Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A method for calculating the effect of outstanding stock options and warrants on diluted EPS

The treasury stock method is a way for companies to calculate how many additional shares may be generated from outstanding in-the-money warrants and options. The new additional shares are then used in calculating the company’s diluted earnings per share (EPS).

The treasury stock method implies that the money obtained by the company from the exercising of an in-the-money option is used for stock repurchases. Repurchasing those shares turns them into treasury stock, hence the name.

Generally Accepted Accounting Principles (GAAP) mandates that companies must provide details on their diluted EPS. Therefore, the GAAP method is utilized to compute this figure for financial reporting.

EPS is diluted due to outstanding in-the-money options and warrants. These allow investors who own them to buy a number of common shares at a price below lower than the current market price.

To learn more, launch our free accounting and finance courses!

Additional Shares Outstanding = Shares From Exercise – Repurchased Shares

Additional Shares Outstanding = n – (n x K / P)

Additional Shares Outstanding = n (1 – K/P)

Where:

To learn more, launch our free accounting and finance courses!

The treasury stock method has certain assumptions:

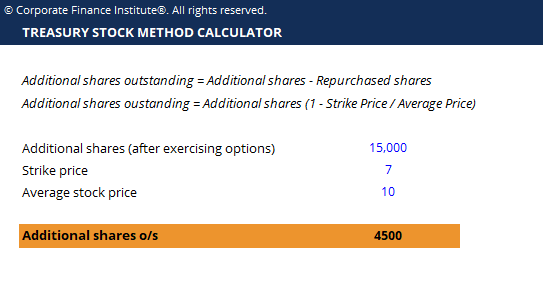

For example, a company has an outstanding total of in-the-money options and warrants for 15,000 shares. The exercise price of each of these options is $7. The average market price, however, for the reporting period is $10. Assuming all the options and warrants outstanding are exercised, the company will generate 15,000 x $7 = $105,000 in proceeds. Using these proceeds, the company can buy $105,000 / $10 = 10,500 shares at the average market price. Thus, the net increase in shares outstanding is 15,000 – 10,500 = 4,500.

This can also be found by simply using the last formula provided above. The net increase in shares outstanding is 15,000 (1 – 7/10) = 4,500.

Alternatively, use our free treasury stock method calculator to determine the effect of this example on shares outstanding.

Click the button below to download our free Treasury Stock Method calculator now!

The exercise of in-the-money options and warrants is the most dilutive of all potentially dilutive actions. In summary, EPS is calculated by dividing net income by weighted-average shares outstanding (WASO).

Using the treasury stock method, there is no effect on net income, as all proceeds from the repurchase are assumed to be used to repurchase treasury stock from the market. However, there is an effect on shares outstanding (WASO).

Since net income, the numerator, has a change of zero under the treasury stock method, and the weighted average shares outstanding, the denominator, increases, there is a guaranteed decrease in the diluted EPS.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

We hope this has been a helpful guide to the treasury stock method of calculating diluted shares outstanding. If you’re interested in advancing your career in corporate finance, these CFI articles will help you on your way: