Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The process of determining a debtor’s ability to repay loan obligations

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

Credit analysis is a process undertaken by lenders to understand the creditworthiness of a prospective borrower, meaning how capable (and how likely) they are of repaying principal and interest obligations.

The borrower, also known as the debtor, could be an individual or a business entity; the former is referred to as retail (or personal) lending, and the latter is what’s known as commercial lending.

Lenders, also known as creditors, employ a variety of qualitative and quantitative techniques (including risk models) when conducting credit analysis in order to quantify and effectively price risk.

Credit is “created” when one party receives resources from another party, but payment is not expected until some contracted date (or dates) in the future.

The resource may be cash, as is the case with a bank loan. Alternatively, the resource may be a physical product (like inventory); this is called trade credit.

In both cases, credit risk exists. This is defined as the risk that a creditor will advance resources to a debtor, but that payment (or repayment) will not be made. Credit analysis is conducted in order to understand the level of credit risk presented by a borrower, given the parameters of a specific credit request.

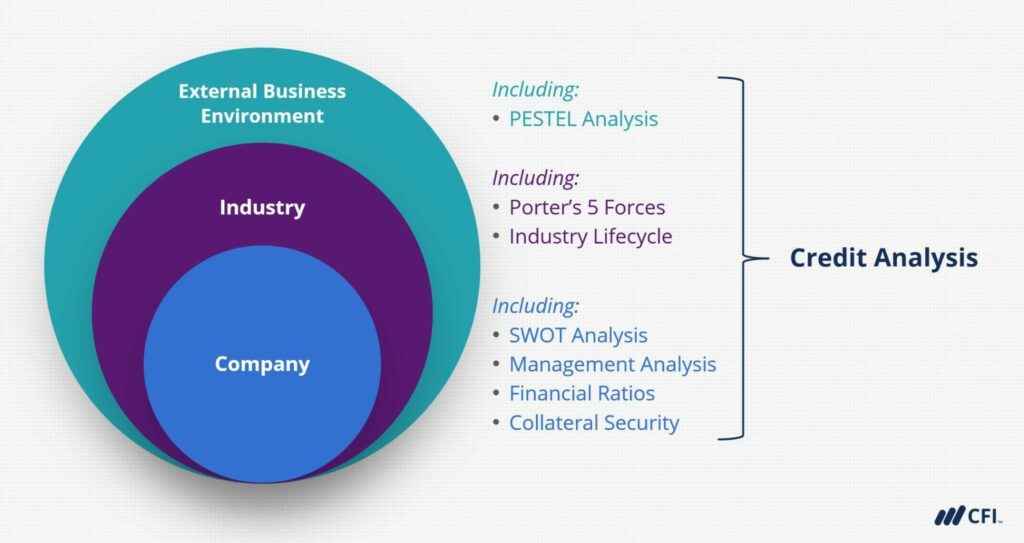

Credit professionals analyzing a prospective borrower will employ a variety of qualitative and quantitative techniques.

Qualitative techniques include trying to understand risks in the external environment, like where interest rates are heading and the state of the broader economy, among others. A framework like PESTEL is often employed.

For commercial lenders, specifically, they’ll also want to understand business characteristics – like the borrower’s competitive advantage(s) and industry trends (using frameworks like SWOT and Porter’s 5 Forces, respectively). Management experience is another very important consideration.

Quantitative elements of the analysis include assessing financial ratios using risk models, understanding financial projections, employing sensitivity analysis, and evaluating the strength of any physical collateral that could serve as security against the credit exposure.

A popular credit analysis framework is the 5 Cs of Credit; the 5 Cs underpin the component parts of most risk rating and loan pricing models. The 5 Cs are:

Personal lending (often referred to as “retail credit”) tends to be much more formulaic than its commercial counterpart.

With commercial credit analysis specifically – where the borrower is seeking a business loan – lenders must make sense of each individual business entity. And as we know, no two businesses are completely alike.

Underwriting commercial credit requires a larger number of quantitative and qualitative data points, which go into a risk model to calculate a corporate credit rating. This credit rating (or score) directly impacts pricing and other elements of loan structure.

There is considerable opportunity for finance enthusiasts that wish to make a career in commercial banking; 2022 commercial banking industry revenue in the United States was estimated at USD$963bn[1].

Strong credit analysis and lending management skills can open the door to a range of job opportunities in financial services, whether you’re seeking a career in personal or corporate finance. Some prospective employers include:

This includes traditional commercial banks of all sizes, as well as credit unions. There are countless relationship management, analyst, and risk management-type roles at financial institutions where someone with strong credit acumen can build a very rewarding career for themselves.

Private, non-bank lenders come in many shapes and sizes, including residential and commercial real estate lending, equipment finance, and asset-based lending, among others. There are also many opportunities for people with lending experience to look at private loan and mortgage broker firms.

Many businesses that sell B2B extend credit terms to their customers; this is what’s called trade credit. Many large corporations employ entire teams of credit analysts to assess the creditworthiness of prospective customers and to set reasonable limits on their accounts.

Rating agencies like Fitch and Moody’s employ teams of credit analysts to assess the credit risk of publicly traded companies. This fixed income credit analysis supports debt ratings that are used to price fixed income securities, which trade publicly (like corporate bonds).

These firms also hire credit analysts to manage risk in their investment portfolios, or even to manage the balance sheets of individual private companies that the firm has invested in and which employ debt in their capital structures.

Fintech is an abbreviation of two words – “financial technology.” For decades, technology applications have disrupted traditional products and services across a variety of sectors; financial services is no exception.

Many technology companies are developing AI (artificial intelligence) and machine learning-driven algorithms and programs to analyze and underwrite credit more quickly and efficiently than traditional financial services firms, which rely heavily on human intermediaries and considerable paperwork.

While much of the disruption and development has occurred in personal lending (where underwriting credit is more homogenous and generally involves fewer data points), some companies are also trying to innovate in the commercial credit space, particularly at the smaller end of the business landscape.

CFI offers the Commercial Banking & Credit Analyst™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: