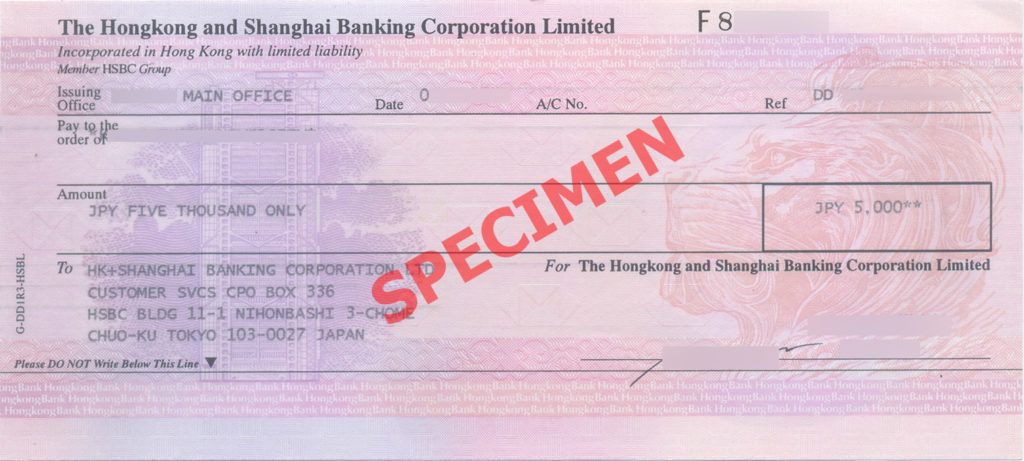

Demand Draft

A negotiable instrument to transfer funds from one bank to another

What is a Demand Draft?

A demand draft, also called a remotely created check (RCC), is a negotiable instrument to transfer funds from one bank to another. It is issued by a bank to a client (drawer) in order to direct a different bank or another branch of the same bank (drawee) to pay the specified amount of money to the payee.

When a demand draft is issued to the drawer, the money is debited from the drawer’s account. Once it is given to the payee and he/she presents it to the bank, it is immediately paid out to the payee in the form of cash or check.

Sometimes, the drawer and the payee can be the same person, as the drawer may want to transfer money from one bank account to another account at a different bank.

Characteristics of a Demand Draft

- It is issued by the bank to another bank.

- It is considered to be a prepaid negotiable instrument because the money is taken from the drawer’s account when it is issued. Therefore, when the payee cashes it out, it will not bounce due to insufficient funds since the payment is already made by the drawer. As a result, it is more secure and comes with less risk compared to a check.

- It is only payable to the payee written on the demand draft, and it is payable on demand. It means the payee can immediately be paid the specified amount and cannot be stopped from payment once he/she presents it to the bank to be cashed out.

- It does not require the use of a signature to authorize the transfer of funds. It can be authorized remotely by fax, phone, or online. Instead of a signature, it will say “authorized by depositor” or “authorized by drawer.”

How Do You Get a Demand Draft?

You can visit your bank or fill out an online application offered by your bank. You need to provide details such as your bank account information, the full name of the payee, and the address of the payee’s bank.

You also need to provide the amount of money, the currency of the money, the reason for payment, and instructions about whether the bank should send it to you or directly to the payee. In addition, you may be required to pay a fee to the bank before the demand draft can be issued.

When is a Demand Draft Used?

A demand draft can be used when you purchase items online or over the phone. It can also be used when there are recurring debits from your bank account, such as bill payments.

Other common uses include return item fees, customer payments made remotely from the company, and transfer payments between different bank accounts. Therefore, demand drafts can usually be accepted by telemarketers, utility companies, credit card companies, and insurance agencies.

Types of Demand Drafts

1. Sight demand draft

A slight demand draft is payable immediately, and it is often used when purchasing goods internationally. For example, when a seller ships goods to a buyer, the seller still possesses the title of the goods until the buyer receives the goods.

The buyer can use a sight demand draft to transfer funds to the seller instantly so the seller can immediately transfer the title of goods to the buyer.

2. Time demand draft

A time demand draft comes with a set payment date in the future, and it is not payable immediately. It is only payable in full after a certain amount of time when the goods are received by the payee.

In international trade, some exporters and importers may prefer to use a time demand draft. For example, an importer issues a time demand draft to the exporter, but payment in full can only be made 15 days after the arrival of the shipment of goods and the transfer of the title of goods to the importer.

Safety Regulations

Since the use of a signature is not required and issuance can be done remotely (i.e., phone, fax, online), it is susceptible to fraud, as scammers only need to know your bank account information in order to debit your account. However, banks will deny unauthorized demand drafts if they detect suspicious activity.

Depending on your bank and the country you are in, you are given approximately 90 days from the time the demand draft is deposited to the payee’s account to dispute the transaction. There may also be regulations to govern your safety, depending on your location.

For example, the U.S. Federal Reserve issued a regulation that shifts the liability for loss from the drawer’s bank to the payee’s bank. As a result, it helps the drawer to avoid paying for fraudulent demand drafts.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: