Money Order

A guaranteed form of payment for a specified amount that two parties can use as a form of payment in exchange for a given product or service

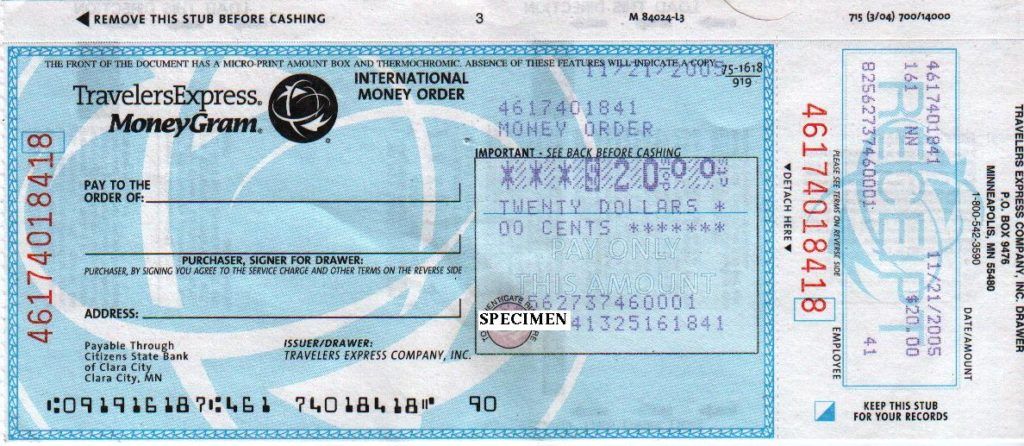

What is a Money Order?

A money order is a guaranteed form of payment for a specified amount that two parties can use as a form of payment in exchange for a given product or service. To obtain a money order, an entity must pay the amount that’s been agreed upon for a good or service.

The issuer will then produce the official money order document – which can then be given to the other party (or parties) involved in the transaction. Upon receipt, it can be exchanged for a deposit in the holder’s bank account.

History of Money Order

The money order concept came into existence in late 18th century Britain. When the concept was initially pioneered, it was not particularly successful. It was because of the system’s high fees, which made more traditional payment methods such as cash or checks more appealing. The payment system was then sold off to a private buyer who was able to significantly lower the fees associated with requesting a money order, making the system popular.

The most pivotal point in the history of money orders occurred when the British Post Office saw value in the service. British postal officials welcomed the idea that one party could safely send a money order to another party without running the risk of theft.

If cash was sent, it could easily be stolen and added to any bank account. A money order was legally binding and could only be deposited into the account of a specified entity. The post office acquired the system and managed to improve its profitability, making it a significant source of cash flow for the organization.

Disadvantages

While the concept was deemed fairly appealing and profitable, it still comes with a few disadvantages. The payment system saw very limited acceptance and usage in the brokerage and insurance industries due to concerns over how it could be used for money laundering.

Since the system could easily be used in business transactions between a multitude of parties, it could potentially serve as a vehicle for laundering money obtained through illegal activities. For example, a criminal organization could receive income through several money orders and declare this income through a limited liability company (LLC), thus rendering the money legitimate or “clean.”

To combat the exploitation of money orders as money laundering instruments, bureaucratic policies were implemented in an attempt to set up checks and balances in the system. Legislation such as the U.S. Bank Secrecy Act and the USA Patriot Act requires that money orders be subject to “more regulatory processing” than checks (since those could be easily forged).

As part of efforts to make the practice safer, the U.S. government also capped the maximum transaction amount at $1,000 for domestic orders and $700 for international orders.

Money Order Alternatives

With advancements in technology, consumers can now avail themselves of a number of alternatives to money orders. The newer alternatives are notably cheaper, more efficient, and safer.

Alternatives include the MasterCard/Visa credit payment systems, the Konbini system in Japan, and the Postepay system in Italy. In the United States, PaidByCash continues to grow in popularity and is currently offered in more than 60,000 stores across the country.

In conclusion, money orders were the first monetary transaction vehicles that pioneered the advent of modern payment processing technologies.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful: