Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of loan where the interest rate changes according to changes in market interest rates at set reset dates (for example, monthly or quarterly)

A variable rate loan is a type of loan where the interest changes according to changes in market interest rates. Unlike a fixed-rate loan, where borrowers pay a constant interest rate, a variable rate loan comprises varying monthly or quarterly payments that change according to market interest rate changes.

Lenders typically link variable rate loans to a benchmark such as the Secured Overnight Financing Rate (SOFR) in the U.S., the prime rate, or other regional reference rates. When the benchmark changes, the lender adjusts the loan’s interest rate in line with the agreement. Rate adjustments don’t happen daily but occur at set intervals, such as monthly, quarterly, or semiannually, depending on the loan terms.

In corporate and bank borrowing scenarios, a variable rate loan is tied to a benchmark interest rate, often SOFR in the United States. SOFR reflects the cost of overnight borrowing backed by U.S. Treasury securities and is based on actual market transactions.

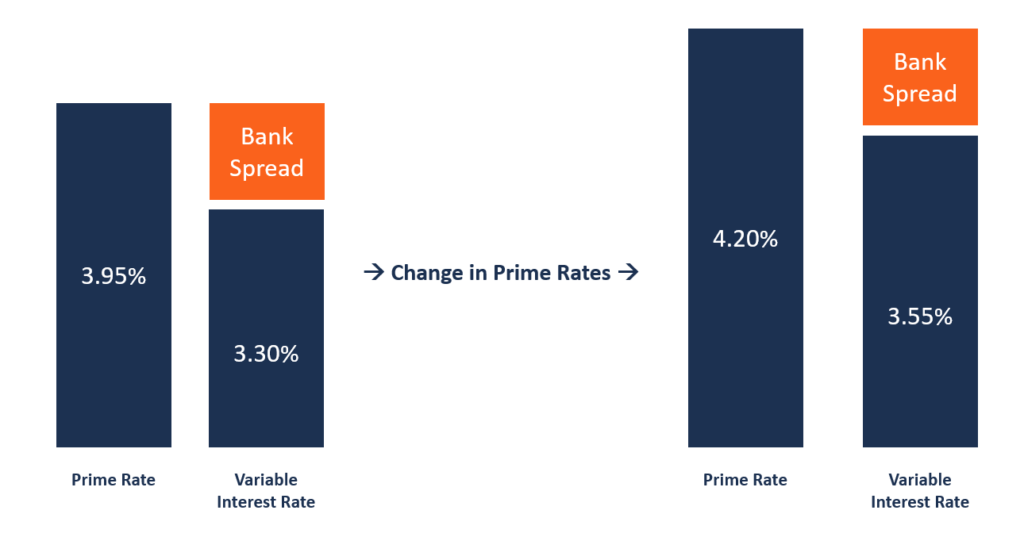

A common benchmark used in retail lending is the prime rate. The prime rate is a reference rate for products like auto loans, mortgages, and credit cards. The prime rate is closely tied to the Federal Reserve’s target federal funds rate. When the Fed raises or lowers the federal funds rate, banks usually adjust their prime rate in the same direction.

Lenders set loan rates by adding a margin or spread to the chosen benchmark. The spread depends on factors such as the type of loan, the length of the term, and the borrower’s credit profile. For example, a commercial loan may be priced at Term SOFR + 3%, meaning the rate resets in line with SOFR at agreed intervals, while the 3% spread represents the lender’s margin.

From the borrower’s perspective, a variable rate loan is beneficial because they are often subject to lower interest rates than fixed-rate loans. However, variable rate loans can become more expensive if interest rates rise over the loan’s term.

Most often, the interest rate tends to be lower at the beginning, and it may adjust over the course of the loan term. During periods of constantly fluctuating interest rates, a fixed-rate loan tends to be more attractive than a variable loan. In such cases, fixed-rate loans come with an interest rate that remains unchanged during the duration of the loan.

From the lender’s perspective, a variable rate loan offers greater value compared to a fixed-rate loan. Lenders can adjust the interest rate upwards to reflect market changes, while the interest charged on a fixed-rate loan remains fixed regardless of the changes in the market.

A variable rate mortgage is a home loan where the interest rate is adjusted periodically to reflect changes in the benchmark interest rate. Mortgage lenders can offer a variable interest rate on the home loan for the entire term of the loan or an adjustable-rate mortgage that combines both fixed and variable interest rates. A variable rate mortgage is adjusted at a rate that is above the reference or benchmark rate.

Borrowers prefer variable loans when they expect interest rates to fall in the future, as they can benefit from lower rates when market interest rates decline. On the other hand, where the loan agreement provides a cap on the variable rate, the borrowers are protected from rising interest rates. This means there is a maximum limit on how much the borrower can be charged, regardless of the benchmark interest rate.

The variable rate for a mortgage is structured in a way that it includes an indexed rate and a variable rate margin. High-quality borrowers may qualify for a lower margin above the indexed rate, which is typically pegged to the lender’s prime rate or to SOFR in the U.S. The interest rate on the mortgage then fluctuates with changes in the chosen benchmark.

The loan can take two forms. First, borrowers can be charged a variable interest rate throughout the entire term of the loan. In this case, the rate is the indexed benchmark plus a spread determined by the lender. Alternatively, the variable component can be part of a hybrid loan.

For example, a 5/1 adjustable-rate mortgage is a type of hybrid loan. Borrowers pay a fixed interest rate for the first five years, after which the rate resets annually based on the benchmark rate plus the lender’s margin.

CFI is the official provider of the Certified Banking & Credit Analyst (CBCA)® certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: