Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The entity or person to whom a bill is addressed and is given instructions to pay

Common in bill or check transactions, a drawee can be described as the entity or person upon whom a bill or check is drawn. The drawee is the entity or person to whom a bill is addressed and is given instructions to pay. In most cases, when a check (bill of exchange) is being drawn, the party said to be the drawee is normally a banker.

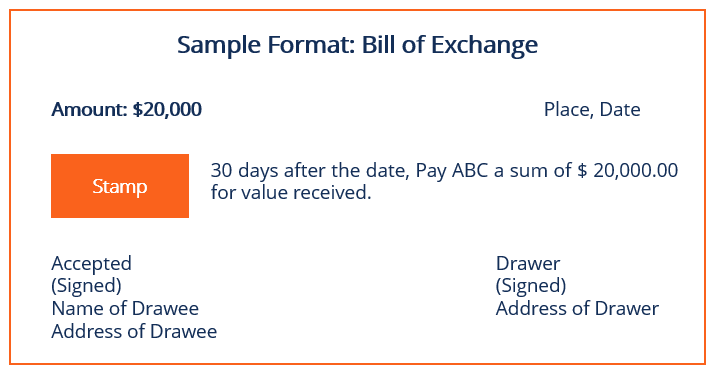

The individual or entity who draws up the bill is known as the drawer, and the person or entity to whom the bill is favorably drawn is known as the payee. They are the receiver of the payment or to whom the bill is payable.

In a financial transaction, a drawee typically serves as an intermediary. The primary purpose of the drawee is to channel and direct funds from a payer’s account (also known as a drawer or depositor) to the account of the payee (the receiver of the funds or the natural person to whom the funds are payable).

In most instances, the drawee is a financial institution. In such a situation, the drawee holds the funds from the payer in an account that it manages. The account is often a deposit account. It is a common function for consumer and/or commercial banks. The consumer bank takes funds from the account of the payer or depositor to meet the financial obligation set forth in accordance with the information provided on a check.

Apart from banks, other entities that can serve as a drawee can be wire transfer and money order companies and companies that provide check-cashing services. It is important to note that the entities may require processing fees to facilitate and process the transaction to completion. Money orders typically serve as a bill of exchange (the drawee role). In such a transaction, the bill of exchange is presented to the payee and is honored by the entity that receives the funds from the depositor or payer.

To depict and highlight the role and function of a drawer, consider the following example:

Mary works at Company ABC. The company pays its employees on the 25th of each month. The employees (including Mary) obtain their salaries through a check. Assuming it is the 25th of January today, Mary receives her salary check and presents it to her bank to cash the check. Mary’s bank will have the funds directed from the bank account of the company into Mary’s account, in accordance with the figure stipulated on the check. Hence, the bank deducts the funds from Company ABC’s account and pay the funds directly into Mary’s account.

In this scenario, Company ABC has instructed the bank to draw funds from its account and have those funds sent to Mary’s account. The bank is the drawee in this setting, company ABC is the drawer, and Mary is the Payee.

Henceforth, the owner of the account from which the funds are to be drawn is referred to as the drawer, the bank or institution that is facilitating the channeling of the funds from the drawer’s account is known as the drawee, and the person to whom the funds are sent to is the payee.

It is important to note that a drawee is not always a financial or banking institution. A common example is the use of coupons. Suppose there is a manufacturer who distributes coupons to individuals or entities. The coupon holder decides to make use of the coupon as part of a transaction. The store or shop that receives and accepts the coupon can be regarded as the drawee.

Although the transaction does not necessarily require a physical channeling of funds due to the coupon acting as a discount voucher – i.e., no cash is handed directly to the customer or the coupon is not cashed as would be the case with a check – it may still result in actual payment. It would depend on the regulations that govern the activity.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.