Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A binding agreement that outlines the rights and obligations of both parties in an M&A deal

An M&A deal structure is a binding agreement between parties in a merger or acquisition (M&A) that outlines the rights and obligations of both parties. It states what each party of the merger or acquisition is entitled to and what each is obliged to do under the agreement. Simply put, a deal structure can be referred to as the terms and conditions of an M&A.

Mergers and acquisitions involve the coming together (synergizing) of two business entities to become one for economic, social, or other reasons. A merger or acquisition is possible only when there is a mutual agreement between both parties. The agreed upon terms on which these entities are willing to come together are known as an M&A deal structure.

Deal structuring is a part of the M&A process; it is one of the steps that must be taken in a merger or acquisition. It is the process of prioritizing the objectives of a merger or acquisition and ensuring that the top-priority objectives of all parties involved are satisfied, along with considering the weight of risk each party must bear. Initiating the deal structuring process requires all parties involved to state:

Developing a proper M&A deal structure can be quite complicated and challenging because of the number of factors to be considered. These factors include preferred financing means, corporate control, business plan, market conditions, antitrust laws, accounting policies, etc. Employing the right kind of financial, investment, and legal advice can make the process less complicated.

There are three well-known traditional ways of structuring a merger acquisition deal although, in recent times, business entities have engaged in other, more creative and flexible deal structuring methods. The three traditional ways of structuring an M&A deal are asset acquisition, stock purchase, and mergers. The methods can also be combined to achieve a more flexible deal structure.

In an asset acquisition, the buyer purchases the assets of the selling company. An asset acquisition is usually the best deal structure for the selling company if it prefers a cash transaction. The buyer chooses which assets it wants to purchase.

Advantages of an asset acquisition may include:

Disadvantages of an asset acquisition include:

Unlike an asset acquisition, where there is a direct transaction of assets, assets are not directly transacted in a stock purchase. In a stock purchase acquisition, a majority amount of the seller’s voting stock shares are acquired by the buyer. In essence, it means control of the seller’s assets and liabilities are transferred to the buyer.

Advantages of a stock purchase acquisition:

Disadvantages of a stock purchase acquisition:

Though the term “merger” is commonly used interchangeably with “acquisition,” in a strict sense, a merger is the result of an agreement between two separate business entities to come together as one new entity. A merger is typically less complicated than an acquisition because all liabilities, assets, etc. become that of the new entity.

In structuring a deal, the advantages and disadvantages must be considered along with other influencing factors to reach a conclusion on which method to adopt.

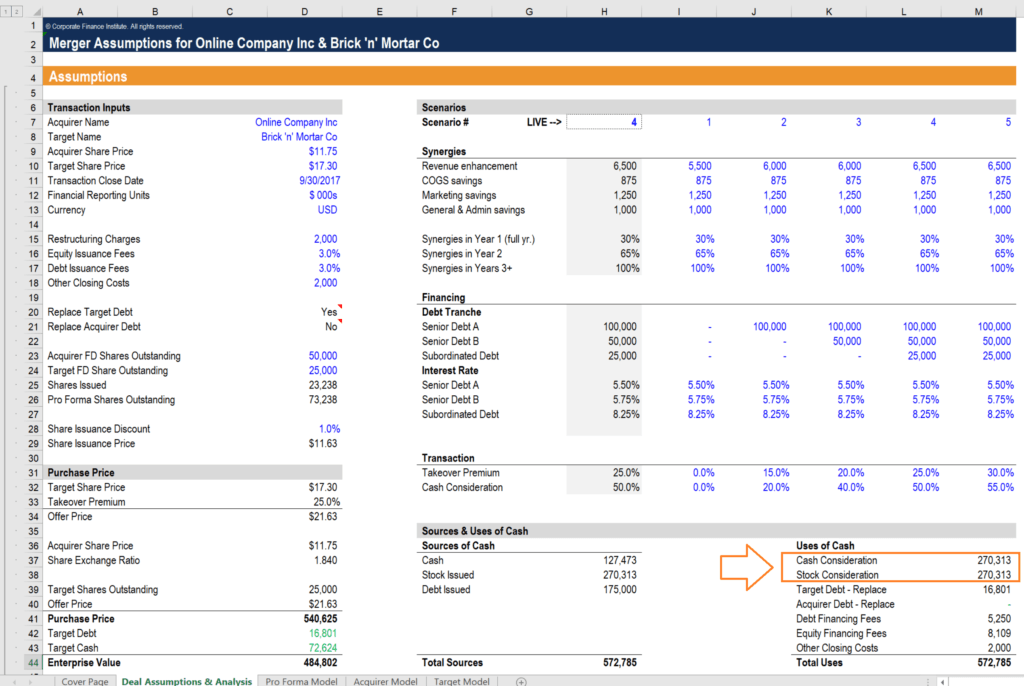

Below is a screenshot from CFI’s M&A Model Course, which has an assumptions section that includes various deal structures.

To create a great deal structure, aim for a win-win scenario, where the interests of both parties are well represented in the deal and risks are reduced to the barest minimum. Most often, win-win deal structures are more likely to lead to a sealed merger or acquisition deal and may even reduce the time required to complete the M&A process.

There are two important documents that are used to delineate the M&A deal structuring process. They are the Term Sheet and Letter of Intent (LOI).

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: