Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

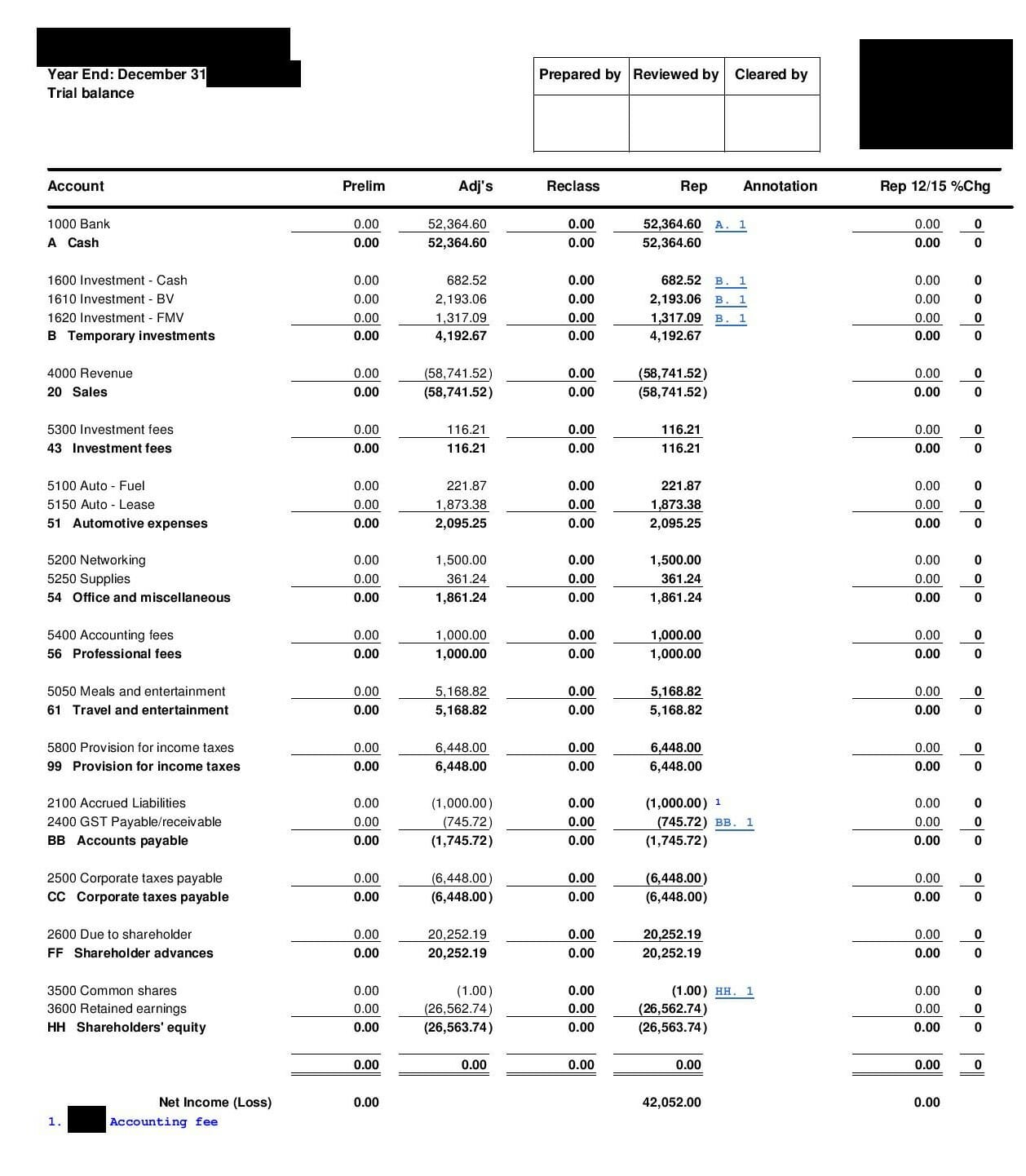

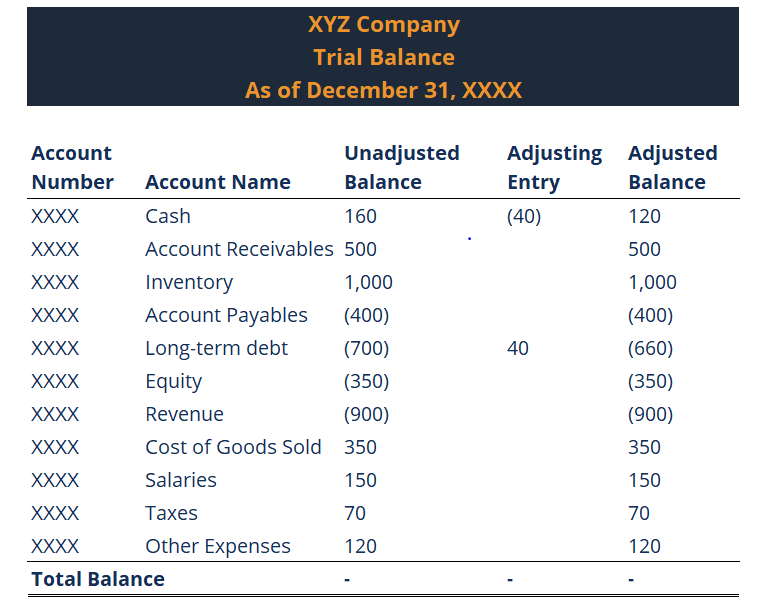

A report that lists the balances of all the company's general ledger accounts

A trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time. The accounts reflected on a trial balance are related to all major accounting items, including assets, liabilities, equity, revenues, expenses, gains, and losses. It is primarily used to identify the balance of debits and credits entries from the transactions recorded in the general ledger at a certain point in time.

Below is an example of a Company’s Trial Balance:

In addition to error detection, the trial balance is prepared to make the necessary adjusting entries to the general ledger. It is prepared again after the adjusting entries are posted to ensure that the total debits and credits are still balanced. It is not an official financial statement. It is usually used internally and is not distributed to people outside the company.

A trial balance includes a list of all general ledger account totals. Each account should include an account number, description of the account, and its final debit/credit balance. In addition, it should state the final date of the accounting period for which the report is created. The main difference from the general ledger is that the general ledger shows all of the transactions by account, whereas the trial balance only shows the account totals, not each separate transaction.

Finally, if some adjusting entries were entered, it must be reflected on a trial balance. In this case, it should show the figures before the adjustment, the adjusting entry, and the balances after the adjustment.

A trial balance can trace the mathematical inaccuracy of the general ledger. However, there are a number of errors that cannot be detected by this report:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Trial Balance. From here, we recommend continuing to build out your knowledge and understanding of more corporate finance topics, such as: