Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

How the laws of supply and demand apply in a macro context

Aggregate supply and demand refers to the concept of supply and demand but applied at a macroeconomic scale. Aggregate supply and aggregate demand are both plotted against the aggregate price level in a nation and the aggregate quantity of goods and services exchanged at a specified price.

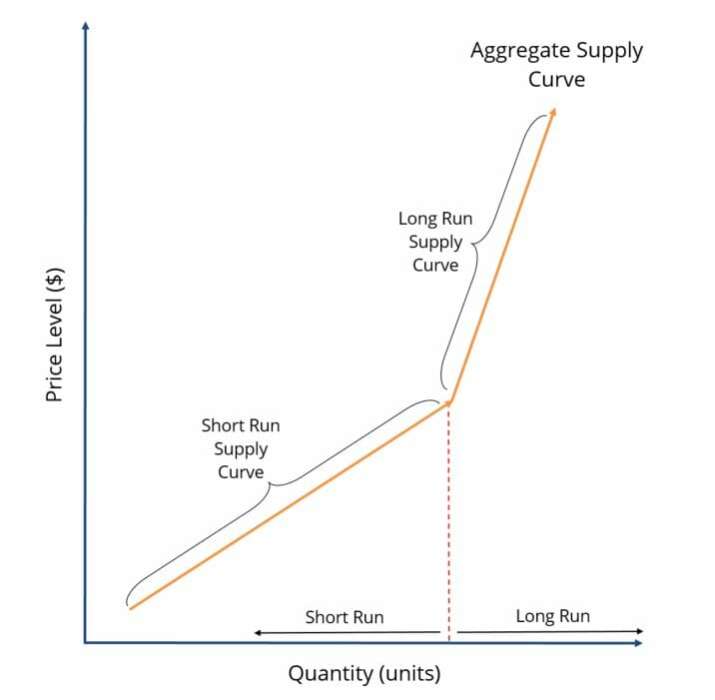

The aggregate supply curve measures the relationship between the price level of goods supplied to the economy and the quantity of goods supplied. In the short run, the supply curve is fairly elastic, whereas in the long run, it is fairly inelastic (steep). This has to do with the factors of production that a firm is able to change during these two different time intervals.

In the short run, a firm’s supply is constrained by the changes that can be made to short run production factors such as the amount of labor deployed, raw material inputs, or overtime hours. However, in the long run, firms are able to open new plants, expand plants or adopt new technologies, indicating that maximum supply is less constrained. For a more in-depth explanation of short vs. long run production, click here.

The reason why the supply curve is more inelastic (steeper) in the long run is that firms will be able to adapt to changes in price levels better. For instance, suppose that a firm can only increase production by 5% by changing short-run production factors and that the price level increases by 15%. Assuming unit elasticity for simplicity, the firm cannot supply the equilibrium supply quantity in the short run. Thus, its short-run aggregate supply curve will flatten as the firm cannot keep supplying goods at the same rate as prices increase.

However, in the long run, the firm is able to manipulate long-run production factors and provide the equilibrium quantity by producing 15% more. Thus, the curve is more inelastic as the firm becomes more responsive to price changes. In this case, short and long-run production are usually correlated with output quantity, such that a firm is able to better keep up with changes in output when long-run factors of production need to be changed to meet the equilibrium quantity. The graph below illustrates this concept:

Since consumer demand does not face the same constraints faced by suppliers, there is no relative change in the elasticity of demand itself. Rather, the steepness of the demand curve depends on the price elasticity of demand for the good. Thus, the aggregate demand curve follows a consistent downward slope, whose elasticity is subject to change due to factors such as:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following CFI resources: