheet or statement of financial position.

For asset accounts, which include cash, accounts receivable, inventory, PP&E, and others, the left side of the T Account (debit side) is always an increase to the account. The right side (credit side) is conversely, a decrease to the asset account. For liabilities and equity accounts, however, debits always signify a decrease to the account, while credits always signify an increase to the account.

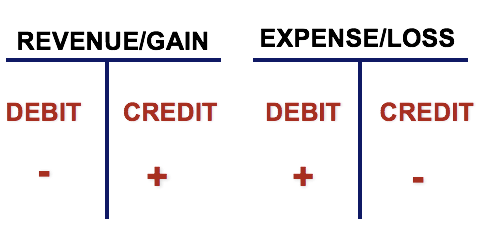

T Accounts are also used for income statement accounts as well, which include revenues, expenses, gains, and losses.

Once again, debits to revenue/gain decrease the account while credits increase the account. The opposite is true for expenses and losses. Putting all the accounts together, we can examine the following.

Using T Accounts, tracking multiple journal entries within a certain period of time becomes much easier. Every journal entry is posted to its respective T Account, on the correct side, by the correct amount.

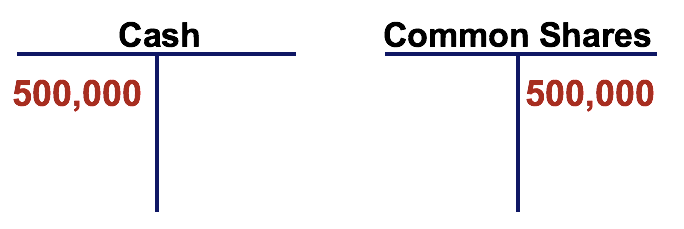

For example, if a company issued equity shares for $500,000, the journal entry would be composed of a Debit to Cash and a Credit to Common Shares.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

This has been CFI’s guide to T Accounts. To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: